StoneX currently trades at $96.80 and has been a dream stock for shareholders. It’s returned 274% since August 2020, more than tripling the S&P 500’s 89% gain. The company has also beaten the index over the past six months as its stock price is up 14.4%.

Is there a buying opportunity in StoneX, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is StoneX Not Exciting?

Despite the momentum, we're swiping left on StoneX for now. Here are two reasons why you should be careful with SNEX and a stock we'd rather own.

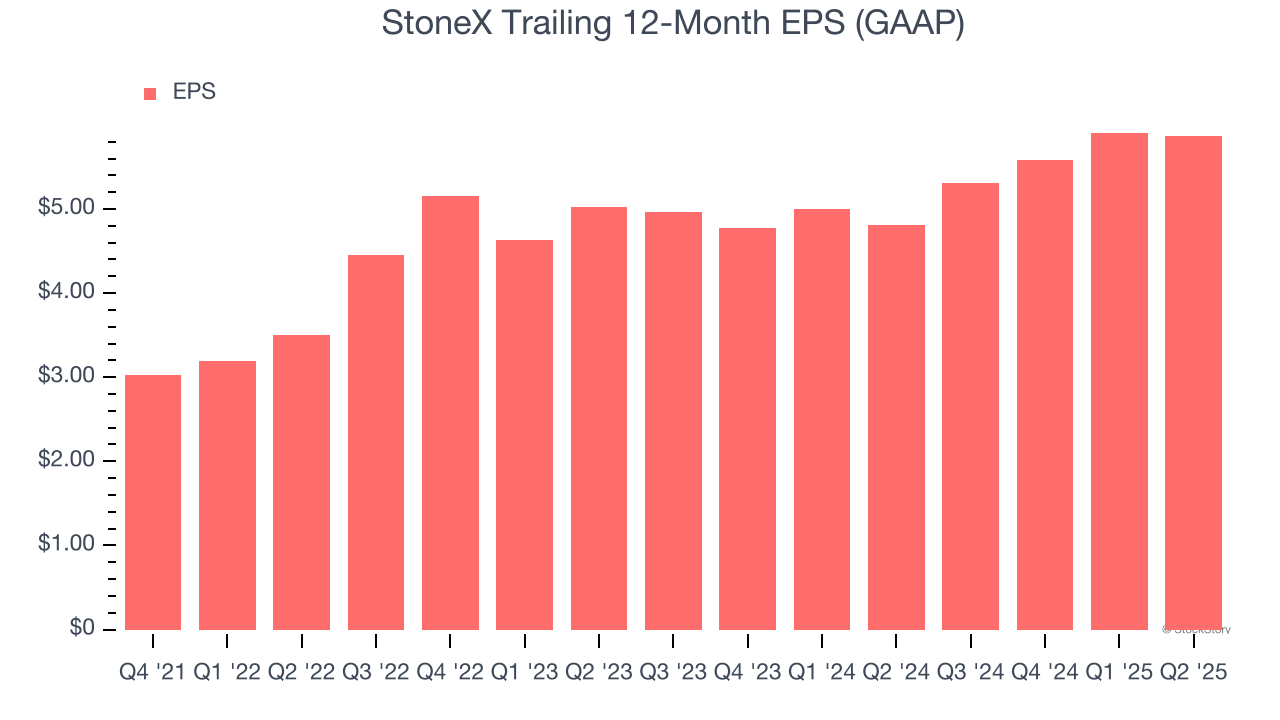

1. EPS Barely Growing

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

StoneX’s full-year EPS grew at a weak 3.2% compounded annual growth rate over the last four years, worse than the broader financials sector.

