Genuine Parts trades at $124.12 and has moved in lockstep with the market. Its shares have returned 6.9% over the last six months while the S&P 500 has gained 5.6%.

Is now the time to buy Genuine Parts, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Is Genuine Parts Not Exciting?

We're cautious about Genuine Parts. Here are three reasons why there are better opportunities than GPC and a stock we'd rather own.

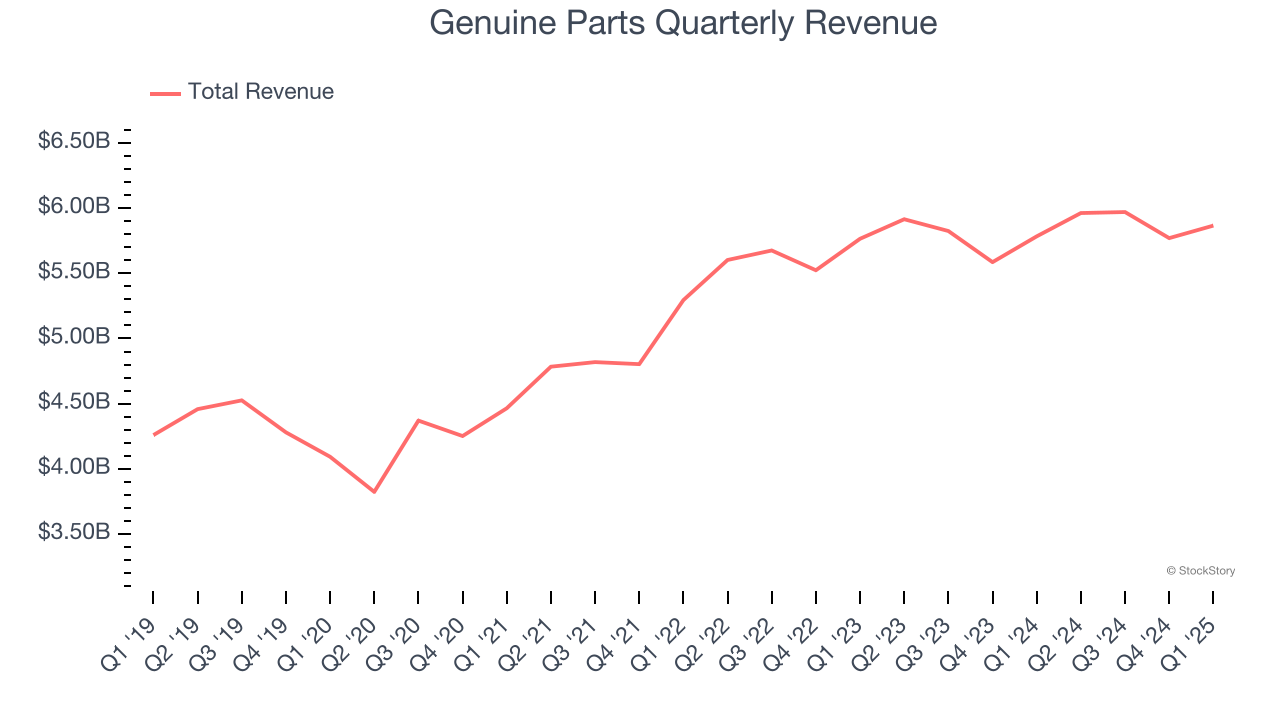

1. Long-Term Revenue Growth Disappoints

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Regrettably, Genuine Parts’s sales grew at a sluggish 4.2% compounded annual growth rate over the last six years. This was below our standard for the consumer retail sector.

