Looking back on regional banks stocks’ Q2 earnings, we examine this quarter’s best and worst performers, including Preferred Bank (NASDAQ: PFBC) and its peers.

Regional banks, financial institutions operating within specific geographic areas, serve as intermediaries between local depositors and borrowers. They benefit from rising interest rates that improve net interest margins (the difference between loan yields and deposit costs), digital transformation reducing operational expenses, and local economic growth driving loan demand. However, these banks face headwinds from fintech competition, deposit outflows to higher-yielding alternatives, credit deterioration (increasing loan defaults) during economic slowdowns, and regulatory compliance costs. Recent concerns about regional bank stability following high-profile failures and significant commercial real estate exposure present additional challenges.

The 98 regional banks stocks we track reported a satisfactory Q2. As a group, revenues were in line with analysts’ consensus estimates.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 5.7% since the latest earnings results.

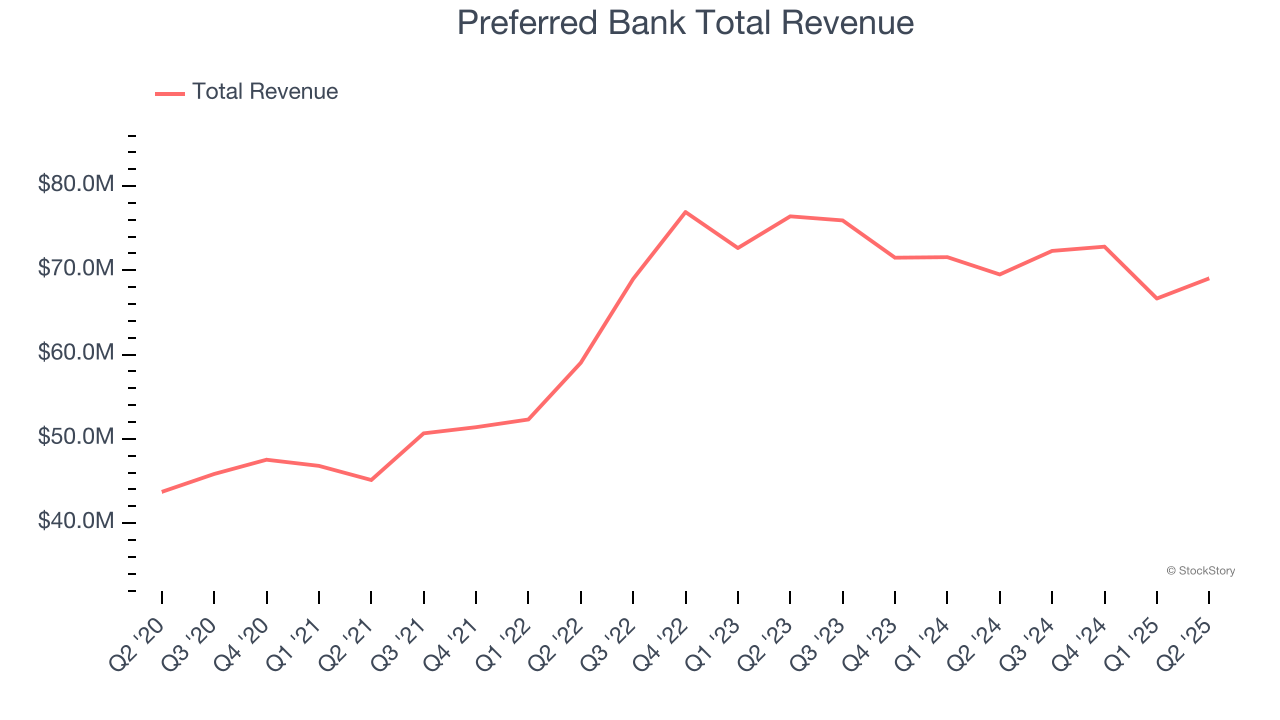

Preferred Bank (NASDAQ: PFBC)

Founded in 1991 with a focus on serving the Pacific Rim community in Southern California, Preferred Bank (NASDAQ: PFBC) is a commercial bank that provides banking products and services to small and mid-sized businesses, entrepreneurs, real estate developers, and high net worth individuals.

Preferred Bank reported revenues of $69.05 million, flat year on year. This print fell short of analysts’ expectations by 2.3%. Overall, it was a slower quarter for the company with EPS in line with analysts’ estimates.

Li Yu, Chairman and CEO, commented, “We are pleased to report our results for the second quarter of 2025. We recorded net income of $32.8 million or $2.52 per fully diluted share. This quarter we had an increase in our loan portfolio of 1.8% (linked quarter), however, deposits only increased slightly. The Bank’s net interest margin improved to 3.85%. Last quarter we reported a net interest margin of 3.75% which was negatively impacted by an outsized interest reversal.

Unsurprisingly, the stock is down 3.7% since reporting and currently trades at $89.07.

Is now the time to buy Preferred Bank? Access our full analysis of the earnings results here, it’s free.

