As the Q1 earnings season comes to a close, it’s time to take stock of this quarter’s best and worst performers in the traditional fast food industry, including Krispy Kreme (NASDAQ: DNUT) and its peers.

Traditional fast-food restaurants are renowned for their speed and convenience, boasting menus filled with familiar and budget-friendly items. Their reputations for on-the-go consumption make them favored destinations for individuals and families needing a quick meal. This class of restaurants, however, is fighting the perception that their meals are unhealthy and made with inferior ingredients, a battle that's especially relevant today given the consumers increasing focus on health and wellness.

The 14 traditional fast food stocks we track reported a slower Q1. As a group, revenues missed analysts’ consensus estimates by 1.3% while next quarter’s revenue guidance was in line.

While some traditional fast food stocks have fared somewhat better than others, they have collectively declined. On average, share prices are down 2.3% since the latest earnings results.

Krispy Kreme (NASDAQ: DNUT)

Famous for its Original Glazed doughnuts and parent company of Insomnia Cookies, Krispy Kreme (NASDAQ: DNUT) is one of the most beloved and well-known fast-food chains in the world.

Krispy Kreme reported revenues of $375.2 million, down 15.3% year on year. This print fell short of analysts’ expectations by 2.2%. Overall, it was a softer quarter for the company with a significant miss of analysts’ EBITDA estimates.

“Our ability to become a bigger Krispy Kreme requires that we become better, and we are taking swift and decisive action to pay down debt, de-leverage the balance sheet and drive sustainable, profitable growth,” said Krispy Kreme CEO, Josh Charlesworth.

Krispy Kreme delivered the slowest revenue growth of the whole group. Unsurprisingly, the stock is down 29.6% since reporting and currently trades at $3.03.

Read our full report on Krispy Kreme here, it’s free.

