Since March 2025, Columbia Financial has been in a holding pattern, posting a small return of 0.9% while floating around $15.51. The stock also fell short of the S&P 500’s 15.6% gain during that period.

Is now the time to buy Columbia Financial, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Do We Think Columbia Financial Will Underperform?

We're cautious about Columbia Financial. Here are three reasons why CLBK doesn't excite us and a stock we'd rather own.

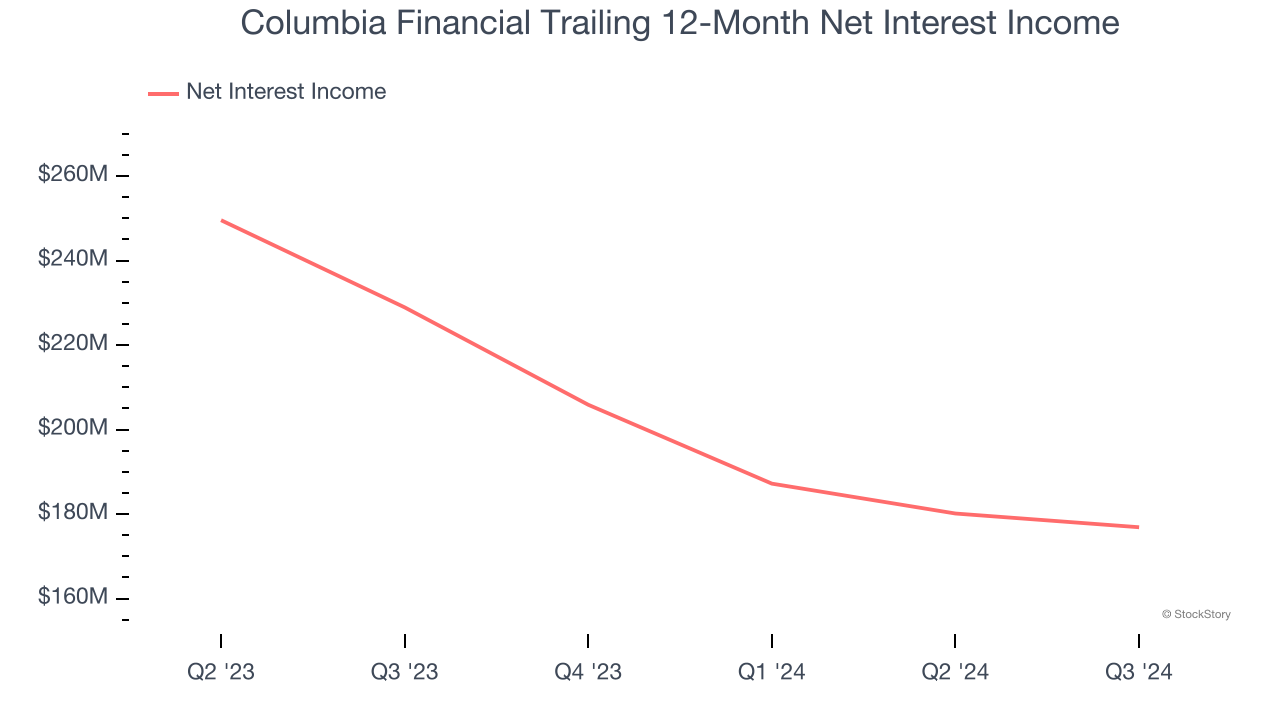

1. Net Interest Income Hits a Plateau

Net interest income commands greater market attention due to its reliability and consistency, whereas one-time fees are often seen as lower-quality revenue that lacks the same dependable characteristics.

Columbia Financial’s net interest income was flat over the last five years, much worse than the broader banking industry. This shows that lending underperformed its other business lines.