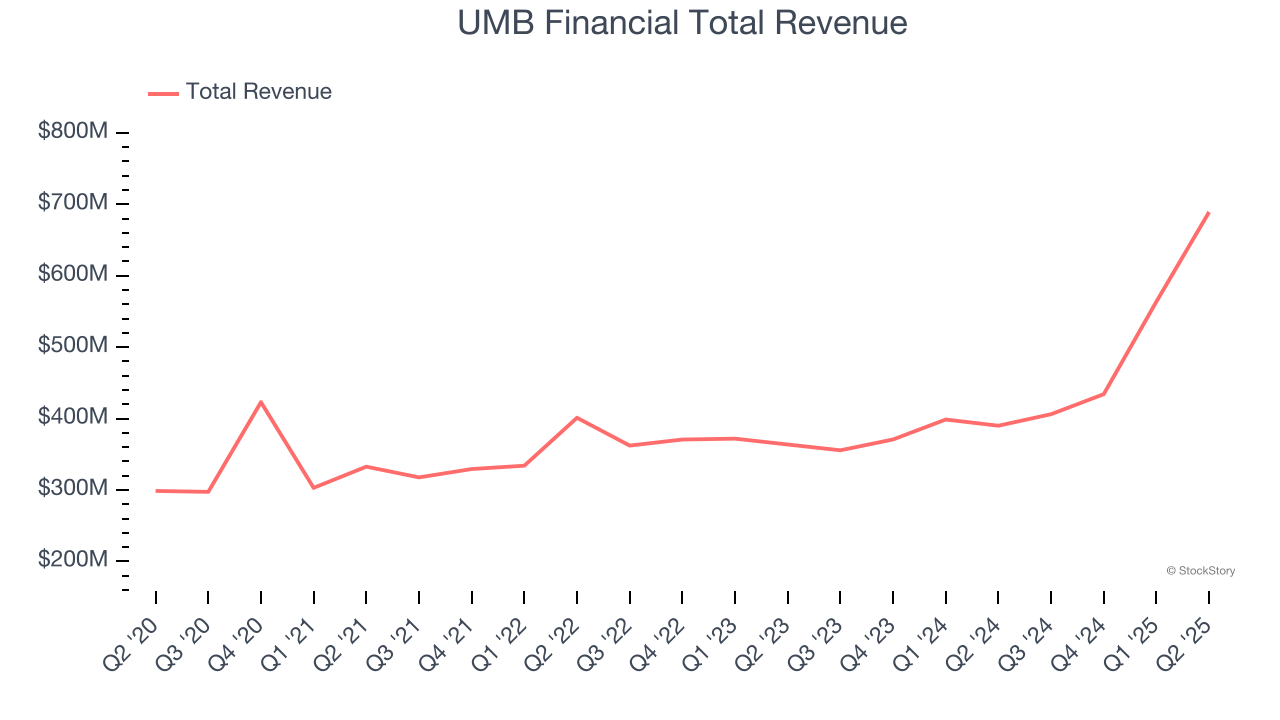

Best Q2: UMB Financial (NASDAQ: UMBF)

With roots dating back to 1913 and a name derived from "United Missouri Bank," UMB Financial (NASDAQ: UMBF) is a financial holding company that provides banking, asset management, and fund services to commercial, institutional, and individual customers.

UMB Financial reported revenues of $689.2 million, up 76.7% year on year, outperforming analysts’ expectations by 8.6%. The business had a stunning quarter with an impressive beat of analysts’ EPS estimates and a solid beat of analysts’ tangible book value per share estimates.

Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 1.2% since reporting. It currently trades at $108.39.

Is now the time to buy UMB Financial? Access our full analysis of the earnings results here, it’s free.

Weakest Q2: Coastal Financial (NASDAQ: CCB)

Pioneering the intersection of traditional banking and financial technology in the Pacific Northwest, Coastal Financial (NASDAQ: CCB) operates as a bank holding company that provides traditional banking services and Banking-as-a-Service (BaaS) solutions to consumers and businesses.

Coastal Financial reported revenues of $119.4 million, down 11.7% year on year, falling short of analysts’ expectations by 21.5%. It was a disappointing quarter as it posted a significant miss of analysts’ net interest income estimates and a significant miss of analysts’ EPS estimates.

As expected, the stock is down 8.9% since the results and currently trades at $92.40.

Read our full analysis of Coastal Financial’s results here.

WesBanco (NASDAQ: WSBC)

Tracing its roots back to 1870 in West Virginia, WesBanco (NASDAQ: WSBC) is a bank holding company that provides retail and commercial banking, trust services, insurance, and investment products through its subsidiaries across several Midwestern and Mid-Atlantic states.

WesBanco reported revenues of $260.7 million, up 76.2% year on year. This print beat analysts’ expectations by 1.6%. Taking a step back, it was a satisfactory quarter as it also produced a narrow beat of analysts’ net interest income estimates but a slight miss of analysts’ tangible book value per share estimates.

The stock is down 7.4% since reporting and currently trades at $29.51.

Read our full, actionable report on WesBanco here, it’s free.

Synovus Financial (NYSE: SNV)

Tracing its roots back to 1888 when a worker accidentally dropped a textile mill payroll into the dust, prompting the need for better banking, Synovus Financial (NYSE: SNV) is a regional financial services company that provides commercial and consumer banking, wealth management, and specialized lending services across five southeastern states.

Synovus Financial reported revenues of $593.7 million, up 93.9% year on year. This number surpassed analysts’ expectations by 1.5%. It was a strong quarter as it also recorded an impressive beat of analysts’ EPS estimates and a solid beat of analysts’ tangible book value per share estimates.

The stock is down 12% since reporting and currently trades at $46.55.

Read our full, actionable report on Synovus Financial here, it’s free.

Market Update

In response to the Fed’s rate hikes in 2022 and 2023, inflation has been gradually trending down from its post-pandemic peak, trending closer to the Fed’s 2% target. Despite higher borrowing costs, the economy has avoided flashing recessionary signals. This is the much-desired soft landing that many investors hoped for. The recent rate cuts (0.5% in September and 0.25% in November 2024) have bolstered the stock market, making 2024 a strong year for equities. Donald Trump’s presidential win in November sparked additional market gains, sending indices to record highs in the days following his victory. However, debates continue over possible tariffs and corporate tax adjustments, raising questions about economic stability in 2025.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Growth Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.