Earnings results often indicate what direction a company will take in the months ahead. With Q2 behind us, let’s have a look at FTAI Aviation (NASDAQ: FTAI) and its peers.

Supply chain and inventory management are themes that grew in focus after COVID wreaked havoc on the global movement of raw materials and components. Distributors that boast a reliable selection of products–everything from hardhats and fasteners for jet engines to ceiling systems–and quickly deliver goods to customers can benefit from this theme. While e-commerce hasn’t disrupted industrial distribution as much as consumer retail, it is still a real threat, forcing investment in omnichannel capabilities to better interact with customers. Additionally, distributors are at the whim of economic cycles that impact the capital spending and construction projects that can juice demand.

The 26 industrial distributors stocks we track reported a strong Q2. As a group, revenues beat analysts’ consensus estimates by 1.5% while next quarter’s revenue guidance was 2.6% below.

In light of this news, share prices of the companies have held steady as they are up 4.5% on average since the latest earnings results.

FTAI Aviation (NASDAQ: FTAI)

With a focus on the CFM56 engine that powers Boeing and Airbus’s planes, FTAI Aviation (NASDAQ: FTAI) sells, leases, maintains, and repairs aircraft engines.

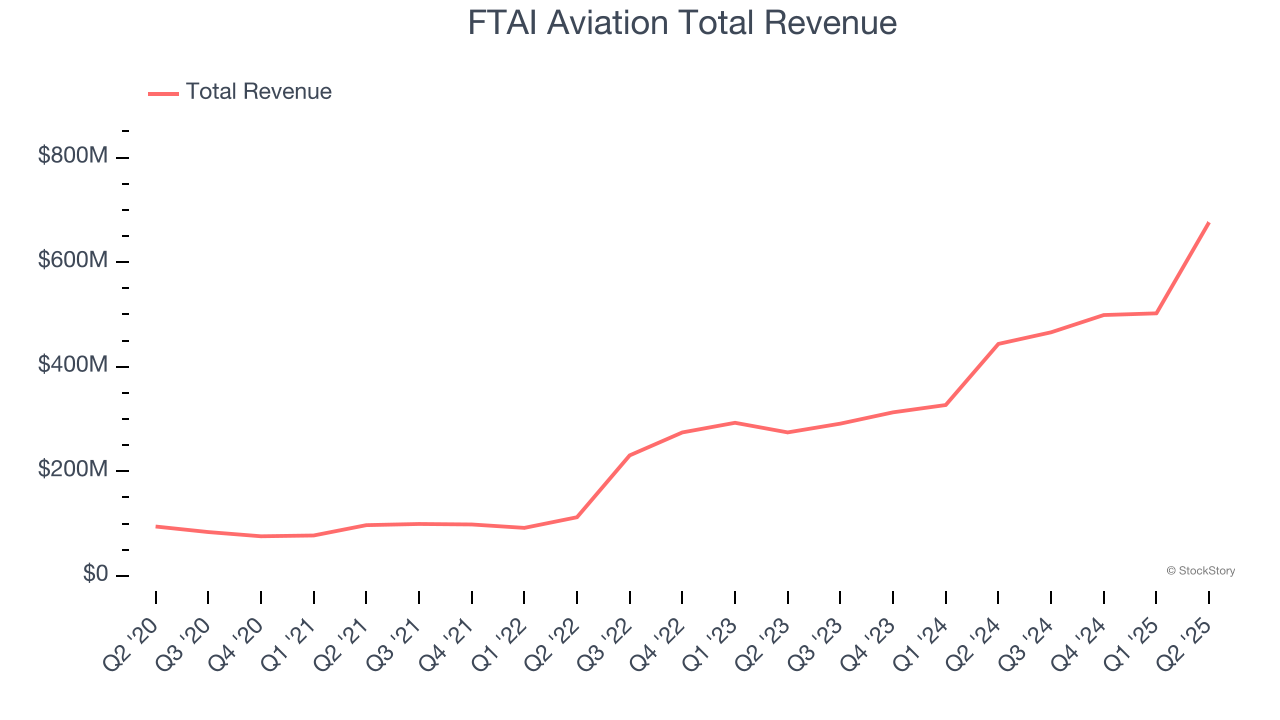

FTAI Aviation reported revenues of $676.2 million, up 52.4% year on year. This print exceeded analysts’ expectations by 5.8%. Overall, it was an incredible quarter for the company with a beat of analysts’ EPS and EBITDA estimates.

“FTAI delivered an excellent quarter, generating over $400 million in positive Adjusted Free Cash Flow,” said Joe Adams, Chairman and CEO(1).

FTAI Aviation scored the fastest revenue growth of the whole group. Unsurprisingly, the stock is up 55.7% since reporting and currently trades at $177.77.

Transcat (NASDAQ: TRNS)

Serving the pharmaceutical, industrial manufacturing, energy, and chemical process industries, Transcat (NASDAQ: TRNS) provides measurement instruments and supplies.

