Property and casualty insurer Selective Insurance Group (NASDAQ: SIGI) reported revenue ahead of Wall Street’s expectations in Q3 CY2025, with sales up 9.3% year on year to $1.36 billion. Its non-GAAP profit of $1.75 per share was 11.9% below analysts’ consensus estimates.

Is now the time to buy Selective Insurance Group? Find out by accessing our full research report, it’s free for active Edge members.

Selective Insurance Group (SIGI) Q3 CY2025 Highlights:

- Net Premiums Earned: $1.20 billion vs analyst estimates of $1.21 billion (8.3% year-on-year growth, in line)

- Revenue: $1.36 billion vs analyst estimates of $293.1 million (9.3% year-on-year growth, 364% beat)

- Combined Ratio: 98.6% vs analyst estimates of 96.7% (193.3 basis point miss)

- Adjusted EPS: $1.75 vs analyst expectations of $1.99 (11.9% miss)

- Book Value per Share: $54.46 vs analyst estimates of $57.16 (11.6% year-on-year growth, 4.7% miss)

- Market Capitalization: $5.11 billion

“Our full-year combined ratio outlook remains at 97 to 98%. With a 98.3% combined ratio through the first nine months of the year and strong net investment income, we delivered year-to-date operating ROE of 12.6%,” said John J. Marchioni, Chairman, President and Chief Executive Officer.

Company Overview

Founded in 1926 during the early days of automobile insurance, Selective Insurance Group (NASDAQ: SIGI) is a property and casualty insurance company that sells commercial, personal, and excess and surplus lines insurance products through independent agents.

