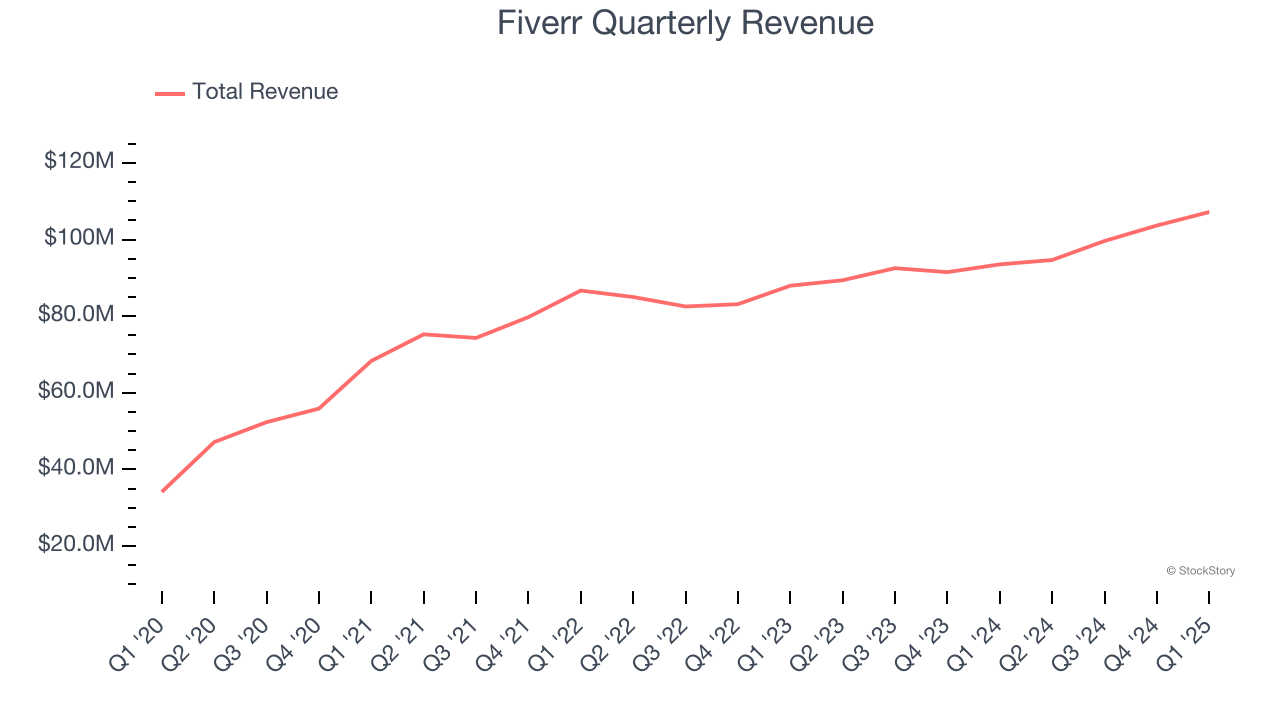

Online freelance marketplace Fiverr (NYSE: FVRR) reported Q1 CY2025 results beating Wall Street’s revenue expectations, with sales up 14.6% year on year to $107.2 million. Guidance for next quarter’s revenue was better than expected at $107 million at the midpoint, 0.7% above analysts’ estimates. Its non-GAAP profit of $0.64 per share was 8% above analysts’ consensus estimates.

Is now the time to buy Fiverr? Find out by accessing our full research report, it’s free.

Fiverr (FVRR) Q1 CY2025 Highlights:

- Revenue: $107.2 million vs analyst estimates of $106.1 million (14.6% year-on-year growth, 1% beat)

- Adjusted EPS: $0.64 vs analyst estimates of $0.59 (8% beat)

- Adjusted EBITDA: $19.44 million vs analyst estimates of $19.33 million (18.1% margin, 0.6% beat)

- The company slightly lifted its revenue guidance for the full year to $431.5 million at the midpoint from $430 million

- EBITDA guidance for the full year is $87 million at the midpoint, in line with analyst expectations

