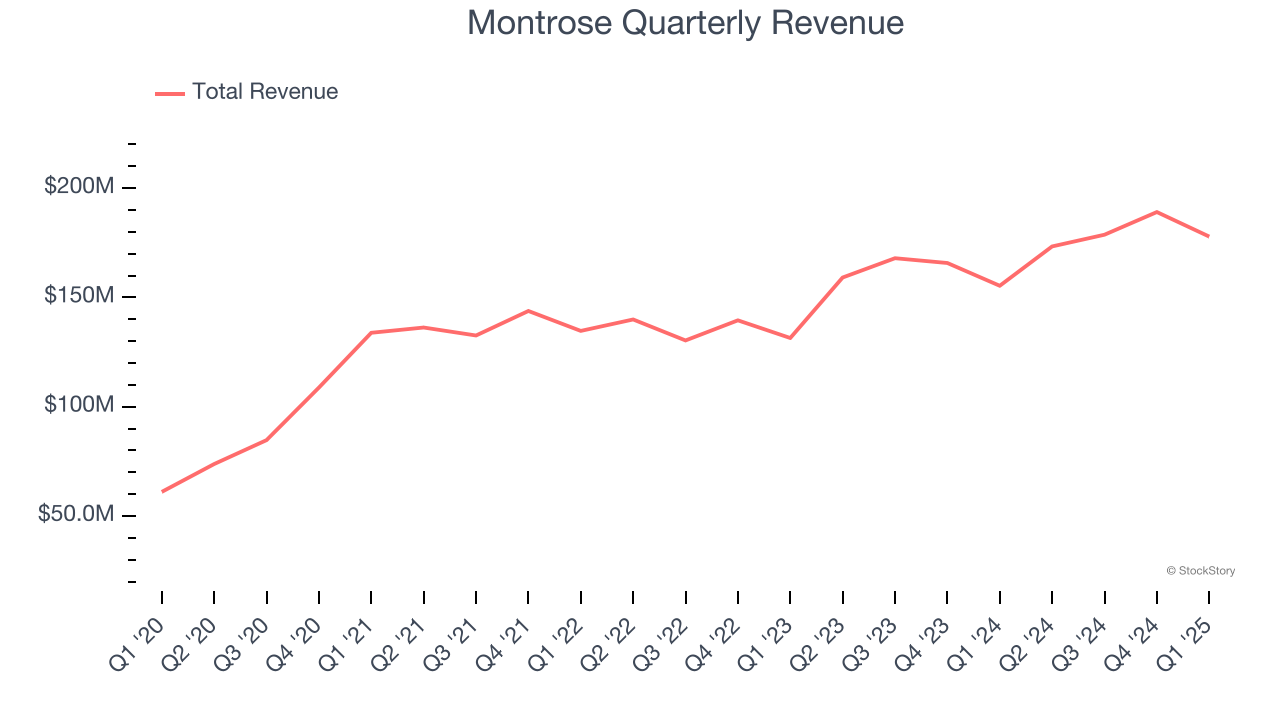

Environmental services provider Montrose (NYSE: MEG) reported Q1 CY2025 results beating Wall Street’s revenue expectations, with sales up 14.5% year on year to $177.8 million. The company’s full-year revenue guidance of $760 million at the midpoint came in 0.7% above analysts’ estimates. Its non-GAAP profit of $0.07 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Montrose? Find out by accessing our full research report, it’s free.

