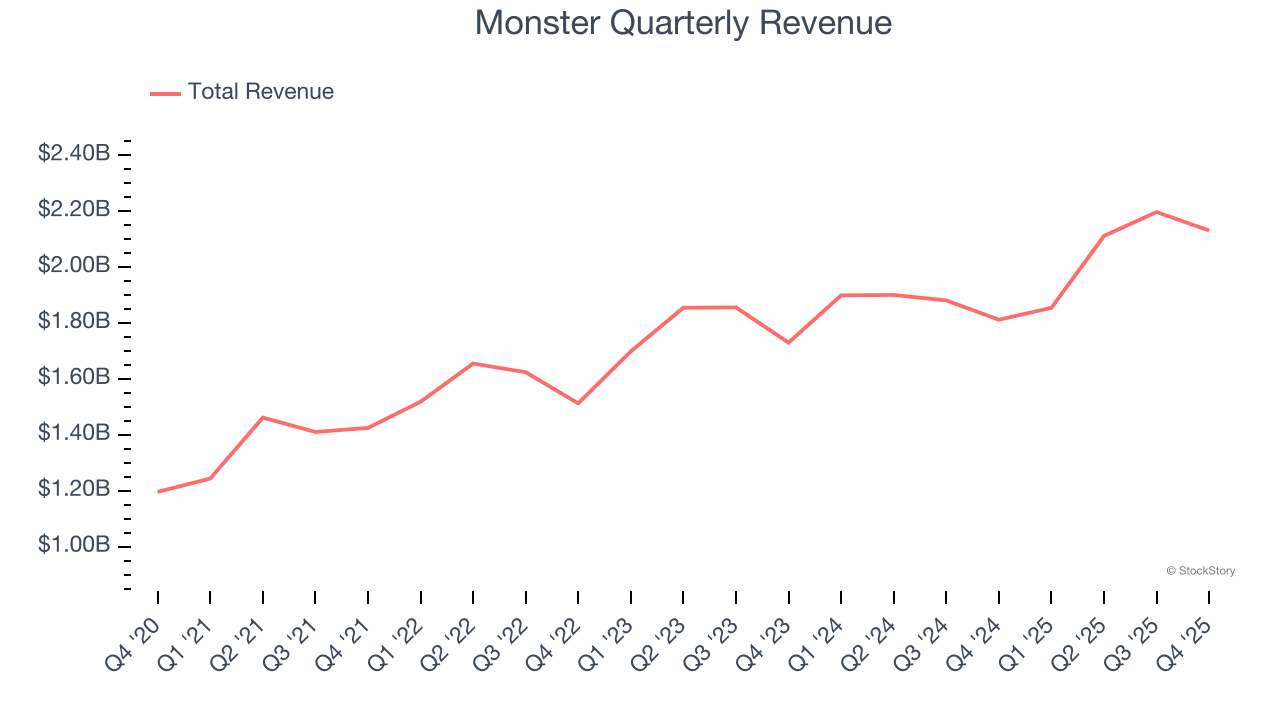

Energy drink company Monster Beverage (NASDAQ: MNST) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, with sales up 17.6% year on year to $2.13 billion. Its non-GAAP profit of $0.51 per share was 4.7% above analysts’ consensus estimates.

Is now the time to buy Monster? Find out by accessing our full research report, it’s free.

Monster (MNST) Q4 CY2025 Highlights:

- Revenue: $2.13 billion vs analyst estimates of $2.04 billion (17.6% year-on-year growth, 4.6% beat)

- Adjusted EPS: $0.51 vs analyst estimates of $0.49 (4.7% beat)

- Operating Margin: 25.5%, up from 21% in the same quarter last year

- Market Capitalization: $83.45 billion

Hilton H. Schlosberg, Chief Executive Officer, said, “The global energy drink category demonstrated solid growth in 2025, driven by increased consumer demand. We delivered a strong close to the year in both our domestic and international markets, with record 2025 fourth quarter net sales increasing 17.6 percent and crossing the $2.0 billion threshold for the first time in the Company’s history for a fiscal fourth quarter. Our net sales to customers outside the United States increased 26.9 percent in the 2025 fourth quarter to approximately 42 percent of total net sales. EMEA in particular, had a solid 2025 fourth quarter with increased net sales of 32.6 percent in dollars.

