As the Q1 earnings season wraps, let’s dig into this quarter’s best and worst performers in the apparel and accessories industry, including Under Armour (NYSE: UAA) and its peers.

Thanks to social media and the internet, not only are styles changing more frequently today than in decades past but also consumers are shifting the way they buy their goods, favoring omnichannel and e-commerce experiences. Some apparel and accessories companies have made concerted efforts to adapt while those who are slower to move may fall behind.

The 17 apparel and accessories stocks we track reported a strong Q1. As a group, revenues beat analysts’ consensus estimates by 1.3% while next quarter’s revenue guidance was in line.

In light of this news, share prices of the companies have held steady. On average, they are relatively unchanged since the latest earnings results.

Under Armour (NYSE: UAA)

Founded in 1996 by a former University of Maryland football player, Under Armour (NYSE: UAA) is an apparel brand specializing in sportswear designed to improve athletic performance.

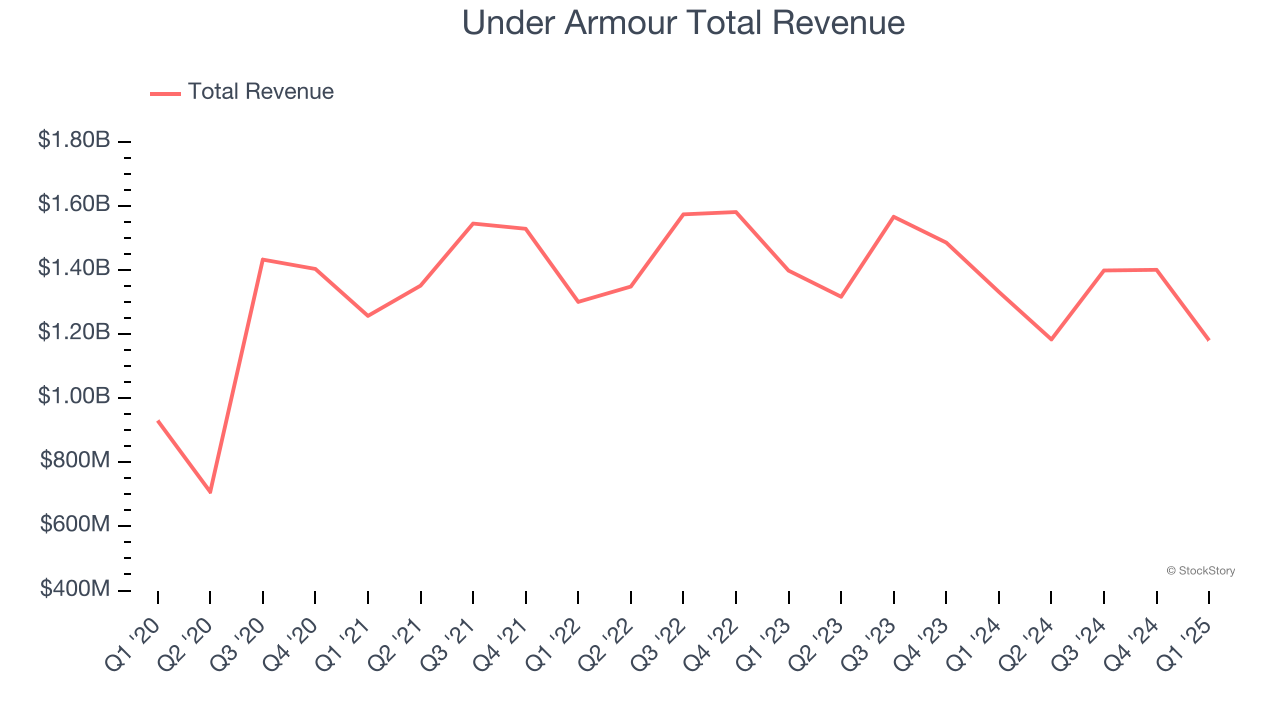

Under Armour reported revenues of $1.18 billion, down 11.4% year on year. This print exceeded analysts’ expectations by 1.3%. Overall, it was a strong quarter for the company with EPS guidance for next quarter exceeding analysts’ expectations and an impressive beat of analysts’ EBITDA estimates.

"One year into our strategic reset, we're laying the groundwork for a more focused Under Armour. By elevating products and storytelling, tightening distribution, and refining our operating model, we are in the process of reigniting brand relevance and positioning the business for sustainable, profitable growth," said Under Armour President and CEO Kevin Plank.

Under Armour delivered the slowest revenue growth of the whole group. The market was likely pricing in the results, and the stock is flat since reporting. It currently trades at $6.19.

Is now the time to buy Under Armour? Access our full analysis of the earnings results here, it’s free.

Best Q1: ThredUp (NASDAQ: TDUP)

Founded to revolutionize thrifting, ThredUp (NASDAQ: TDUP) is a leading online fashion resale marketplace offering a wide selection of gently-used clothing and accessories.