Montrose (MEG) Q1 CY2025 Highlights:

- Revenue: $177.8 million vs analyst estimates of $167.8 million (14.5% year-on-year growth, 6% beat)

- Adjusted EPS: $0.07 vs analyst estimates of -$0.09 (significant beat)

- Adjusted EBITDA: $19.03 million vs analyst estimates of $15.65 million (10.7% margin, 21.6% beat)

- The company reconfirmed its revenue guidance for the full year of $760 million at the midpoint

- EBITDA guidance for the full year is $106.5 million at the midpoint, above analyst estimates of $104.5 million

- Operating Margin: -5.9%, in line with the same quarter last year

- Free Cash Flow was $2.35 million, up from -$28 million in the same quarter last year

- Market Capitalization: $529 million

Montrose Chief Executive Officer and Director, Vijay Manthripragada, commented, "Our uniquely integrated portfolio of environmental science-based solutions and technology continues to position Montrose to exceed expectations. We reported our highest-ever first-quarter revenue, Consolidated Adjusted EBITDA, and operating cash flow. In November 2024, we announced an acquisition pause to focus on stated objectives—to deliver high-single-digit organic revenue growth, enhance margins, improve cash flow generation, prioritize redemption of the preferred shares, optimize our balance sheet, and maintain ample liquidity. Our first quarter performance demonstrates the initial benefits of this shift in our focus. Numerous tailwinds, which we expect to sustain, drove our strong results and underpin confidence in our strengthened 2025 guidance. Examples of key tailwinds include: our private sector clients' increasing industrial activity, the impact of US state regulations on our private and public sector clients, and the strategic advantages of our integrated business model and service portfolio."

Company Overview

Founded to protect a tree-lined two-lane road, Montrose (NYSE: MEG) provides air quality monitoring, environmental laboratory testing, compliance, and environmental consulting services.