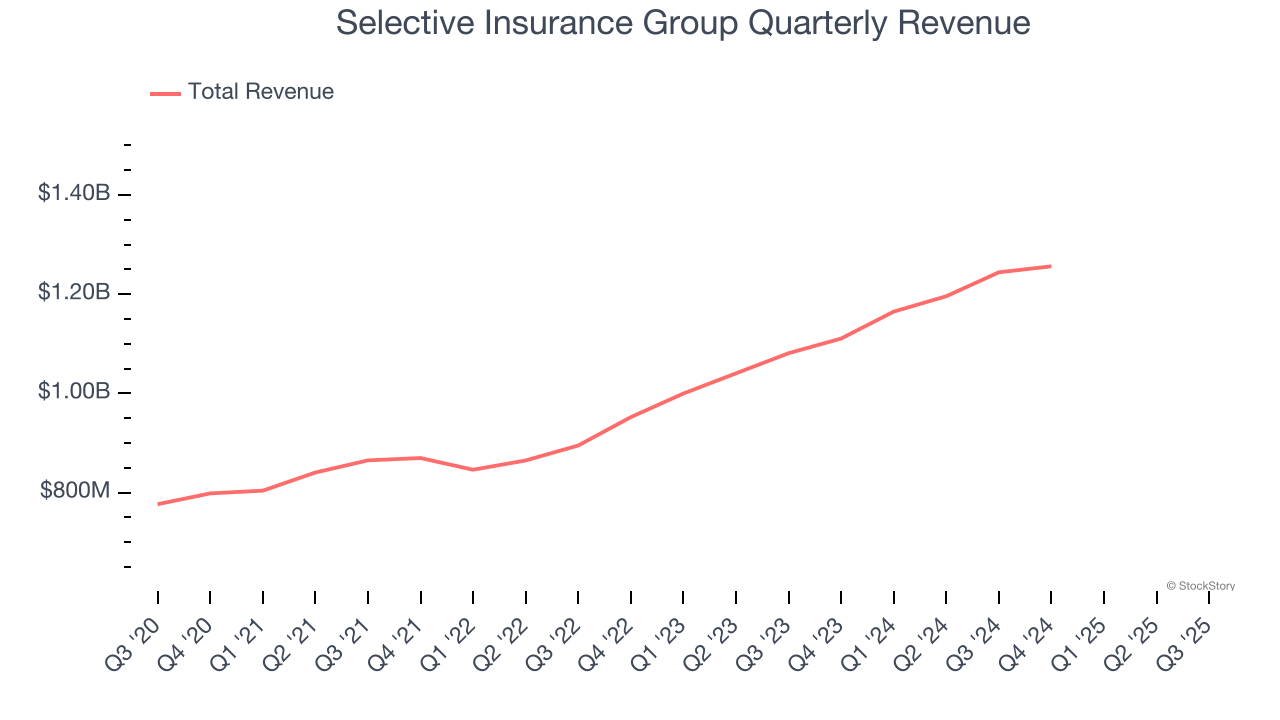

Revenue Growth

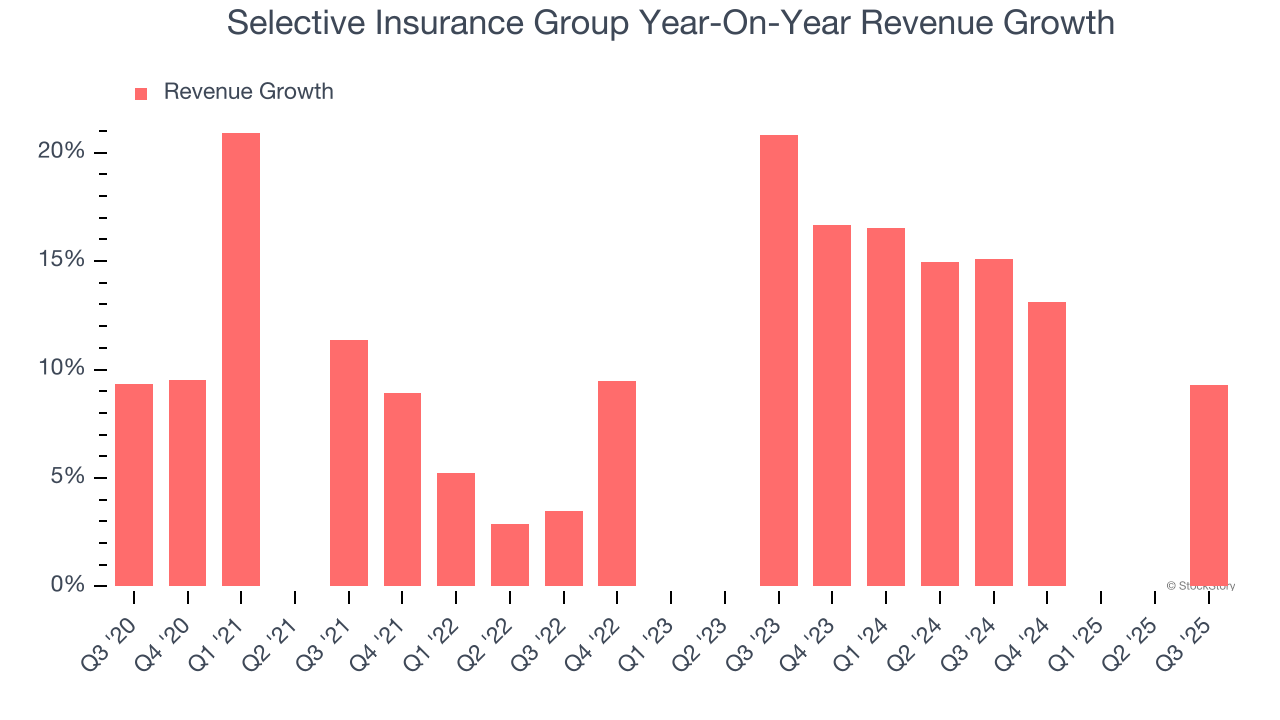

Insurance companies earn revenue from three primary sources: 1) The core insurance business itself, often called underwriting and represented in the income statement as premiums 2) Income from investing the “float” (premiums collected upfront not yet paid out as claims) in assets such as fixed-income assets and equities 3) Fees from various sources such as policy administration, annuities, or other value-added services. Selective Insurance Group’s demand was weak over the last five years as its revenue fell at a 6.2% annual rate. This was below our standards and suggests it’s a lower quality business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Selective Insurance Group’s recent performance shows its demand remained suppressed as its revenue has declined by 29.1% annually over the last two years.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Selective Insurance Group reported year-on-year revenue growth of 9.3%, and its $1.36 billion of revenue exceeded Wall Street’s estimates by 364%.

