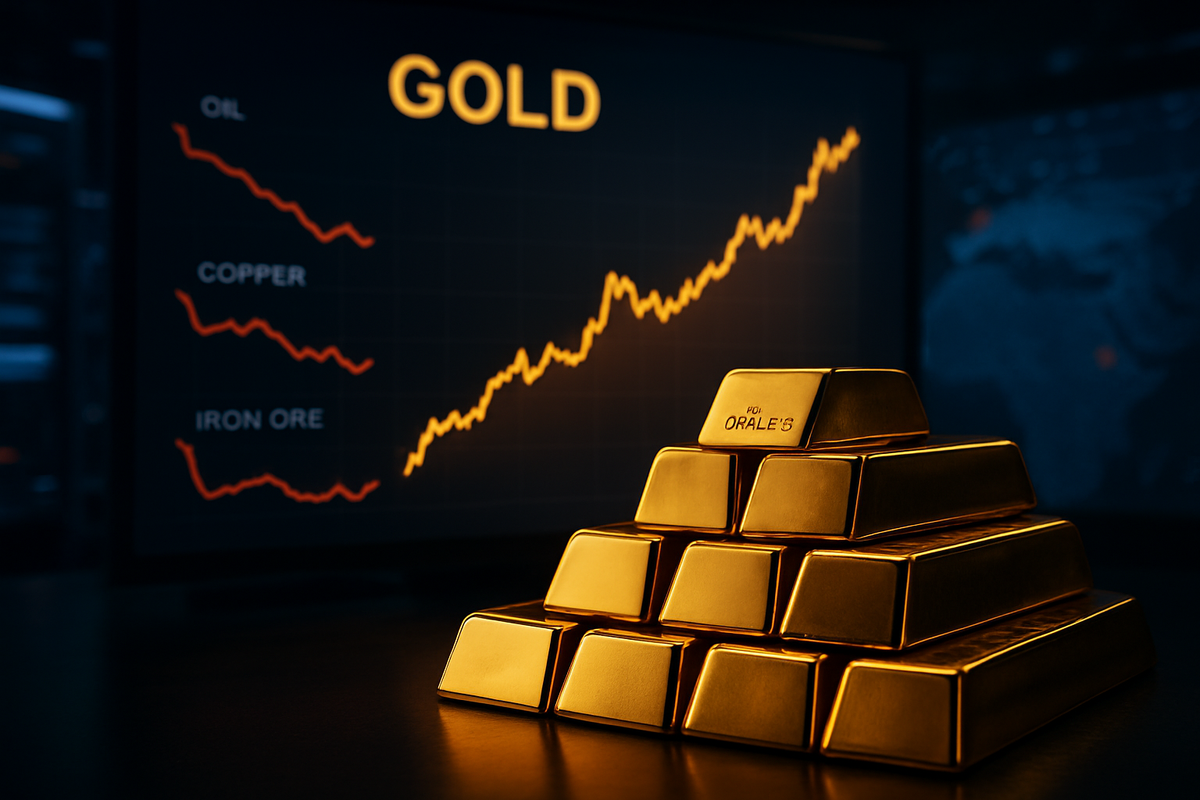

MARCH 17, 2026 — As the global commodity market faces its most significant downturn in years, gold has once again asserted its dominance as the ultimate safe-haven asset. While industrial metals and energy resources are projected to see double-digit declines throughout 2026, the yellow metal is defying the gravity of a cooling global economy, with analysts projecting a 5% rise in prices by year-end. This divergence marks a historic decoupling of precious metals from the broader resource sector, driven by a perfect storm of military conflict and aggressive trade protectionism.

The immediate catalyst for this "golden divergence" is a combination of the escalating U.S.-Iran military conflict and a volatile trade landscape characterized by "weaponized" tariffs. While a structural surplus in oil and a collapse in Chinese industrial demand have sent iron ore and crude prices tumbling, gold has found a solid floor above the $5,000 per ounce mark. As investors flee the uncertainty of equity markets and the potential for supply chain collapses, the demand for "politically neutral" assets has reached a fever pitch, supported by a relentless wave of central bank accumulation.

The Fog of War and the Industrial Retreat

The current market landscape was fundamentally reshaped on February 28, 2026, when a coalition of U.S. and Israeli forces launched targeted airstrikes against Iranian military installations. The subsequent closure of the Strait of Hormuz—a vital artery for 20% of the world's oil and gas—initially spiked energy prices, but the long-term impact has been a flight to quality. While oil prices have since stabilized near $60 per barrel due to record production from non-OPEC sources like the U.S. and Brazil, the geopolitical risk premium has shifted almost entirely into gold.