Sales Growth

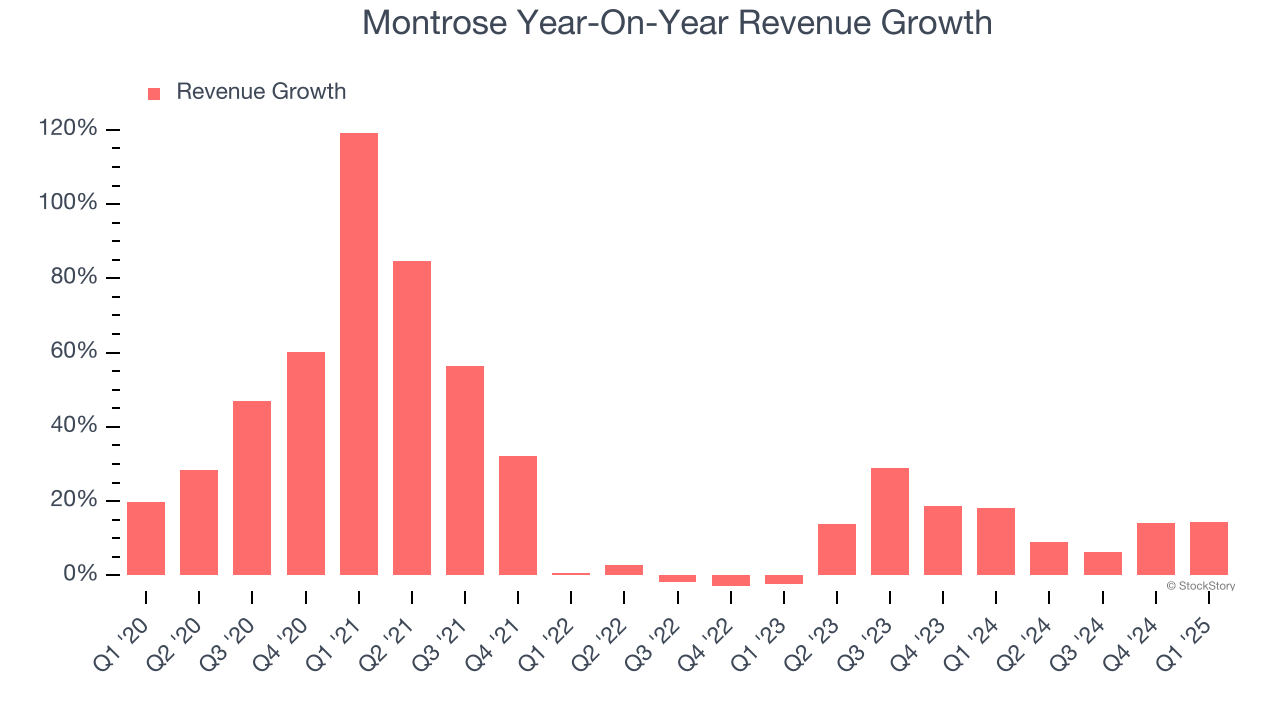

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Luckily, Montrose’s sales grew at an incredible 24.1% compounded annual growth rate over the last five years. Its growth beat the average industrials company and shows its offerings resonate with customers, a helpful starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Montrose’s annualized revenue growth of 15.3% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Montrose reported year-on-year revenue growth of 14.5%, and its $177.8 million of revenue exceeded Wall Street’s estimates by 6%.

Looking ahead, sell-side analysts expect revenue to grow 6.9% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and indicates its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Operating Margin

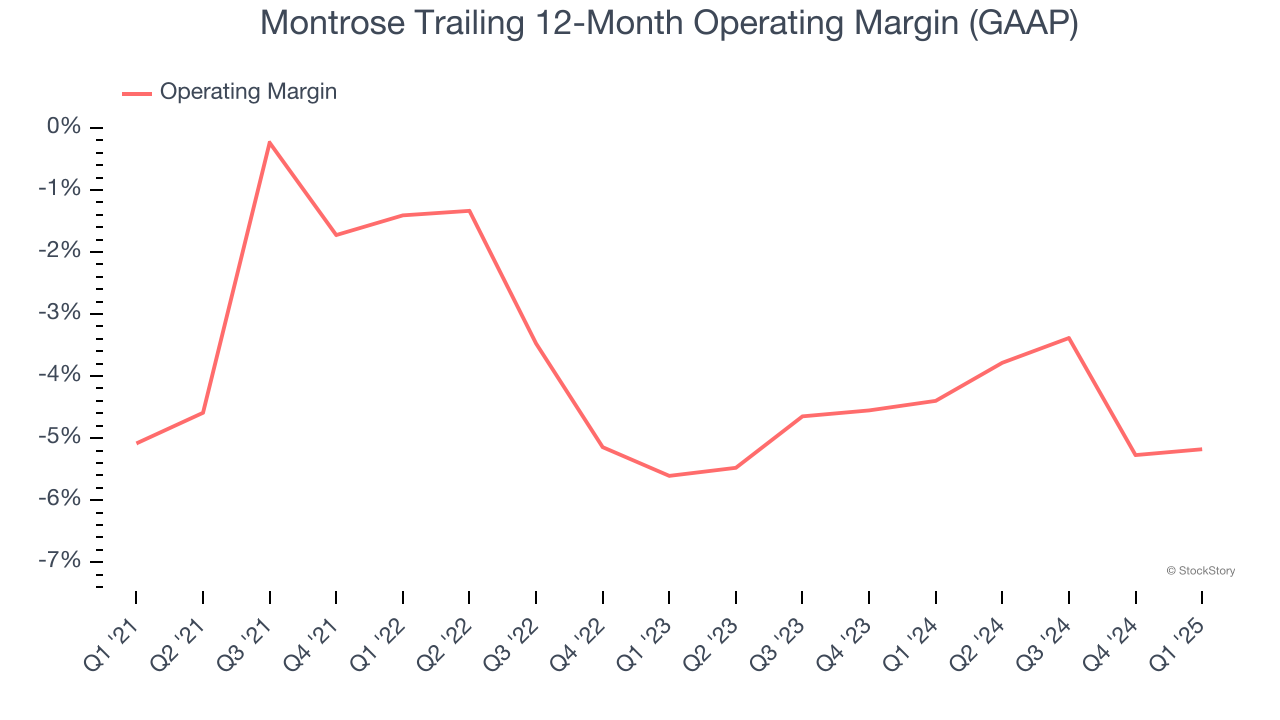

Montrose’s high expenses have contributed to an average operating margin of negative 4.3% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out.