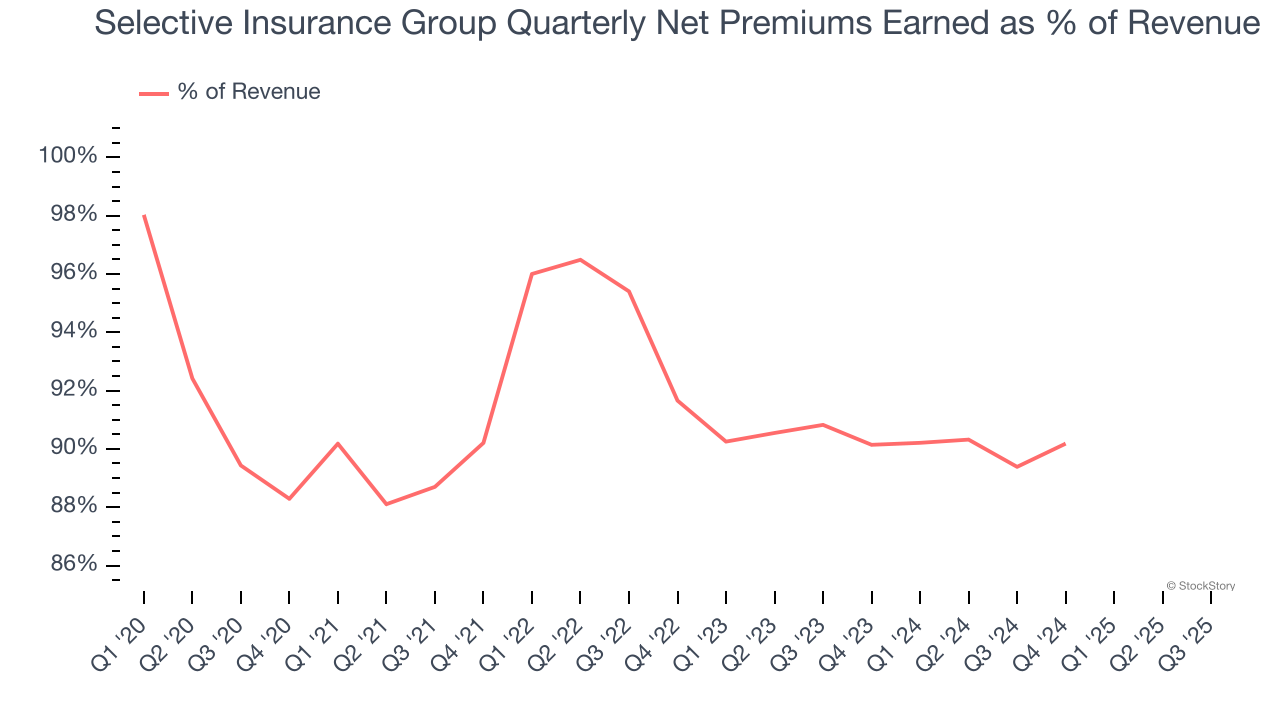

Since the company recorded losses on certain securities, it generated more net premiums earned than revenue during the last five years, meaning Selective Insurance Group lives and dies by its underwriting activities because non-insurance operations barely move the needle.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.Net premiums earned commands greater market attention due to its reliability and consistency, whereas investment and fee income are often seen as more volatile revenue streams that fluctuate with market conditions.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

