Quarterly earnings results are a good time to check in on a company’s progress, especially compared to its peers in the same sector. Today we are looking at Leggett & Platt (NYSE: LEG) and the best and worst performers in the home furnishings industry.

A healthy housing market is good for furniture demand as more consumers are buying, renting, moving, and renovating. On the other hand, periods of economic weakness or high interest rates discourage home sales and can squelch demand. In addition, home furnishing companies must contend with shifting consumer preferences such as the growing propensity to buy goods online, including big things like mattresses and sofas that were once thought to be immune from e-commerce competition.

The 6 home furnishings stocks we track reported a satisfactory Q2. As a group, revenues were in line with analysts’ consensus estimates while next quarter’s revenue guidance was 1% above.

In light of this news, share prices of the companies have held steady as they are up 4% on average since the latest earnings results.

Leggett & Platt (NYSE: LEG)

Founded in 1883, Leggett & Platt (NYSE: LEG) is a diversified manufacturer of products and components for various industries.

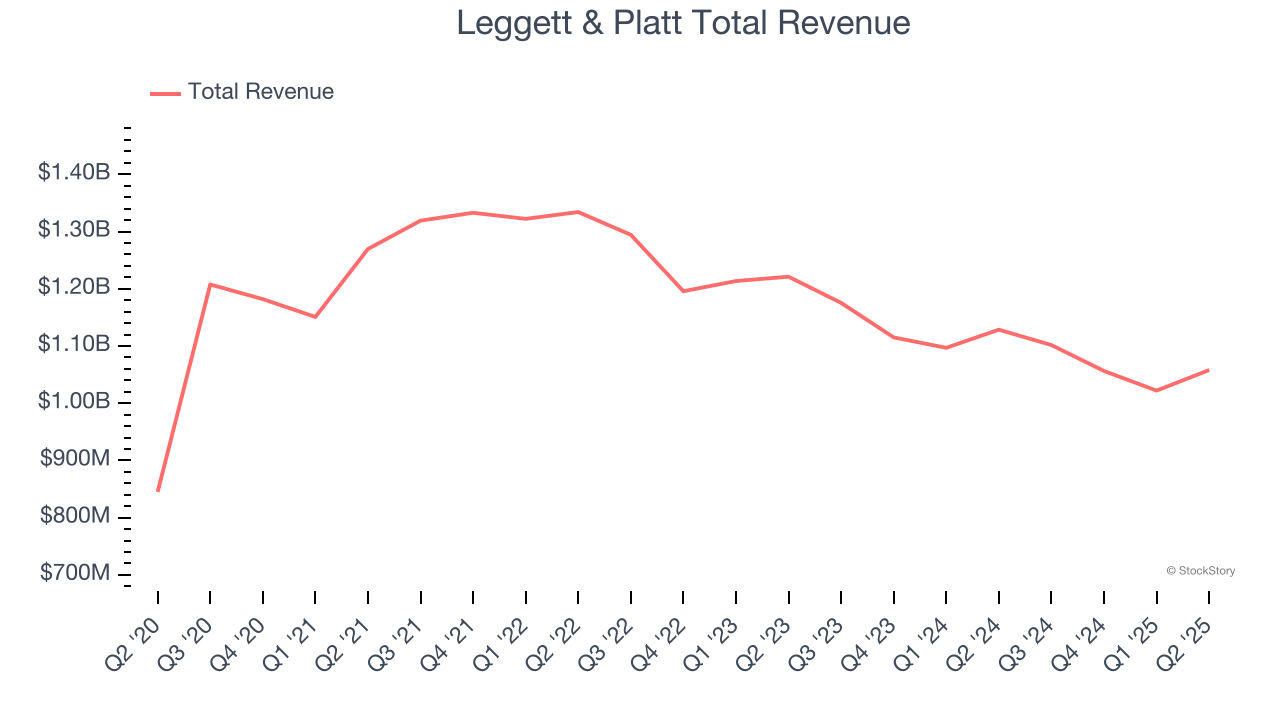

Leggett & Platt reported revenues of $1.06 billion, down 6.3% year on year. This print was in line with analysts’ expectations, but overall, it was a mixed quarter for the company with a decent beat of analysts’ adjusted operating income estimates.

President and CEO Karl Glassman commented, "We are pleased to report another quarter of profitability improvement. We further strengthened our balance sheet by reducing debt and favorably amending our revolving credit facility. We also remain on track to complete the sale of our Aerospace business this year. The continued progress on our strategic initiatives is a direct reflection of the dedication and talent of our employees.

Leggett & Platt delivered the weakest full-year guidance update of the whole group. Unsurprisingly, the stock is down 1.7% since reporting and currently trades at $9.37.

Read our full report on Leggett & Platt here, it’s free.

Best Q2: Purple (NASDAQ: PRPL)

Founded by two brothers, Purple (NASDAQ: PRPL) creates sleep and home comfort products such as mattresses, pillows, and bedding accessories.