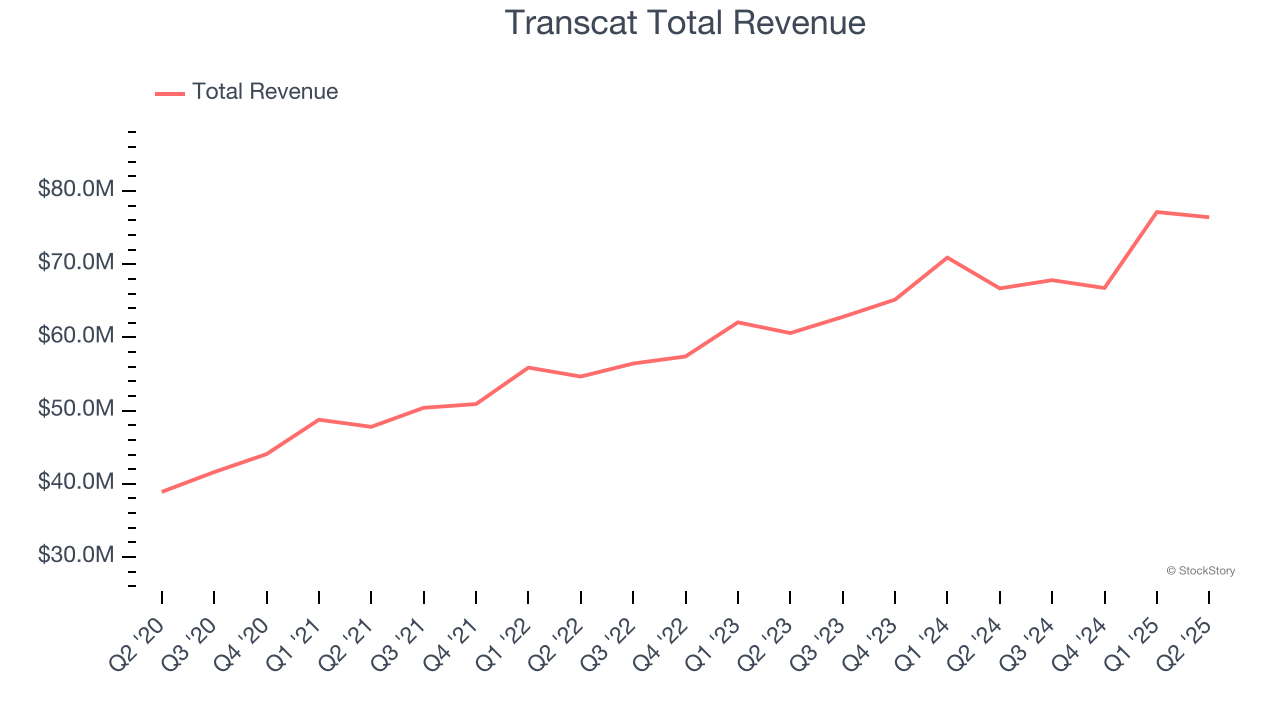

Transcat reported revenues of $76.42 million, up 14.6% year on year, outperforming analysts’ expectations by 5.7%. The business had an incredible quarter with a beat of analysts’ EPS and EBITDA estimates.

Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 3.8% since reporting. It currently trades at $75.45.

Is now the time to buy Transcat? Access our full analysis of the earnings results here, it’s free.

Weakest Q2: Watsco (NYSE: WSO)

Originally a manufacturing company, Watsco (NYSE: WSO) today only distributes air conditioning, heating, and refrigeration equipment, as well as related parts and supplies.

Watsco reported revenues of $2.06 billion, down 3.6% year on year, falling short of analysts’ expectations by 7.2%. It was a disappointing quarter as it posted a significant miss of analysts’ adjusted operating income estimates and a significant miss of analysts’ EBITDA estimates.

Watsco delivered the weakest performance against analyst estimates in the group. As expected, the stock is down 16.1% since the results and currently trades at $389.70.

Read our full analysis of Watsco’s results here.

Richardson Electronics (NASDAQ: RELL)

Founded in 1947, Richardson Electronics (NASDAQ: RELL) is a distributor of power grid and microwave tubes as well as consumables related to those products.

Richardson Electronics reported revenues of $51.89 million, up 9.5% year on year. This number lagged analysts' expectations by 3.7%. Zooming out, it was actually a strong quarter as it produced a beat of analysts’ EPS estimates and an impressive beat of analysts’ EBITDA estimates.

The stock is up 2.2% since reporting and currently trades at $10.01.

Read our full, actionable report on Richardson Electronics here, it’s free.

MRC Global (NYSE: MRC)

Producing bomb casings and tracks for vehicles during WWII, MRC (NYSE: MRC) offers pipes, valves, and fitting products for various industries.

MRC Global reported revenues of $798 million, flat year on year. This print topped analysts’ expectations by 1.7%. It was a strong quarter as it also recorded a solid beat of analysts’ EBITDA estimates and EPS in line with analysts’ estimates.

The stock is flat since reporting and currently trades at $14.25.

Read our full, actionable report on MRC Global here, it’s free.

Market Update

Thanks to the Fed’s rate hikes in 2022 and 2023, inflation has been on a steady path downward, easing back toward that 2% sweet spot. Fortunately (miraculously to some), all this tightening didn’t send the economy tumbling into a recession, so here we are, cautiously celebrating a soft landing. The cherry on top? Recent rate cuts (half a point in September 2024, a quarter in November) have propped up markets, especially after Trump’s November win lit a fire under major indices and sent them to all-time highs. However, there’s still plenty to ponder — tariffs, corporate tax cuts, and what 2025 might hold for the economy.

Want to invest in winners with rock-solid fundamentals? Check out our Hidden Gem Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.