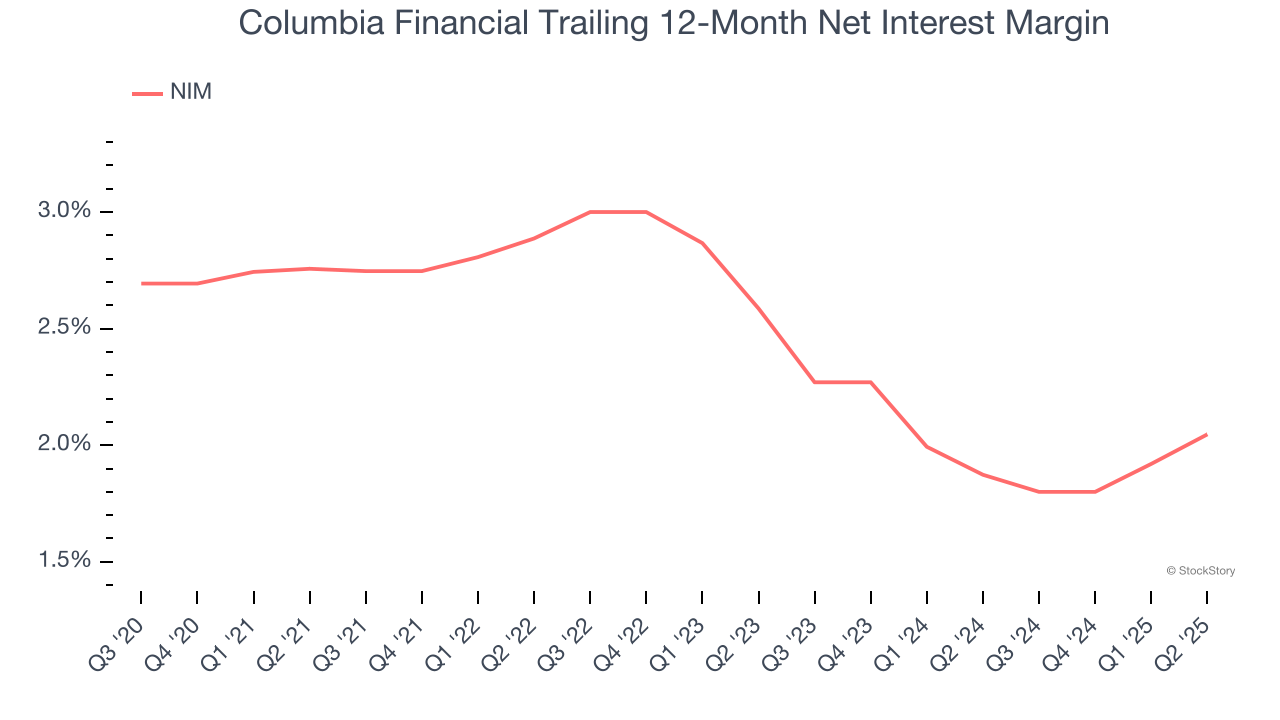

2. Net Interest Margin Dropping

Net interest margin (NIM) serves as a critical gauge of a bank's fundamental profitability by showing the spread between interest income and interest expenses. It's essential for understanding whether a firm can sustainably generate returns from its lending operations.

Over the past two years, Columbia Financial’s net interest margin averaged 2%. Its margin also contracted by 54 basis points (100 basis points = 1 percentage point) over that period.

This decline was a headwind for its net interest income. While prevailing rates are a major determinant of net interest margin changes over time, the decline could mean that Columbia Financial either faced competition for loans and deposits or experienced a negative mix shift in its balance sheet composition.

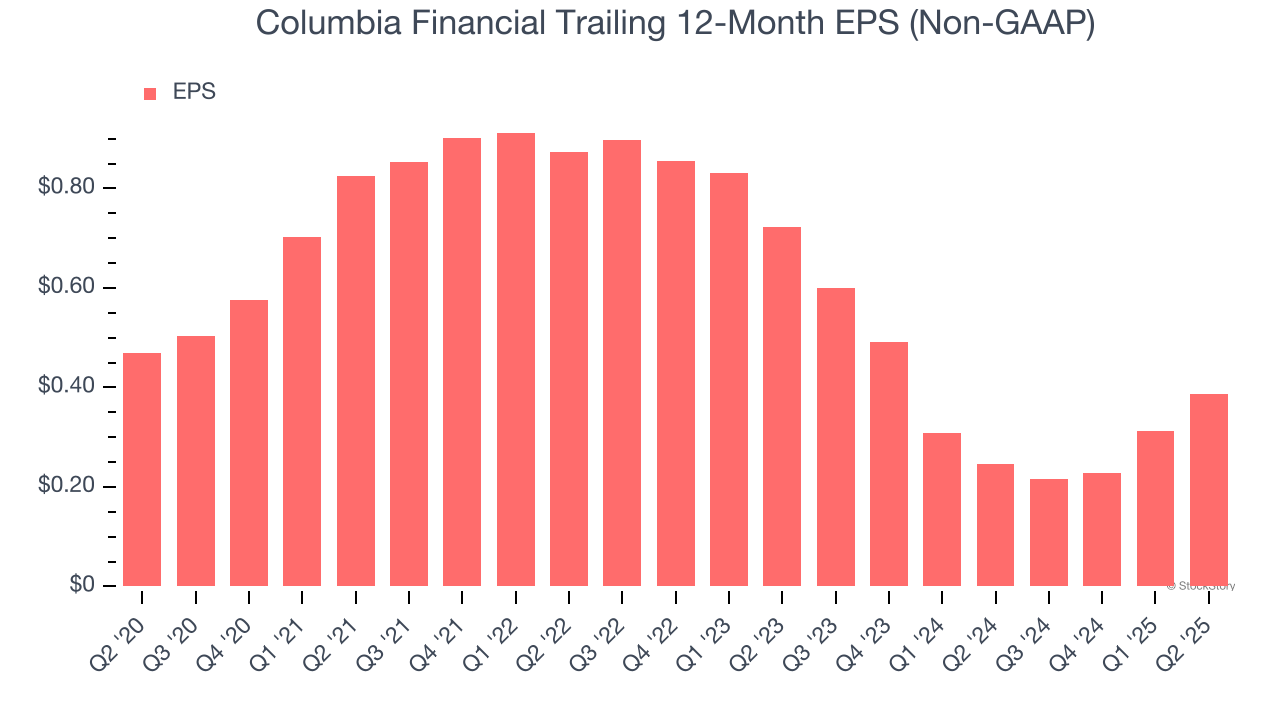

3. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for Columbia Financial, its EPS declined by 3.7% annually over the last five years while its revenue grew by 2.3%. This tells us the company became less profitable on a per-share basis as it expanded.

Final Judgment

Columbia Financial doesn’t pass our quality test. With its shares underperforming the market lately, the stock trades at 1.4× forward P/B (or $15.51 per share). This valuation tells us a lot of optimism is priced in - we think other companies feature superior fundamentals at the moment. We’d suggest looking at one of our top software and edge computing picks.

High-Quality Stocks for All Market Conditions

Trump’s April 2025 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.