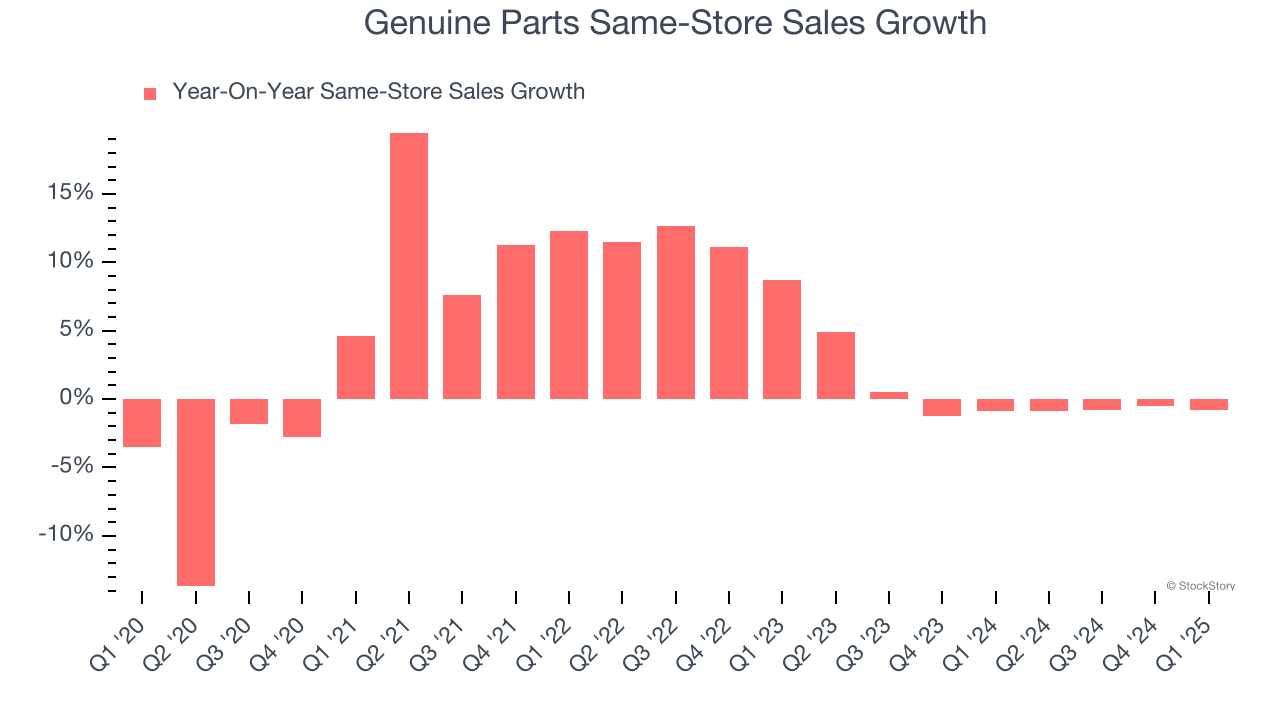

2. Flat Same-Store Sales Indicate Weak Demand

Same-store sales is an industry measure of whether revenue is growing at existing stores, and it is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Genuine Parts’s demand within its existing locations has barely increased over the last two years as its same-store sales were flat.

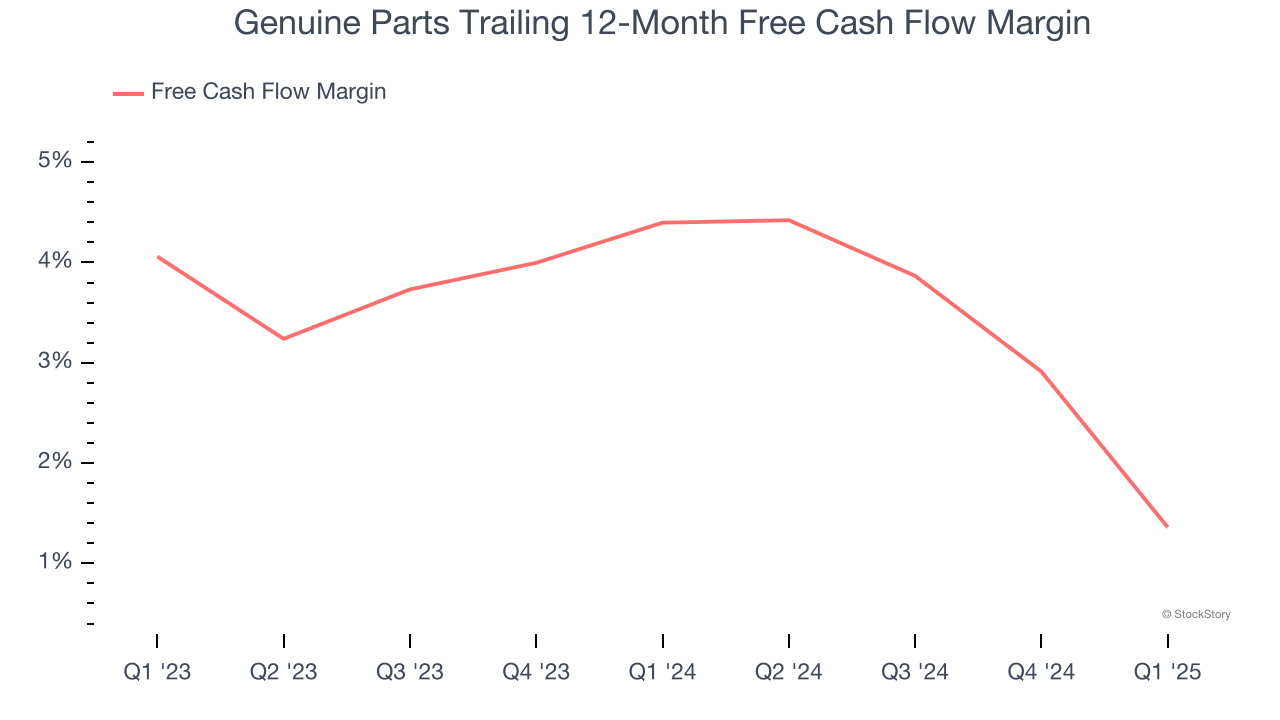

3. Free Cash Flow Margin Dropping

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Genuine Parts’s margin dropped by 3 percentage points over the last year. This decrease came from the higher costs associated with opening more stores.

Final Judgment

Genuine Parts isn’t a terrible business, but it doesn’t pass our quality test. That said, the stock currently trades at 15.2× forward P/E (or $124.12 per share). Investors with a higher risk tolerance might like the company, but we think the potential downside is too great. We're pretty confident there are more exciting stocks to buy at the moment. Let us point you toward one of Charlie Munger’s all-time favorite businesses.

Stocks We Like More Than Genuine Parts

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.