- Operating Margin: -4.8%, in line with the same quarter last year

- Free Cash Flow Margin: 25.5%, down from 28.6% in the previous quarter

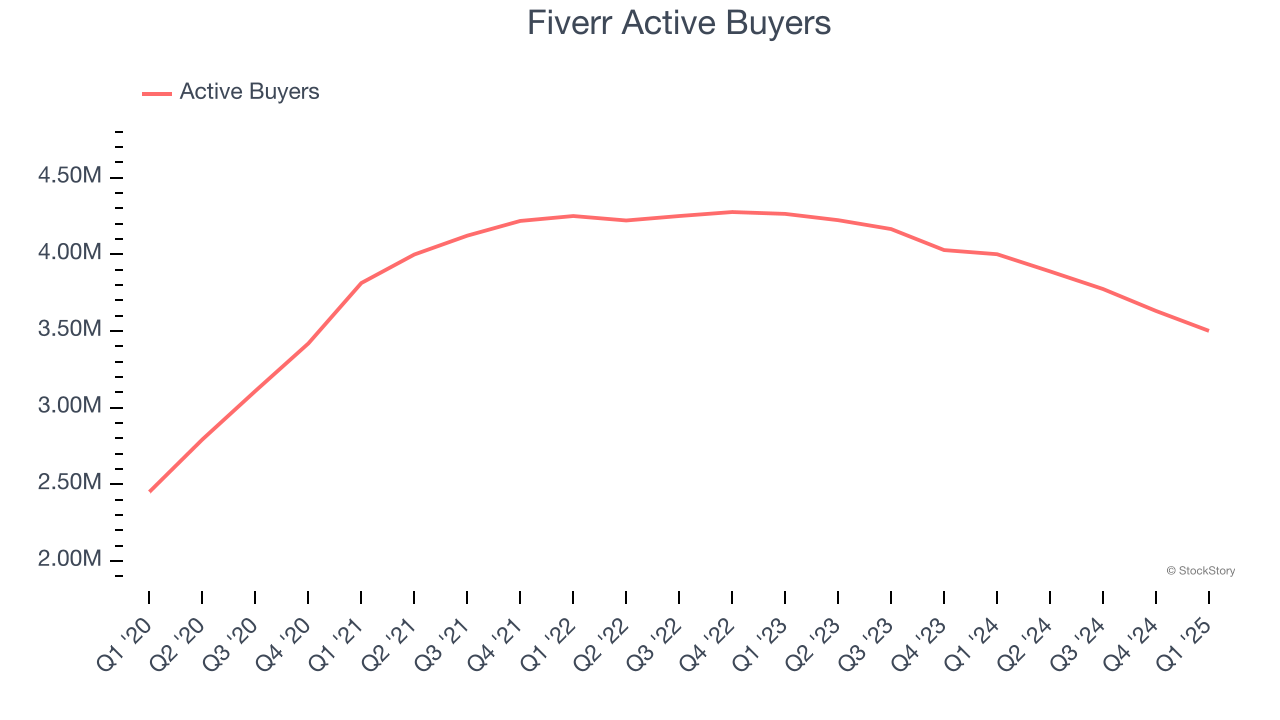

- Active Buyers: 3.5 million, down 500,000 year on year

- Market Capitalization: $962 million

“The year started off on a strong note with focused execution, as revenue and margins came in ahead of expectations. We continue to deliver stable Marketplace performance, robust Services revenue growth, and rapid AI product expansion. Following our recent successful Fiverr Go launch, we are seeing positive signs on buyer conversion, with buyers converting more and faster, as well as making more quality purchase decisions,” said Micha Kaufman, founder and CEO of Fiverr.

Company Overview

Based in Tel Aviv, Fiverr (NYSE: FVRR) operates a fixed price global freelance marketplace for digital services.

Sales Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Regrettably, Fiverr’s sales grew at a mediocre 8.6% compounded annual growth rate over the last three years. This wasn’t a great result compared to the rest of the consumer internet sector, but there are still things to like about Fiverr.

This quarter, Fiverr reported year-on-year revenue growth of 14.6%, and its $107.2 million of revenue exceeded Wall Street’s estimates by 1%. Company management is currently guiding for a 13% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 8.7% over the next 12 months, similar to its three-year rate. This projection doesn't excite us and indicates its newer products and services will not catalyze better top-line performance yet. At least the company is tracking well in other measures of financial health.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Active Buyers

Buyer Growth

As a gig economy marketplace, Fiverr generates revenue growth by expanding the number of services on its platform (e.g. rides, deliveries, freelance jobs) and raising the commission fee from each service provided.

Fiverr struggled with new customer acquisition over the last two years as its active buyers have declined by 6.7% annually to 3.5 million in the latest quarter. This performance isn't ideal because internet usage is secular, meaning there are typically unaddressed market opportunities. If Fiverr wants to accelerate growth, it likely needs to enhance the appeal of its current offerings or innovate with new products.