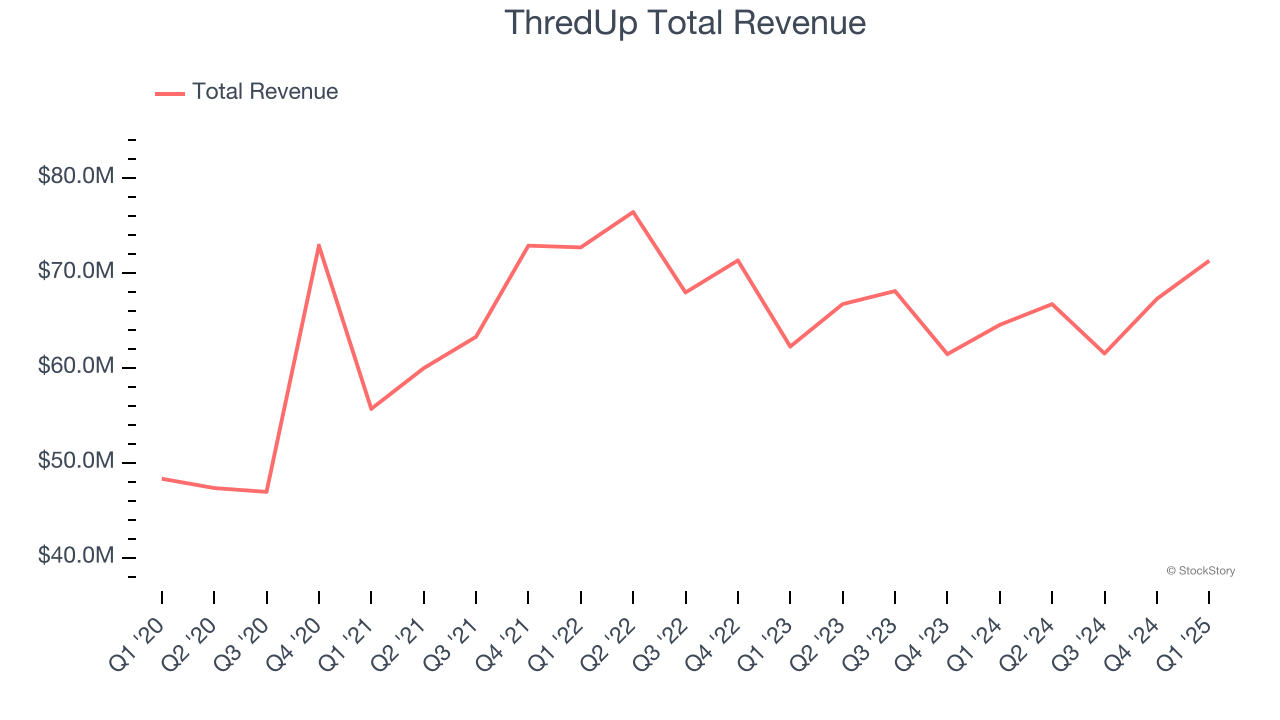

ThredUp reported revenues of $71.29 million, up 10.5% year on year, outperforming analysts’ expectations by 4.4%. The business had an exceptional quarter with an impressive beat of analysts’ EBITDA estimates.

ThredUp delivered the fastest revenue growth among its peers. The market seems happy with the results as the stock is up 91% since reporting. It currently trades at $8.46.

Is now the time to buy ThredUp? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: Movado (NYSE: MOV)

With its watches displayed in 20 museums around the world, Movado (NYSE: MOV) is a watchmaking company with a portfolio of watch brands and accessories.

Movado reported revenues of $131.8 million, down 1.9% year on year, falling short of analysts’ expectations by 7.3%. It was a disappointing quarter as it posted a significant miss of analysts’ EPS estimates.

Movado delivered the weakest performance against analyst estimates in the group. As expected, the stock is down 11.9% since the results and currently trades at $15.38.

Read our full analysis of Movado’s results here.

Oxford Industries (NYSE: OXM)

The parent company of Tommy Bahama, Oxford Industries (NYSE: OXM) is a lifestyle fashion conglomerate with brands that embody outdoor happiness.

Oxford Industries reported revenues of $392.9 million, down 1.3% year on year. This result topped analysts’ expectations by 2.1%. Zooming out, it was a slower quarter as it logged full-year EPS guidance missing analysts’ expectations.

The stock is down 18.6% since reporting and currently trades at $40.73.

Read our full, actionable report on Oxford Industries here, it’s free.

Carter's (NYSE: CRI)

Rumored to sell more than 10 products for every child born in the United States, Carter's (NYSE: CRI) is an American designer and marketer of children's apparel.

Carter's reported revenues of $629.8 million, down 4.8% year on year. This print beat analysts’ expectations by 0.9%. Overall, it was a strong quarter as it also put up an impressive beat of analysts’ EPS estimates and a narrow beat of analysts’ same-store sales estimates.

The stock is down 21.9% since reporting and currently trades at $29.83.

Read our full, actionable report on Carter's here, it’s free.

Market Update

Thanks to the Fed’s rate hikes in 2022 and 2023, inflation has been on a steady path downward, easing back toward that 2% sweet spot. Fortunately (miraculously to some), all this tightening didn’t send the economy tumbling into a recession, so here we are, cautiously celebrating a soft landing. The cherry on top? Recent rate cuts (half a point in September 2024, a quarter in November) have propped up markets, especially after Trump’s November win lit a fire under major indices and sent them to all-time highs. However, there’s still plenty to ponder — tariffs, corporate tax cuts, and what 2025 might hold for the economy.

Want to invest in winners with rock-solid fundamentals? Check out our Hidden Gem Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.