Telecommunications and cable service provider Liberty Broadband (NASDAQ: LBRDK) reported revenue ahead of Wall Street’s expectations in Q1 CY2025, with sales up 8.6% year on year to $266 million. Its GAAP profit of $1.87 per share increased from $1.69 in the same quarter last year.

Is now the time to buy Liberty Broadband? Find out by accessing our full research report, it’s free.

Liberty Broadband (LBRDK) Q1 CY2025 Highlights:

- Revenue: $266 million vs analyst estimates of $248.1 million (8.6% year-on-year growth, 7.2% beat)

- Adjusted EBITDA: $96 million vs analyst estimates of $80.9 million (36.1% margin, 18.7% beat)

- Operating Margin: 16.2%, up from 11.4% in the same quarter last year

- Free Cash Flow Margin: 4.9%, up from 2.4% in the same quarter last year

- Market Capitalization: $13.36 billion

Company Overview

Operating across the United States, Liberty Broadband (NASDAQ: LBRDK) is a provider of high-speed internet, cable television, and telecommunications services across various markets.

Sales Growth

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $1.04 billion in revenue over the past 12 months, Liberty Broadband is a small player in the business services space, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and numerous distribution channels. On the bright side, it can grow faster because it has more room to expand.

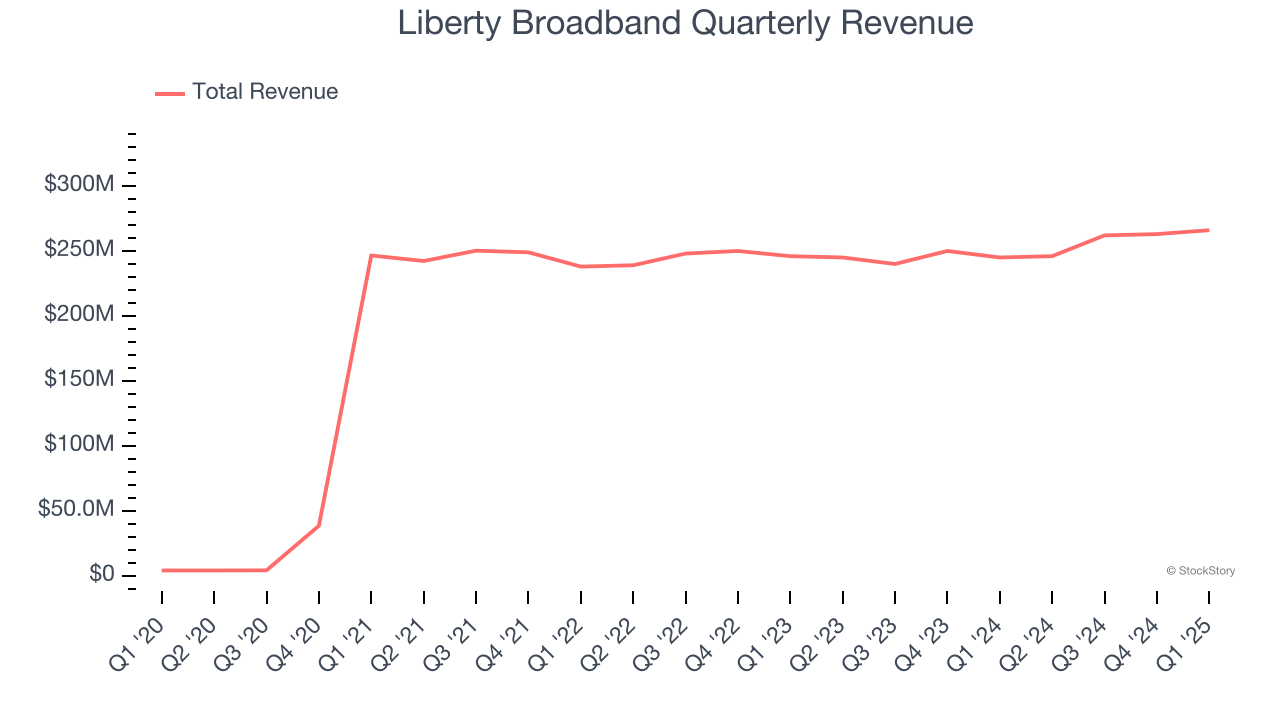

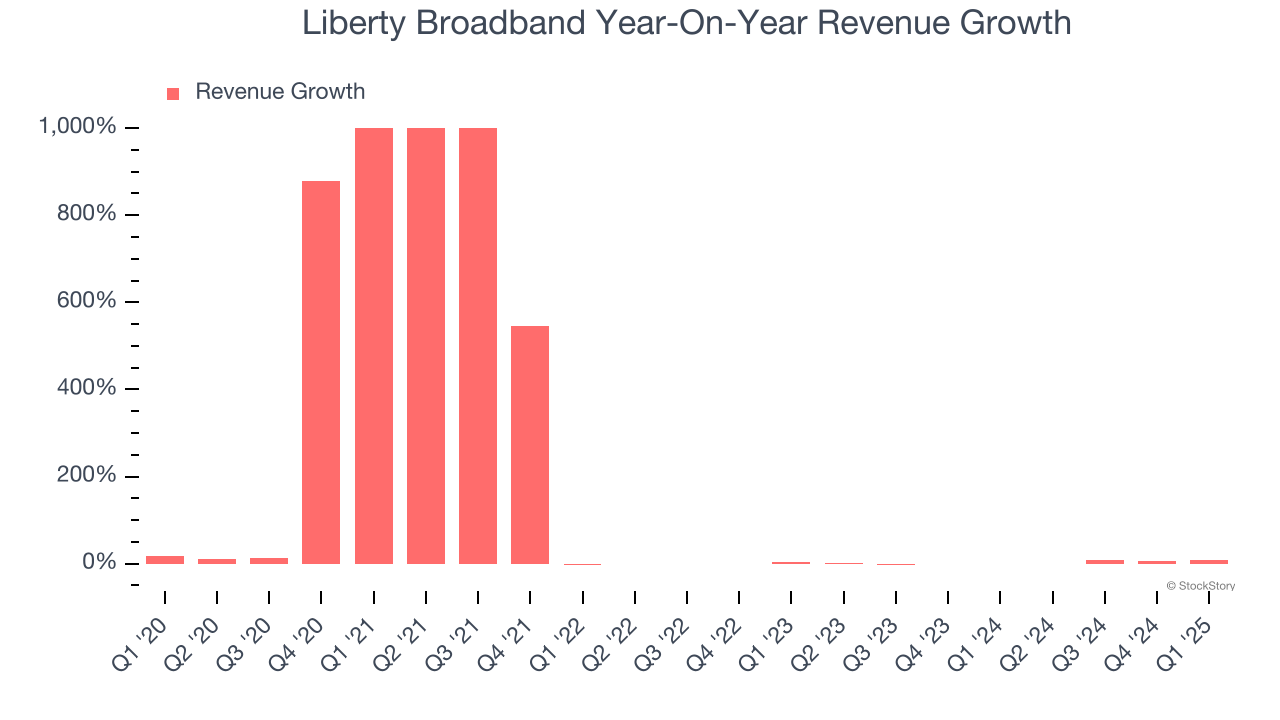

As you can see below, Liberty Broadband’s 132% annualized revenue growth over the last five years was incredible. This shows it had high demand, a useful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Liberty Broadband’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 2.7% over the last two years was well below its five-year trend.

This quarter, Liberty Broadband reported year-on-year revenue growth of 8.6%, and its $266 million of revenue exceeded Wall Street’s estimates by 7.2%.

Looking ahead, sell-side analysts expect revenue to decline by 1.1% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and implies its products and services will see some demand headwinds.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D.