Analyzing the trend in its profitability, Montrose’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q1, Montrose generated a negative 5.9% operating margin.

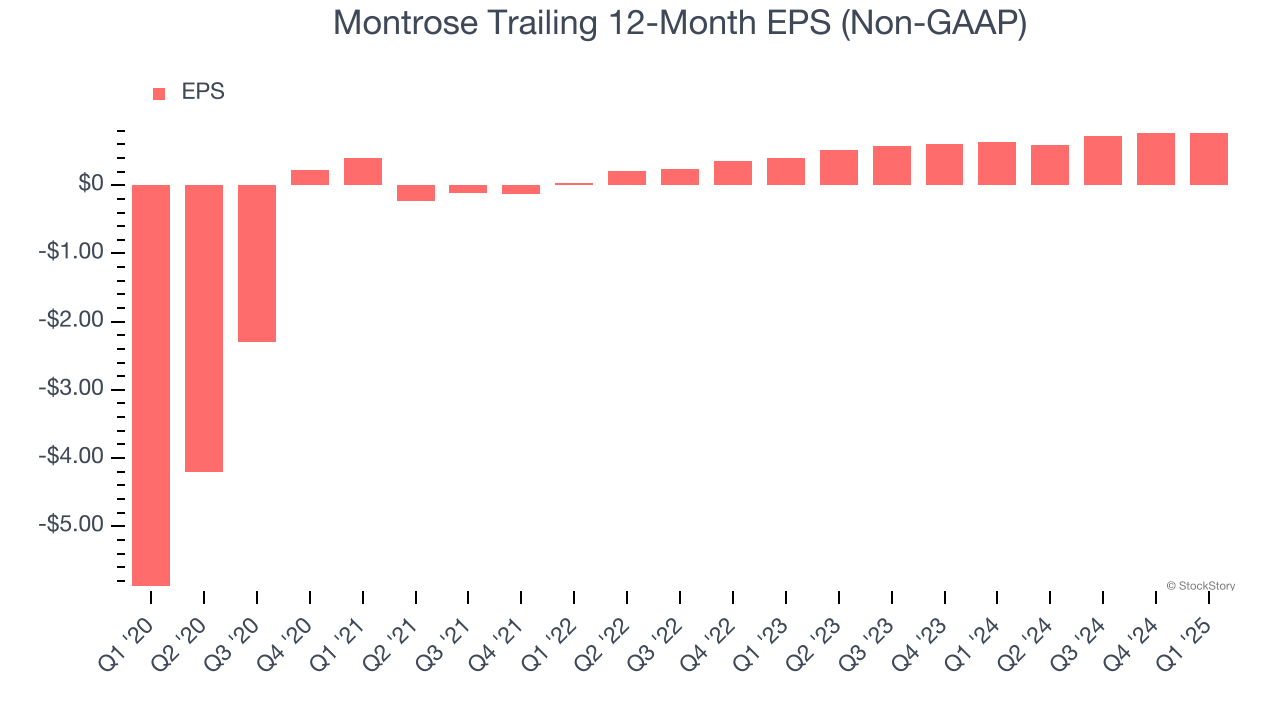

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Montrose’s full-year EPS flipped from negative to positive over the last five years. This is a good sign and shows it’s at an inflection point.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

Montrose’s EPS grew at an astounding 38.7% compounded annual growth rate over the last two years, higher than its 15.3% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

We can take a deeper look into Montrose’s earnings quality to better understand the drivers of its performance. While we mentioned earlier that Montrose’s operating margin was flat this quarter, a two-year view shows its margin has expanded by 1.6 percentage points. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q1, Montrose reported EPS at $0.07, in line with the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

Key Takeaways from Montrose’s Q1 Results

We were impressed by how significantly Montrose blew past analysts’ revenue, EPS, and EBITDA expectations this quarter. We were also excited its full-year EBITDA guidance outperformed Wall Street’s estimates. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 7.5% to $16.11 immediately after reporting.

Montrose put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.