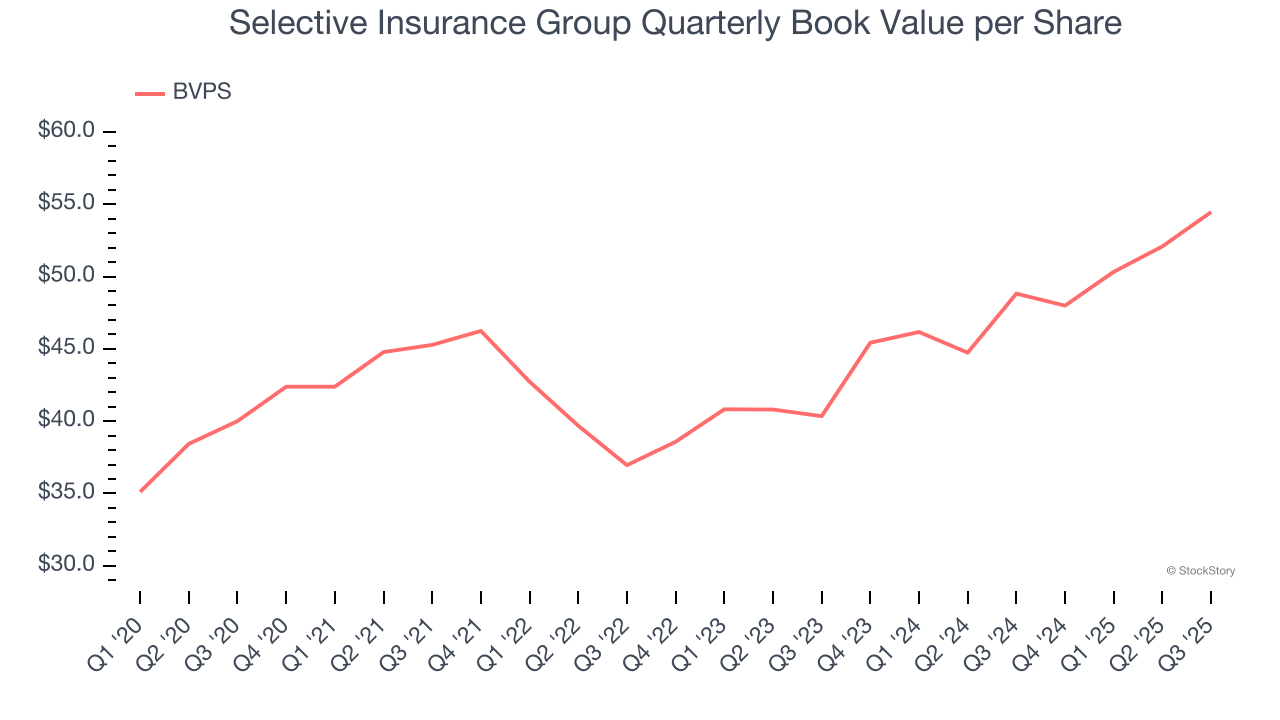

Book Value Per Share (BVPS)

Insurance companies are balance sheet businesses, collecting premiums upfront and paying out claims over time. The float – premiums collected but not yet paid out – are invested, creating an asset base supported by a liability structure. Book value captures this dynamic by measuring:

- Assets (investment portfolio, cash, reinsurance recoverables) - liabilities (claim reserves, debt, future policy benefits)

BVPS is essentially the residual value for shareholders.

We therefore consider BVPS very important to track for insurers and a metric that sheds light on business quality. While other (and more commonly known) per-share metrics like EPS can sometimes be lumpy due to reserve releases or one-time items and can be managed or skewed while still following accounting rules, BVPS reflects long-term capital growth and is harder to manipulate.

Selective Insurance Group’s BVPS grew at a mediocre 6.4% annual clip over the last five years. However, BVPS growth has accelerated recently, growing by 16.2% annually over the last two years from $40.35 to $54.46 per share.

Over the next 12 months, Consensus estimates call for Selective Insurance Group’s BVPS to grow by 16.1% to $57.16, top-notch growth rate.

Key Takeaways from Selective Insurance Group’s Q3 Results

We were impressed by how significantly Selective Insurance Group blew past analysts’ revenue expectations this quarter. On the other hand, its EPS missed and its book value per share fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 5.6% to $76.81 immediately after reporting.

Selective Insurance Group didn’t show it’s best hand this quarter, but does that create an opportunity to buy the stock right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.