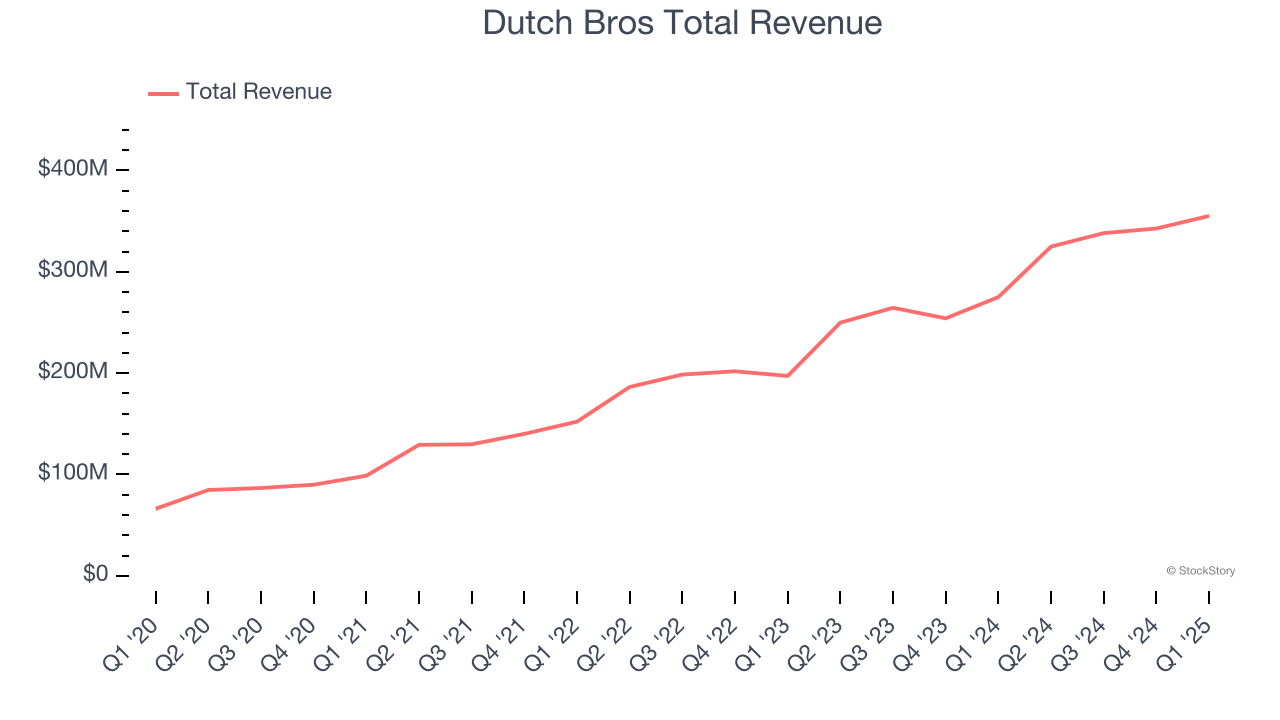

Best Q1: Dutch Bros (NYSE: BROS)

Started in 1992 by two brothers as a single pushcart, Dutch Bros (NYSE: BROS) is a dynamic coffee chain that’s captured the hearts of coffee enthusiasts across the United States.

Dutch Bros reported revenues of $355.2 million, up 29.1% year on year, outperforming analysts’ expectations by 3%. The business had a strong quarter with an impressive beat of analysts’ EBITDA estimates and a solid beat of analysts’ EPS estimates.

Dutch Bros delivered the biggest analyst estimates beat and fastest revenue growth among its peers. The market seems happy with the results as the stock is up 9.9% since reporting. It currently trades at $64.98.

Is now the time to buy Dutch Bros? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: Arcos Dorados (NYSE: ARCO)

Translating to “Golden Arches” in Spanish, Arcos Dorados (NYSE: ARCO) is the master franchisee of the McDonald's brand in Latin America and the Caribbean, responsible for its operations and growth in over 20 countries.

Arcos Dorados reported revenues of $1.08 billion, flat year on year, falling short of analysts’ expectations by 3.6%. It was a disappointing quarter as it posted a significant miss of analysts’ same-store sales and EPS estimates.

As expected, the stock is down 8.8% since the results and currently trades at $7.44.

Read our full analysis of Arcos Dorados’s results here.

Restaurant Brands (NYSE: QSR)

Formed through a strategic merger, Restaurant Brands International (NYSE: QSR) is a multinational corporation that owns three iconic fast-food chains: Burger King, Tim Hortons, and Popeyes.

Restaurant Brands reported revenues of $2.11 billion, up 21.3% year on year. This result missed analysts’ expectations by 1.8%. Overall, it was a softer quarter as it also logged a miss of analysts’ EBITDA estimates and a slight miss of analysts’ same-store sales estimates.

The stock is up 6% since reporting and currently trades at $71.93.

Read our full, actionable report on Restaurant Brands here, it’s free.

Starbucks (NASDAQ: SBUX)

Started by three friends in Seattle’s historic Pike Place Market, Starbucks (NASDAQ: SBUX) is a globally-renowned coffeehouse chain that offers a wide selection of high-quality coffee, beverages, and food items.

Starbucks reported revenues of $8.76 billion, up 2.3% year on year. This print came in 0.6% below analysts' expectations. It was a softer quarter as it also produced a significant miss of analysts’ EBITDA and EPS estimates.

The stock is down 2% since reporting and currently trades at $83.20.

Read our full, actionable report on Starbucks here, it’s free.

Market Update

Thanks to the Fed’s series of rate hikes in 2022 and 2023, inflation has cooled significantly from its post-pandemic highs, drawing closer to the 2% goal. This disinflation has occurred without severely impacting economic growth, suggesting the success of a soft landing. The stock market thrived in 2024, spurred by recent rate cuts (0.5% in September and 0.25% in November), and a notable surge followed Donald Trump’s presidential election win in November, propelling indices to historic highs. Nonetheless, the outlook for 2025 remains clouded by potential trade policy changes and corporate tax discussions, which could impact business confidence and growth. The path forward holds both optimism and caution as new policies take shape.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Growth Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.