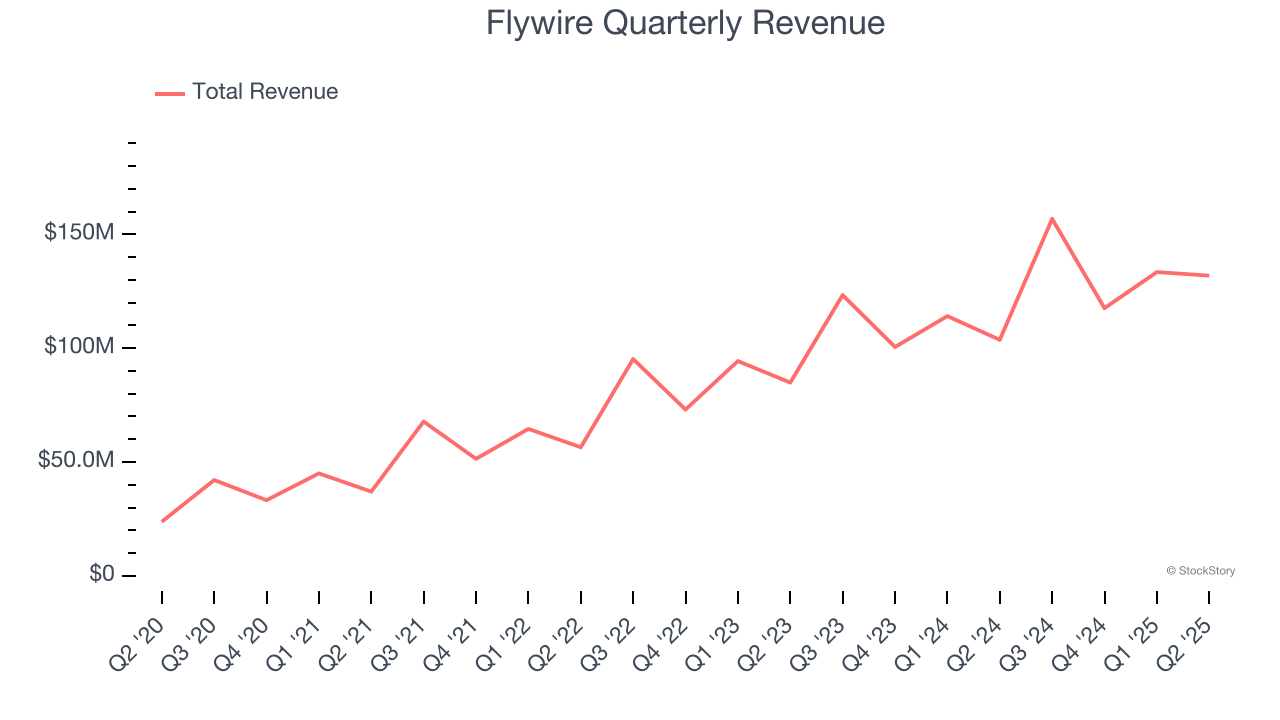

Cross border payment processor Flywire (NASDAQ: FLYW) reported Q2 CY2025 results beating Wall Street’s revenue expectations, with sales up 27.2% year on year to $131.9 million. The company expects next quarter’s revenue to be around $183.5 million, close to analysts’ estimates. Its GAAP loss of $0.10 per share was 48.3% below analysts’ consensus estimates.

Is now the time to buy Flywire? Find out by accessing our full research report, it’s free.

Flywire (FLYW) Q2 CY2025 Highlights:

- Revenue: $131.9 million vs analyst estimates of $125.4 million (27.2% year-on-year growth, 5.2% beat)

- EPS (GAAP): -$0.10 vs analyst expectations of -$0.07 (48.3% miss)

- Adjusted EBITDA: $16.6 million vs analyst estimates of $10.18 million (12.6% margin, 63.1% beat)

- Revenue Guidance for Q3 CY2025 is $183.5 million at the midpoint, roughly in line with what analysts were expecting

- Revenue Guidance for Q3 CY2025 is $183.5 million at the midpoint, roughly in line with what analysts were expecting

- Operating Margin: -6.8%, up from -15.2% in the same quarter last year

- Free Cash Flow was $21.45 million, up from -$80.39 million in the previous quarter

- Market Capitalization: $1.26 billion

Company Overview

Originally created to process international tuition payments for universities, Flywire (NASDAQ: FLYW) is a cross border payments processor and software platform focusing on complex, high-value transactions like education, healthcare and B2B payments.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last three years, Flywire grew its sales at an impressive 31% compounded annual growth rate. Its growth beat the average software company and shows its offerings resonate with customers.

This quarter, Flywire reported robust year-on-year revenue growth of 27.2%, and its $131.9 million of revenue topped Wall Street estimates by 5.2%. Company management is currently guiding for a 17% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 16.8% over the next 12 months, a deceleration versus the last three years. Despite the slowdown, this projection is noteworthy and implies the market sees success for its products and services.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

Flywire’s recent customer acquisition efforts haven’t yielded returns as its CAC payback period was negative this quarter, meaning its incremental sales and marketing investments outpaced its revenue. The company’s inefficiency indicates it operates in a competitive market and must continue investing to grow.

Key Takeaways from Flywire’s Q2 Results

Revenue and EBITDA beat by convincing amounts. Looking ahead, the company reaffirmed full-year revenue growth guidance but increased EBITDA margin guidance, which means there is increasing efficiency in the business. Overall, we think this was a solid quarter with some key areas of upside. The stock traded up 20.3% to $12.45 immediately after reporting.

Flywire may have had a good quarter, but does that mean you should invest right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.