Company Overview

Founded in 2002 as a natural soda and juice company, Monster Beverage (NASDAQ: MNST) is a pioneer of the energy drink category, and its Monster Energy brand targets a young, active demographic.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $8.29 billion in revenue over the past 12 months, Monster is one of the larger consumer staples companies and benefits from a well-known brand that influences purchasing decisions.

As you can see below, Monster grew its sales at a decent 9.5% compounded annual growth rate over the last three years. This shows its offerings generated slightly more demand than the average consumer staples company, a helpful starting point for our analysis.

This quarter, Monster reported year-on-year revenue growth of 17.6%, and its $2.13 billion of revenue exceeded Wall Street’s estimates by 4.6%.

Looking ahead, sell-side analysts expect revenue to grow 8.4% over the next 12 months, similar to its three-year rate. Still, this projection is commendable and indicates the market is forecasting success for its products.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

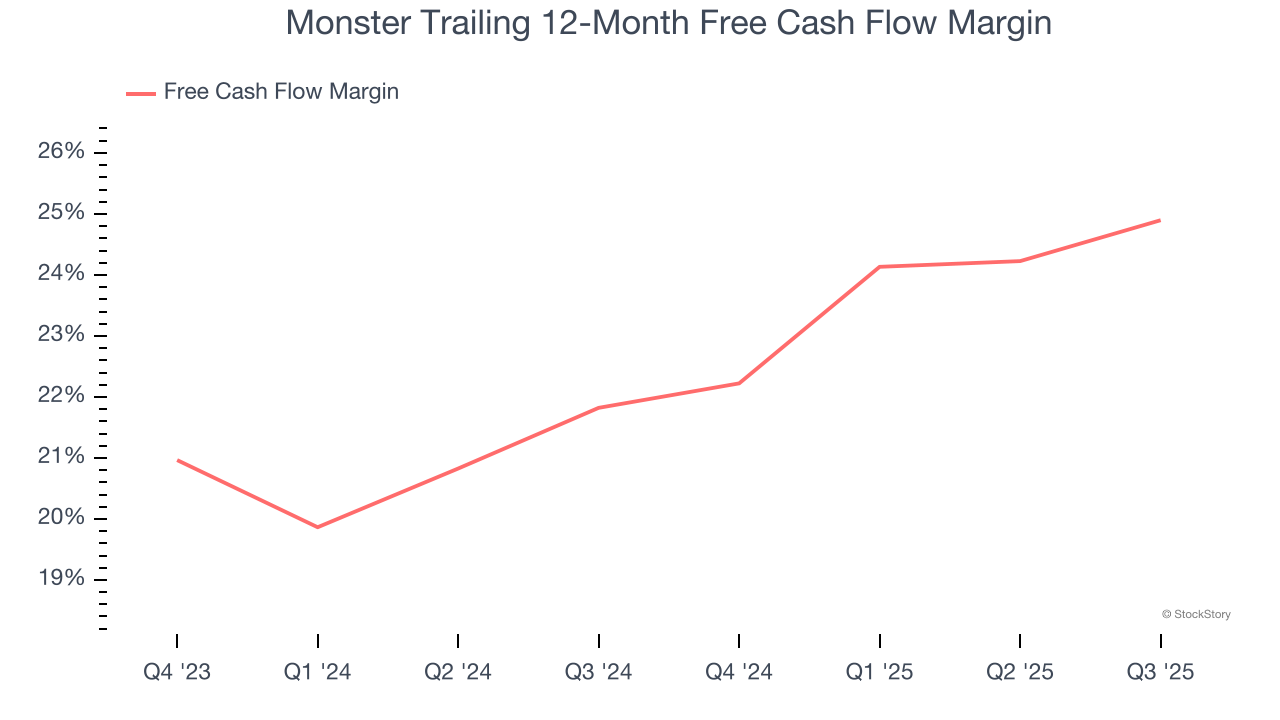

Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Monster has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition. The company’s free cash flow margin was among the best in the consumer staples sector, averaging 24% over the last two years.

Key Takeaways from Monster’s Q4 Results

We enjoyed seeing Monster beat analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its gross margin slightly missed. Overall, we think this was a decent quarter with some key metrics above expectations. The market seemed to be hoping for more, and the stock traded down 3% to $84.13 immediately following the results.

Big picture, is Monster a buy here and now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).