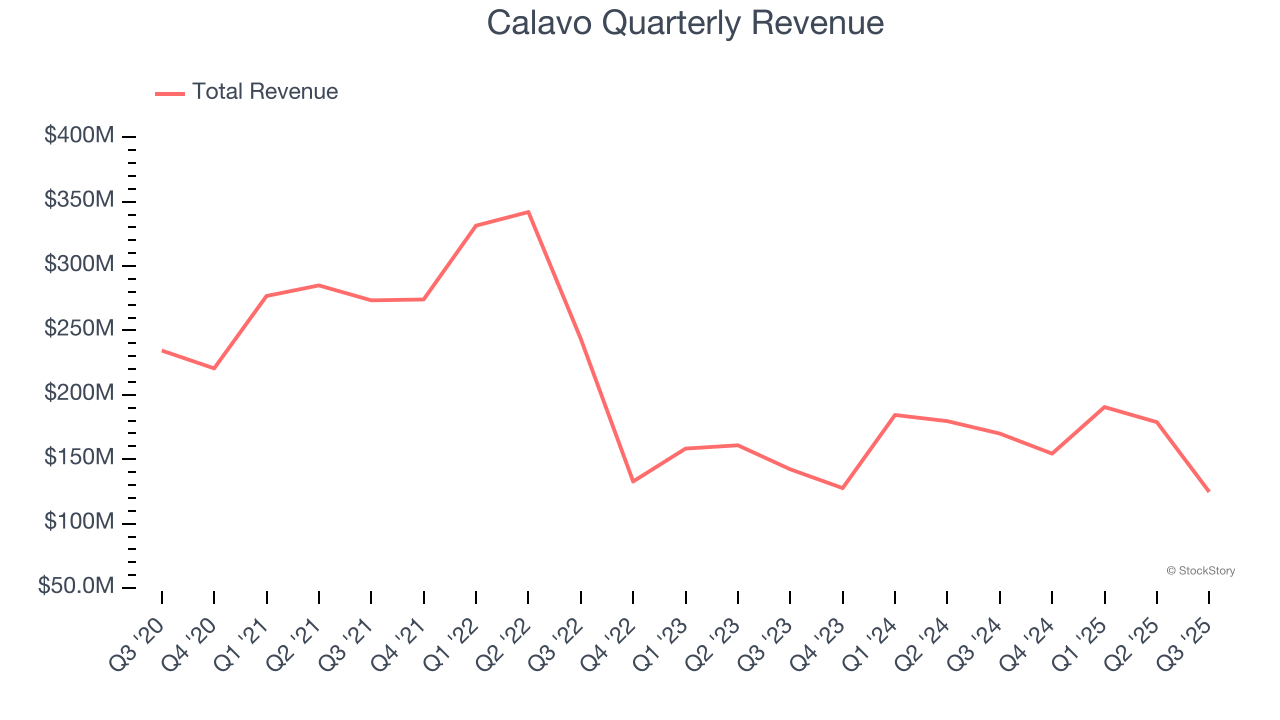

Fresh produce company Calavo Growers (NASDAQ: CVGW) fell short of the markets revenue expectations in Q3 CY2025, with sales falling 26.6% year on year to $124.7 million. Its non-GAAP profit of $0.25 per share was 32.4% below analysts’ consensus estimates. Stock surged from Mission Produce's acquisition announcement.

Is now the time to buy Calavo? Find out by accessing our full research report, it’s free.

Calavo (CVGW) Q3 CY2025 Highlights:

- Revenue: $124.7 million vs analyst estimates of $148 million (26.6% year-on-year decline, 15.7% miss)

- Adjusted EPS: $0.25 vs analyst expectations of $0.37 (32.4% miss)

- Adjusted EBITDA: $5.03 million vs analyst estimates of $10.45 million (4% margin, 51.9% miss)

- Operating Margin: -1.4%, down from 1.8% in the same quarter last year

- Market Capitalization: $396.3 million

- Acquisition Announcement: Mission Produce to acquire Calavo for $483 million

“Over the past century, the Calavo team has built this Company into a global leader in the processing and distribution of avocados, tomatoes, papayas, and guacamole,” said B. John Lindeman, President and Chief Executive Officer of Calavo Growers.

Company Overview

A trailblazer in the avocado industry, Calavo Growers (NASDAQ: CVGW) is a pioneering California-based provider of high-quality avocados and other fresh food products.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $648.4 million in revenue over the past 12 months, Calavo is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

As you can see below, Calavo struggled to generate demand over the last three years. Its sales dropped by 18.3% annually, a tough starting point for our analysis.

This quarter, Calavo missed Wall Street’s estimates and reported a rather uninspiring 26.6% year-on-year revenue decline, generating $124.7 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 14.7% over the next 12 months, an acceleration versus the last three years. This projection is noteworthy and suggests its newer products will spur better top-line performance.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Calavo has shown mediocre cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 3.3%, subpar for a consumer staples business.

Key Takeaways from Calavo’s Q3 Results

We struggled to find many positives in these results. Its revenue missed and its EBITDA fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded up 13.4% to $25.58 immediately following the results. Stock surged due to pending acquisition by Mission Produce.

Big picture, is Calavo a buy here and now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).