In Q1, Fiverr’s active buyers once again decreased by 500,000, a 12.5% drop since last year. The quarterly print was lower than its two-year result, suggesting its new initiatives aren’t moving the needle for buyers yet.

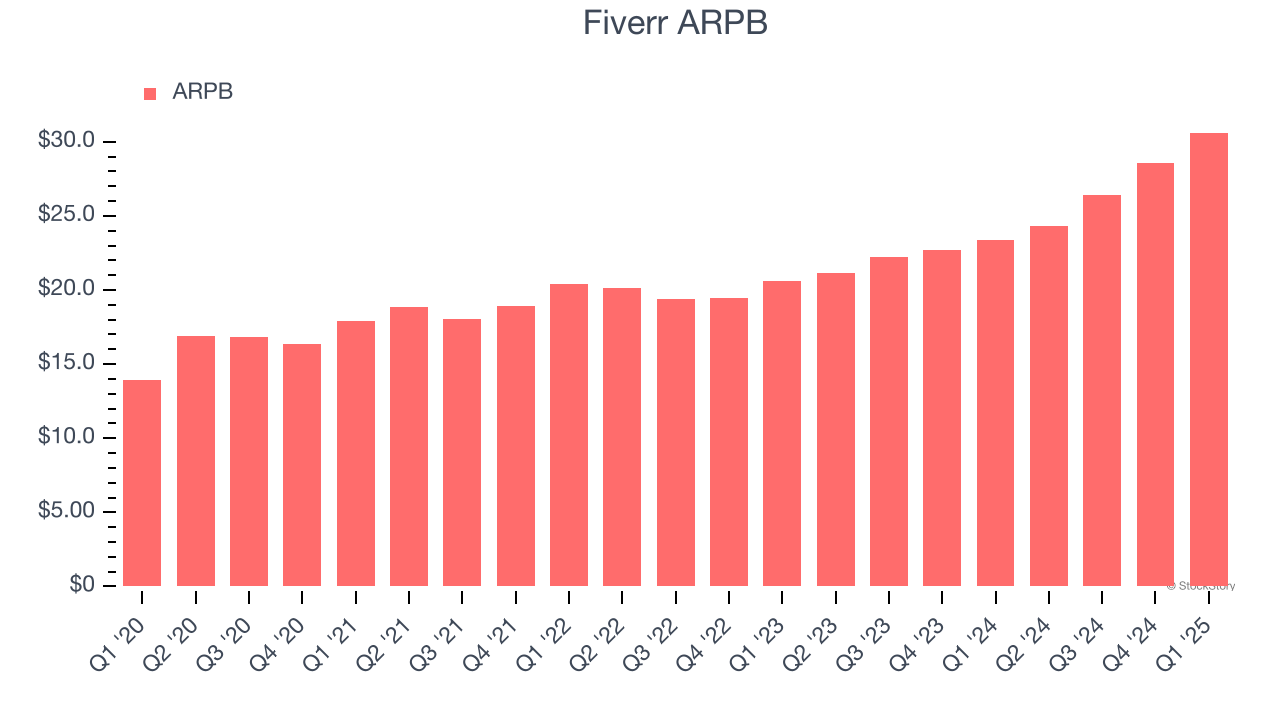

Revenue Per Buyer

Average revenue per buyer (ARPB) is a critical metric to track because it measures how much the company earns in transaction fees from each buyer. This number also informs us about Fiverr’s take rate, which represents its pricing leverage over the ecosystem, or "cut" from each transaction.

Fiverr’s ARPB growth has been exceptional over the last two years, averaging 17.5%. Although its active buyers shrank during this time, the company’s ability to successfully increase monetization demonstrates its platform’s value for existing buyers.

This quarter, Fiverr’s ARPB clocked in at $30.62. It grew by 31% year on year, faster than its active buyers.

Key Takeaways from Fiverr’s Q1 Results

Revenue, EBITDA, and EPS all beat in the quarter. It was also encouraging to see Fiverr’s EBITDA guidance for next quarter beat analysts’ expectations. We were also glad its revenue guidance for next quarter slightly exceeded Wall Street’s estimates. On the other hand, its number of active buyers fell short of Wall Street’s estimates. Overall, this was a solid quarter. The stock traded up 2.7% to $27.50 immediately following the results.

Is Fiverr an attractive investment opportunity right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.