Wrapping up Q2 earnings, we look at the numbers and key takeaways for the gas and liquid handling stocks, including Parker-Hannifin (NYSE: PH) and its peers.

Gas and liquid handling companies possess the technical know-how and specialized equipment to handle valuable (and sometimes dangerous) substances. Lately, water conservation and carbon capture–which requires hydrogen and other gasses as well as specialized infrastructure–have been trending up, creating new demand for products such as filters, pumps, and valves. On the other hand, gas and liquid handling companies are at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

The 12 gas and liquid handling stocks we track reported a strong Q2. As a group, revenues beat analysts’ consensus estimates by 1.3% while next quarter’s revenue guidance was 2.7% below.

Thankfully, share prices of the companies have been resilient as they are up 7.3% on average since the latest earnings results.

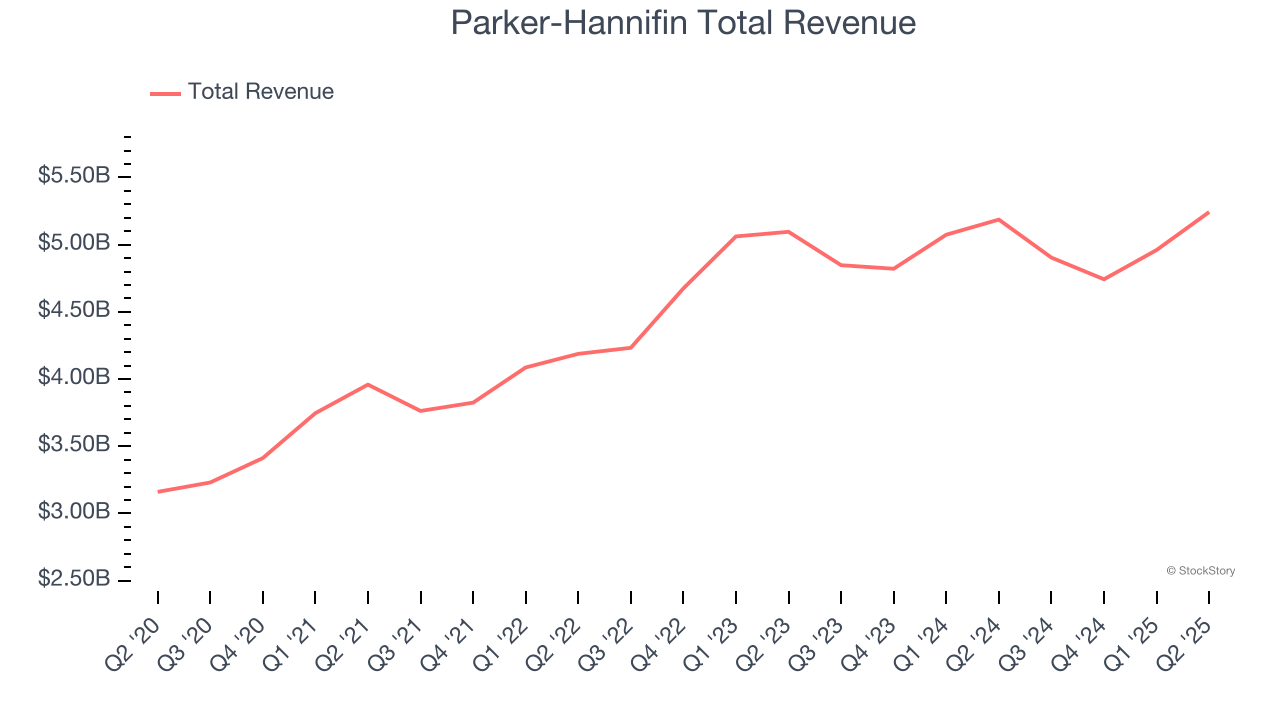

Parker-Hannifin (NYSE: PH)

Founded in 1917, Parker Hannifin (NYSE: PH) is a manufacturer of motion and control systems for a wide variety of mobile, industrial and aerospace markets.

Parker-Hannifin reported revenues of $5.24 billion, up 1.1% year on year. This print exceeded analysts’ expectations by 2.6%. Overall, it was a satisfactory quarter for the company with a solid beat of analysts’ organic revenue estimates.

“Our outstanding performance contributed to a record year for safety, engagement, earnings per share, margins and cash flow,” said Jenny Parmentier, Chairman and Chief Executive Officer.

Interestingly, the stock is up 7.5% since reporting and currently trades at $748.60.

Is now the time to buy Parker-Hannifin? Access our full analysis of the earnings results here, it’s free.