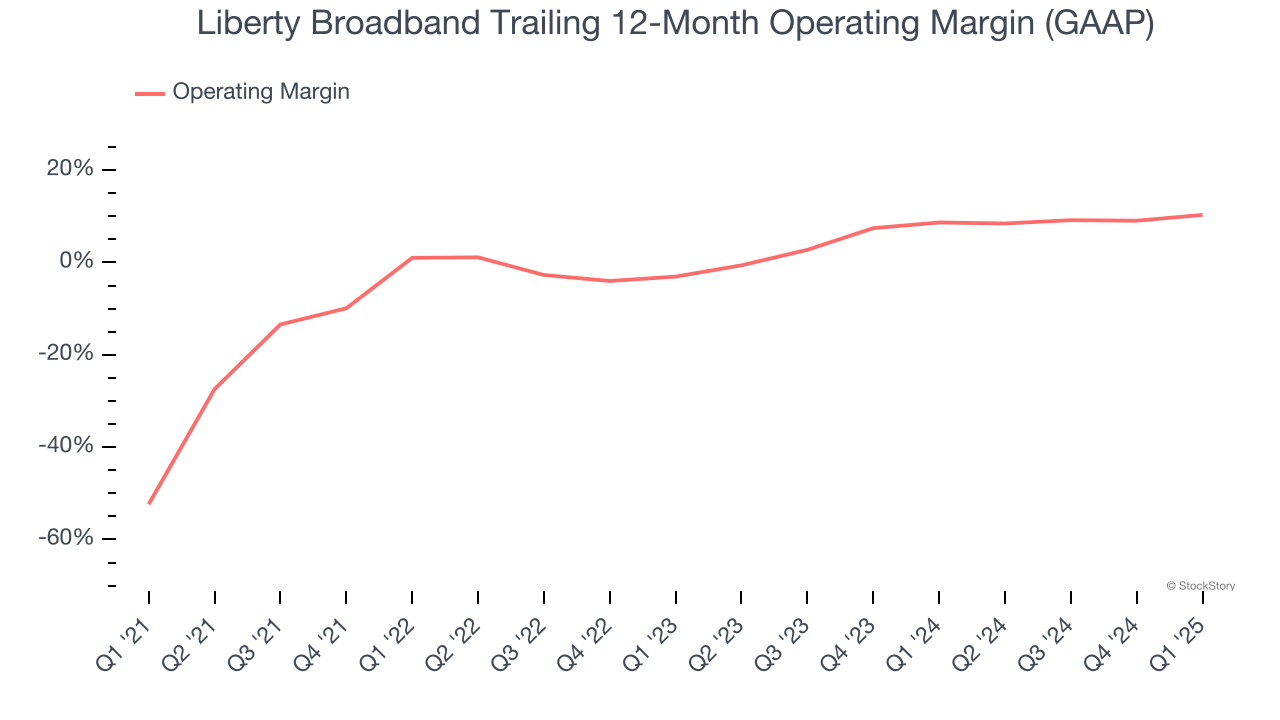

Liberty Broadband was roughly breakeven when averaging the last five years of quarterly operating profits, inadequate for a business services business.

On the plus side, Liberty Broadband’s operating margin rose by 62.7 percentage points over the last five years, as its sales growth gave it immense operating leverage.

This quarter, Liberty Broadband generated an operating profit margin of 16.2%, up 4.7 percentage points year on year. This increase was a welcome development and shows it was more efficient.

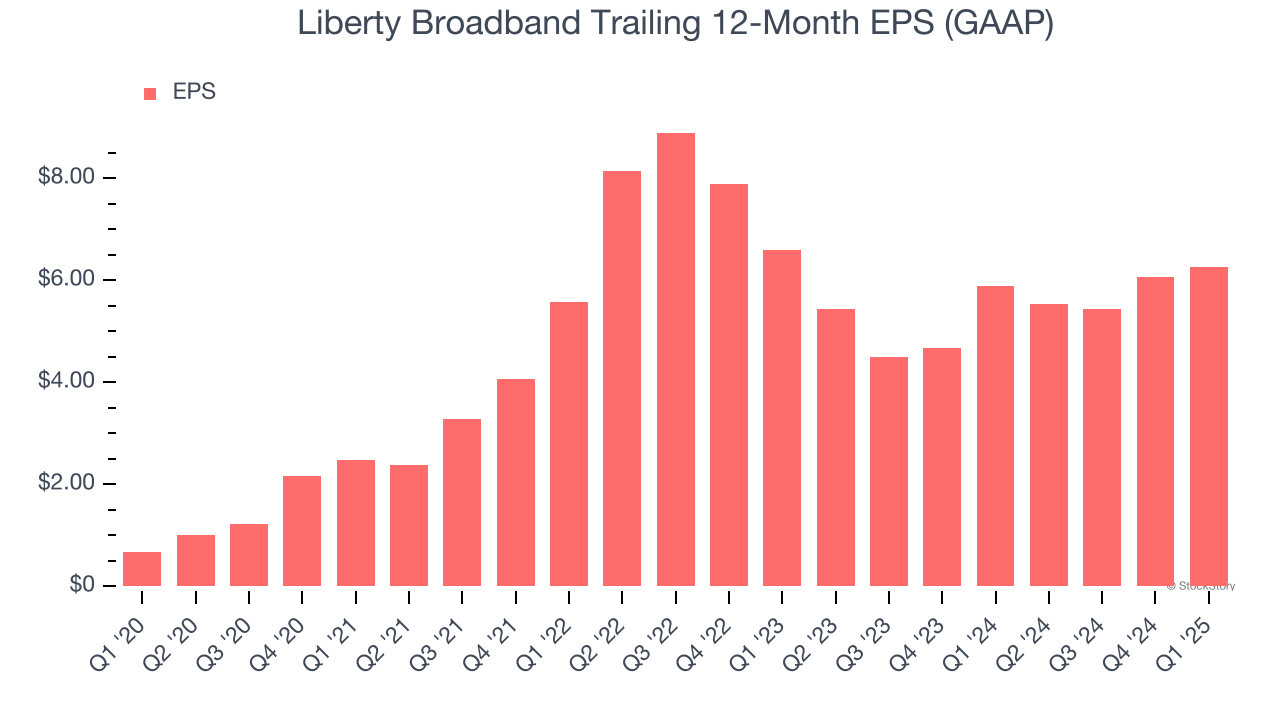

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Liberty Broadband’s EPS grew at an astounding 56% compounded annual growth rate over the last five years. Despite its operating margin expansion and share repurchases during that time, this performance was lower than its 132% annualized revenue growth, telling us the delta came from reduced interest expenses or taxes.

In Q1, Liberty Broadband reported EPS at $1.87, up from $1.69 in the same quarter last year. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

Key Takeaways from Liberty Broadband’s Q1 Results

We were impressed by how significantly Liberty Broadband blew past analysts’ revenue and EBITDA expectations this quarter. Zooming out, we think this was a good print with some key areas of upside. The stock remained flat at $93.43 immediately following the results.

So do we think Liberty Broadband is an attractive buy at the current price? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.