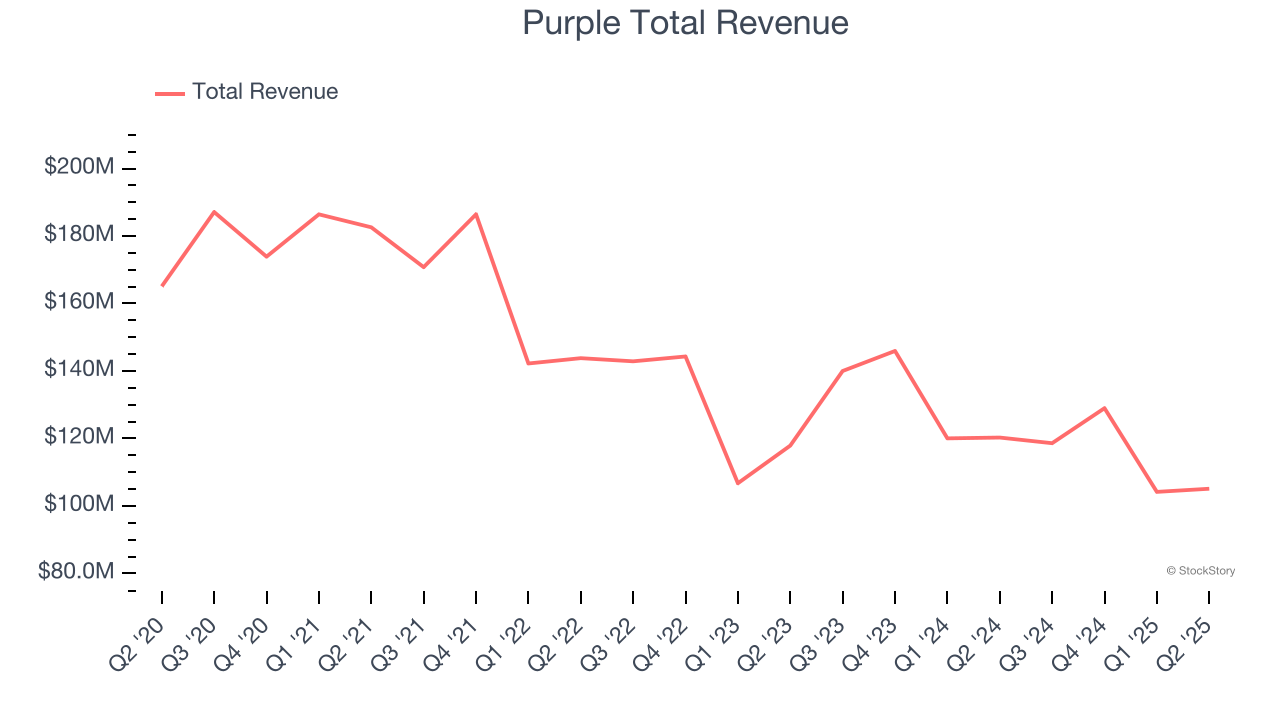

Purple reported revenues of $105.1 million, down 12.6% year on year, in line with analysts’ expectations. The business had an exceptional quarter with a solid beat of analysts’ adjusted operating income estimates and full-year EBITDA guidance exceeding analysts’ expectations.

The market seems happy with the results as the stock is up 23.3% since reporting. It currently trades at $1.05.

Is now the time to buy Purple? Access our full analysis of the earnings results here, it’s free.

Weakest Q2: La-Z-Boy (NYSE: LZB)

The prized possession of every mancave, La-Z-Boy (NYSE: LZB) is a furniture company specializing in recliners, sofas, and seats.

La-Z-Boy reported revenues of $492.2 million, flat year on year, in line with analysts’ expectations. It was a slower quarter as it posted a significant miss of analysts’ EPS and adjusted operating income estimates.

As expected, the stock is down 13.9% since the results and currently trades at $33.70.

Read our full analysis of La-Z-Boy’s results here.

Lovesac (NASDAQ: LOVE)

Known for its oversized, premium beanbags, Lovesac (NASDAQ: LOVE) is a specialty furniture brand selling modular furniture.

Lovesac reported revenues of $160.5 million, up 2.5% year on year. This print was in line with analysts’ expectations. It was a strong quarter as it also produced a beat of analysts’ EPS and EBITDA estimates.

Lovesac scored the highest full-year guidance raise among its peers. The stock is down 12.9% since reporting and currently trades at $18.10.

Read our full, actionable report on Lovesac here, it’s free.

Mohawk Industries (NYSE: MHK)

Established in 1878, Mohawk Industries (NYSE: MHK) is a leading producer of floor-covering products for both residential and commercial applications.

Mohawk Industries reported revenues of $2.80 billion, flat year on year. This number beat analysts’ expectations by 2.2%. Taking a step back, it was a satisfactory quarter as it also produced an impressive beat of analysts’ organic revenue estimates but EPS guidance for next quarter missing analysts’ expectations.

Mohawk Industries pulled off the biggest analyst estimates beat among its peers. The stock is up 12.6% since reporting and currently trades at $130.66.

Read our full, actionable report on Mohawk Industries here, it’s free.

Market Update

Thanks to the Fed’s series of rate hikes in 2022 and 2023, inflation has cooled significantly from its post-pandemic highs, drawing closer to the 2% goal. This disinflation has occurred without severely impacting economic growth, suggesting the success of a soft landing. The stock market thrived in 2024, spurred by recent rate cuts (0.5% in September and 0.25% in November), and a notable surge followed Donald Trump’s presidential election win in November, propelling indices to historic highs. Nonetheless, the outlook for 2025 remains clouded by potential trade policy changes and corporate tax discussions, which could impact business confidence and growth. The path forward holds both optimism and caution as new policies take shape.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Quality Compounder Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.