This geopolitical tension coincides with a bruising "industrial slump" that began in late 2025. China’s property sector, once the primary engine for global metal demand, has continued its structural decline, leading to a projected 7% drop in the World Bank’s aggregate commodity index for 2026. Steel demand is expected to bottom out at 837 million metric tons, leaving industrial commodities like iron ore and copper in a bear market. In this environment, gold's 5% projected growth stands in stark contrast to the 10-12% declines expected in industrial inputs, as the "war premium" outweighs the deflationary pressures of a global manufacturing slowdown.

A Tale of Two Giants: Newmont and Barrick Diverge

The surge in gold prices has created a stark divide among the world’s leading mining firms. Newmont (NYSE: NEM), under the strategic direction of CEO Natascha Viljoen, has emerged as the primary beneficiary of this high-price environment. The company recently reported a massive Q1 2026 earnings beat, with earnings per share (EPS) of $0.72. Newmont’s profit margins are now approaching a staggering 70%, bolstered by the successful integration of its Ahafo North project. By focusing on high-grade assets and rigorous cost controls, Newmont has positioned itself as the "gold standard" for investors looking to capture the upside of the 2026 rally.

In contrast, Barrick Gold (NYSE: GOLD) is grappling with operational headwinds and rising costs. Despite the record price of gold, Barrick’s All-In Sustaining Costs (AISC) have climbed toward $1,950 per ounce, eating into the gains provided by the market. Tensions between the two industry titans reached a breaking point earlier this month when Newmont issued a "Notice of Default" to Barrick regarding the management of their Nevada Gold Mines (NGM) joint venture. This legal rift has introduced a layer of corporate uncertainty for Barrick, as investors worry that operational mismanagement could prevent the company from fully capitalizing on the safest haven in the market.

De-Dollarization and the Central Bank Pillar

Beyond the headlines of war and corporate infighting, a deeper structural shift is supporting gold: the aggressive "de-dollarization" efforts by global central banks. The U.S. administration’s pivot to a 15% blanket levy on imports—following the Supreme Court’s striking down of earlier "emergency" tariff authorities—has caused a rift in international trade. As trade policy becomes increasingly unpredictable, central banks in emerging markets are diversifying away from the U.S. dollar at a record pace.

Central bank hoarding remains a critical pillar of support for the $5,000/oz floor. While net purchases saw a slight seasonal dip in January 2026, nations such as Uzbekistan and Malaysia have continued to add significant tonnage to their reserves. Most notably, the Bank of Korea has recently signaled a shift in its conservative reserve policy, announcing plans to invest in gold ETFs for the first time in over a decade. This institutional appetite suggests that even if geopolitical tensions were to cool, the underlying demand for gold as a reserve asset remains historically high, providing a safety net that industrial commodities simply do not possess.

Navigating the "Higher-for-Longer" Horizon

Looking forward, the path for gold will be dictated by the duration of the Strait of Hormuz closure and the Federal Reserve's response to energy-driven inflation. Markets are currently pricing in a "higher-for-longer" interest rate environment, which traditionally creates a headwind for non-yielding assets like gold. However, the "fear factor" of a broader regional conflict in the Middle East has so far neutralized the impact of high real yields. If the US-Iran conflict escalates into a multi-theater war, some analysts suggest gold could challenge the $6,000 mark by the end of Q3 2026.

Conversely, the main challenge for the gold market will be a potential resolution to trade uncertainties. If the current administration reaches a "grand bargain" with major trading partners to lower the 15% blanket levy, the drive for de-dollarization could lose some of its urgency. Investors should also watch for a "supply chain decoupling" where Western manufacturers move entirely away from Chinese-sourced industrial metals, a move that could ironically create a localized spike in industrial commodity prices, potentially narrowing the performance gap between gold and base metals.

The Outlook: A Fragmented Future

The 2026 commodity slump has proven that gold remains the undisputed king of crisis. Its ability to project a 5% gain while the rest of the resource sector bleeds is a testament to its role as a hedge against both military conflict and economic policy failure. For the market moving forward, the significance of this period lies in the normalization of gold at prices above $5,000, a level that was considered unthinkable just two years ago.

For investors, the key takeaways are clear: margin discipline is paramount. As seen with the divergence between Newmont (NYSE: NEM) and Barrick Gold (NYSE: GOLD), high gold prices do not guarantee universal success in the mining sector. Moving into the second half of 2026, the market will be watching for signs of central bank fatigue and any shifts in the Middle Eastern conflict. For now, the "Golden Age" appears to be more than just a headline; it is the new reality of a fragmented and volatile global economy.

This content is intended for informational purposes only and is not financial advice.