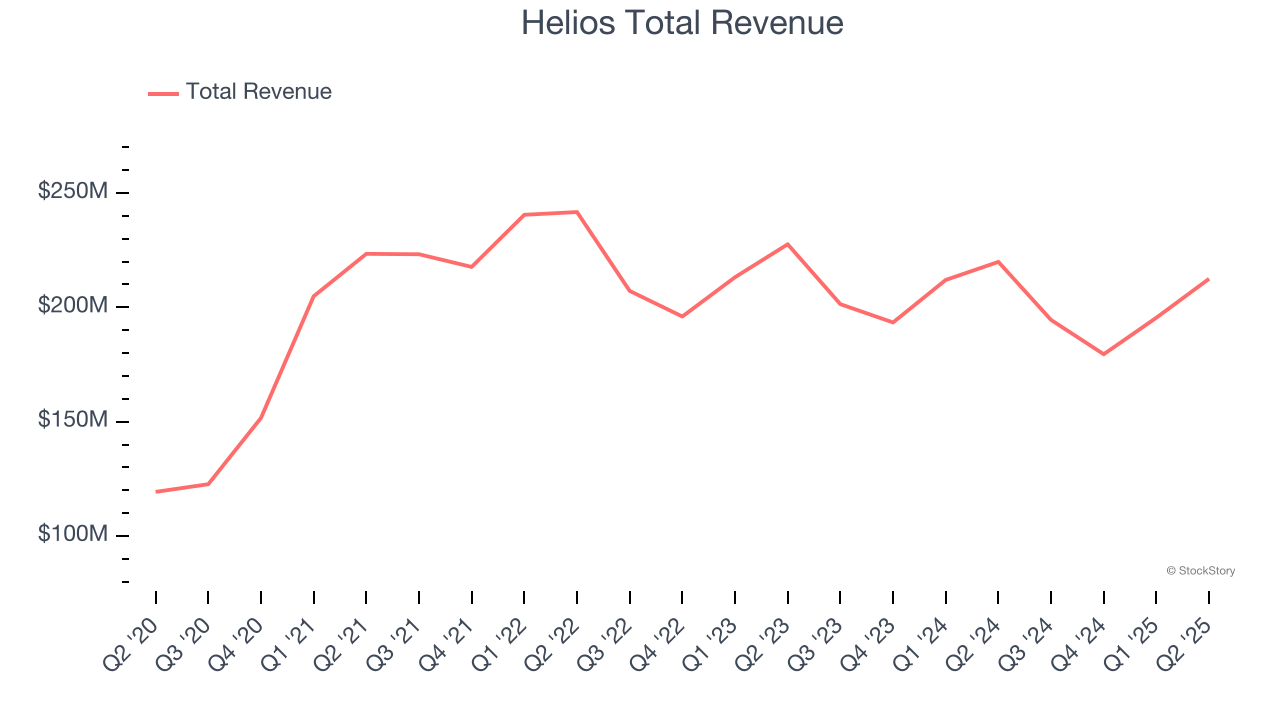

Best Q2: Helios (NYSE: HLIO)

Founded on the principle of treating others as one wants to be treated, Helios (NYSE: HLIO) designs, manufactures, and sells motion and electronic control components for various sectors.

Helios reported revenues of $212.5 million, down 3.4% year on year, outperforming analysts’ expectations by 5.5%. The business had a stunning quarter with a solid beat of analysts’ organic revenue estimates and EPS guidance for next quarter exceeding analysts’ expectations.

Helios pulled off the biggest analyst estimates beat and highest full-year guidance raise among its peers. The market seems happy with the results as the stock is up 43% since reporting. It currently trades at $52.68.

Is now the time to buy Helios? Access our full analysis of the earnings results here, it’s free.

Weakest Q2: Graco (NYSE: GGG)

Founded in 1926, Graco (NYSE: GGG) is an industrial company specializing in the development and manufacturing of fluid-handling systems and products.

Graco reported revenues of $571.8 million, up 3.4% year on year, falling short of analysts’ expectations by 3.1%. It was a disappointing quarter as it posted a significant miss of analysts’ adjusted operating income estimates and a significant miss of analysts’ EPS estimates.

Graco delivered the weakest performance against analyst estimates in the group. As expected, the stock is down 3% since the results and currently trades at $84.54.

Read our full analysis of Graco’s results here.

ITT (NYSE: ITT)

Playing a crucial role in the development of the first transatlantic television transmission in 1956, ITT (NYSE: ITT) provides motion and fluid handling equipment for various industries

ITT reported revenues of $972.4 million, up 7.3% year on year. This print topped analysts’ expectations by 2.6%. It was a strong quarter as it also put up a solid beat of analysts’ organic revenue estimates and a decent beat of analysts’ adjusted operating income estimates.

The stock is up 6% since reporting and currently trades at $169.15.

Read our full, actionable report on ITT here, it’s free.

Ingersoll Rand (NYSE: IR)

Started with the invention of the steam drill, Ingersoll Rand (NYSE: IR) provides mission-critical air, gas, liquid, and solid flow creation solutions.

Ingersoll Rand reported revenues of $1.89 billion, up 4.6% year on year. This result surpassed analysts’ expectations by 2.4%. Overall, it was a very strong quarter as it also recorded a solid beat of analysts’ adjusted operating income estimates and full-year EBITDA guidance slightly topping analysts’ expectations.

The stock is down 8% since reporting and currently trades at $77.94.

Read our full, actionable report on Ingersoll Rand here, it’s free.

Market Update

Thanks to the Fed’s series of rate hikes in 2022 and 2023, inflation has cooled significantly from its post-pandemic highs, drawing closer to the 2% goal. This disinflation has occurred without severely impacting economic growth, suggesting the success of a soft landing. The stock market thrived in 2024, spurred by recent rate cuts (0.5% in September and 0.25% in November), and a notable surge followed Donald Trump’s presidential election win in November, propelling indices to historic highs. Nonetheless, the outlook for 2025 remains clouded by potential trade policy changes and corporate tax discussions, which could impact business confidence and growth. The path forward holds both optimism and caution as new policies take shape.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.