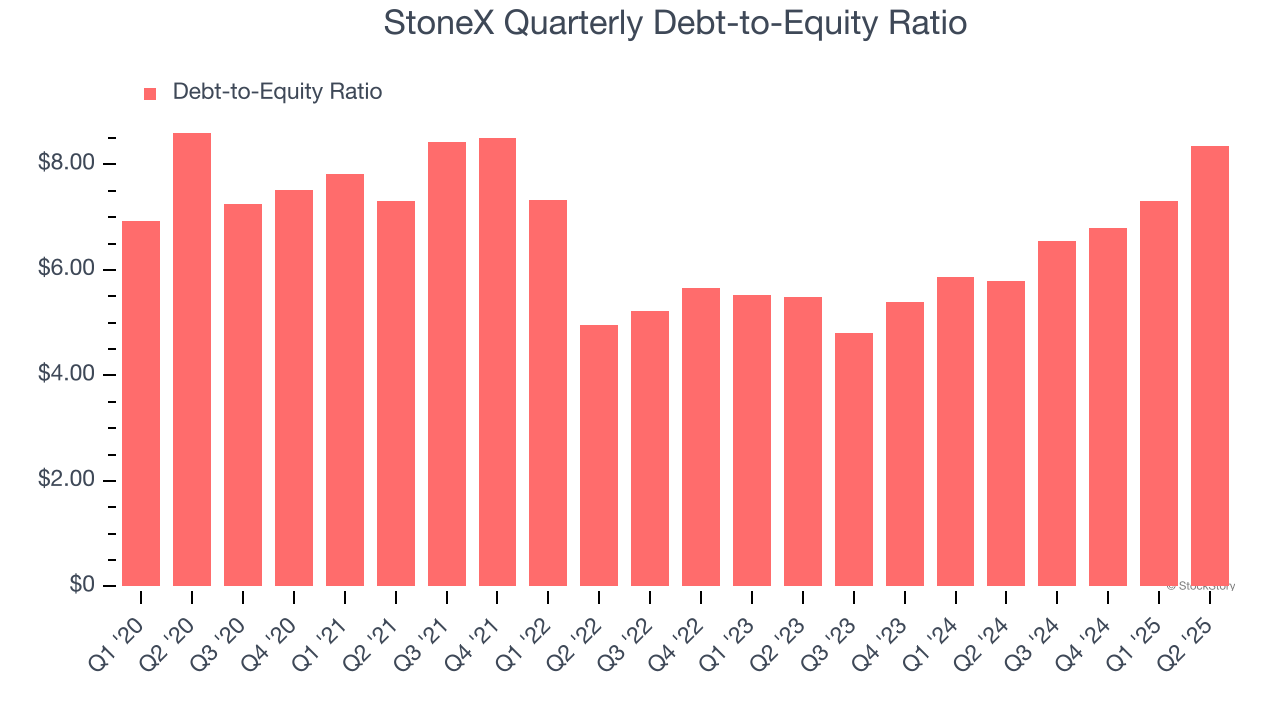

The debt-to-equity ratio is a widely used measure to assess a company's balance sheet health. A higher ratio means that a business aggressively financed its growth with debt. This can result in higher earnings (if the borrowed funds are invested profitably) but also increases risk.

2. Debt to Equity

If debt levels are too high, there could be difficulties in meeting obligations, especially during economic downturns or periods of rising interest rates if the debt has variable-rate payments.

StoneX currently has $16.51 billion of debt and $1.98 billion of shareholder's equity on its balance sheet, and over the past four quarters, has averaged a debt-to-equity ratio of 7.2×. We think this is dangerous - for an insurance business, anything above 1.0× raises red flags.

Final Judgment

StoneX’s business quality ultimately falls short of our standards. With its shares topping the market in recent months, the stock trades at 2.3× forward P/E (or $96.80 per share). While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're pretty confident there are more exciting stocks to buy at the moment. We’d recommend looking at the most entrenched endpoint security platform on the market.

Stocks We Would Buy Instead of StoneX

Donald Trump’s April 2025 "Liberation Day" tariffs sent markets into a tailspin, but stocks have since rebounded strongly, proving that knee-jerk reactions often create the best buying opportunities.

The smart money is already positioning for the next leg up. Don’t miss out on the recovery - check out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.