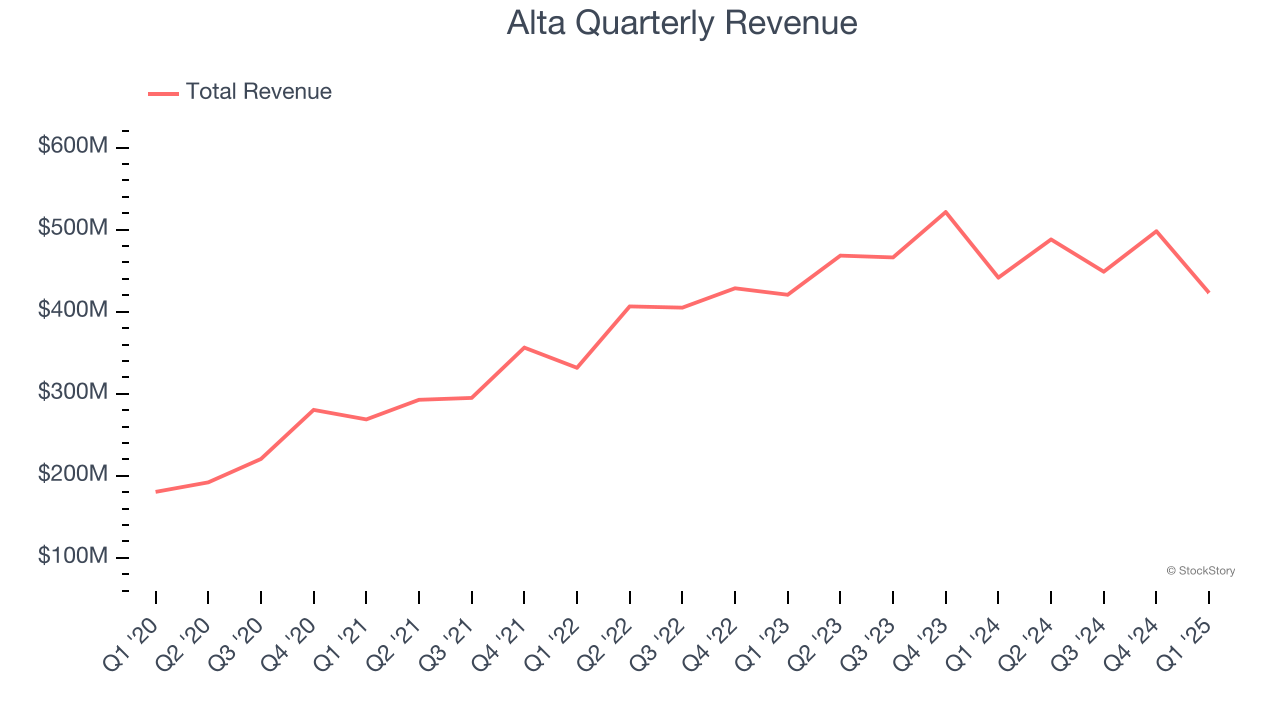

Equipment distribution company Alta Equipment Group (NYSE: ALTG) fell short of the market’s revenue expectations in Q1 CY2025, with sales falling 4.2% year on year to $423 million. Its non-GAAP loss of $0.48 per share was in line with analysts’ consensus estimates.

Is now the time to buy Alta? Find out by accessing our full research report, it’s free.

Alta (ALTG) Q1 CY2025 Highlights:

- Revenue: $423 million vs analyst estimates of $432.9 million (4.2% year-on-year decline, 2.3% miss)

- Adjusted EPS: -$0.48 vs analyst estimates of -$0.48 (in line)

- Adjusted EBITDA: $33.6 million vs analyst estimates of $31.13 million (7.9% margin, 8% beat)

- EBITDA guidance for the full year is $179 million at the midpoint, above analyst estimates of $176.2 million

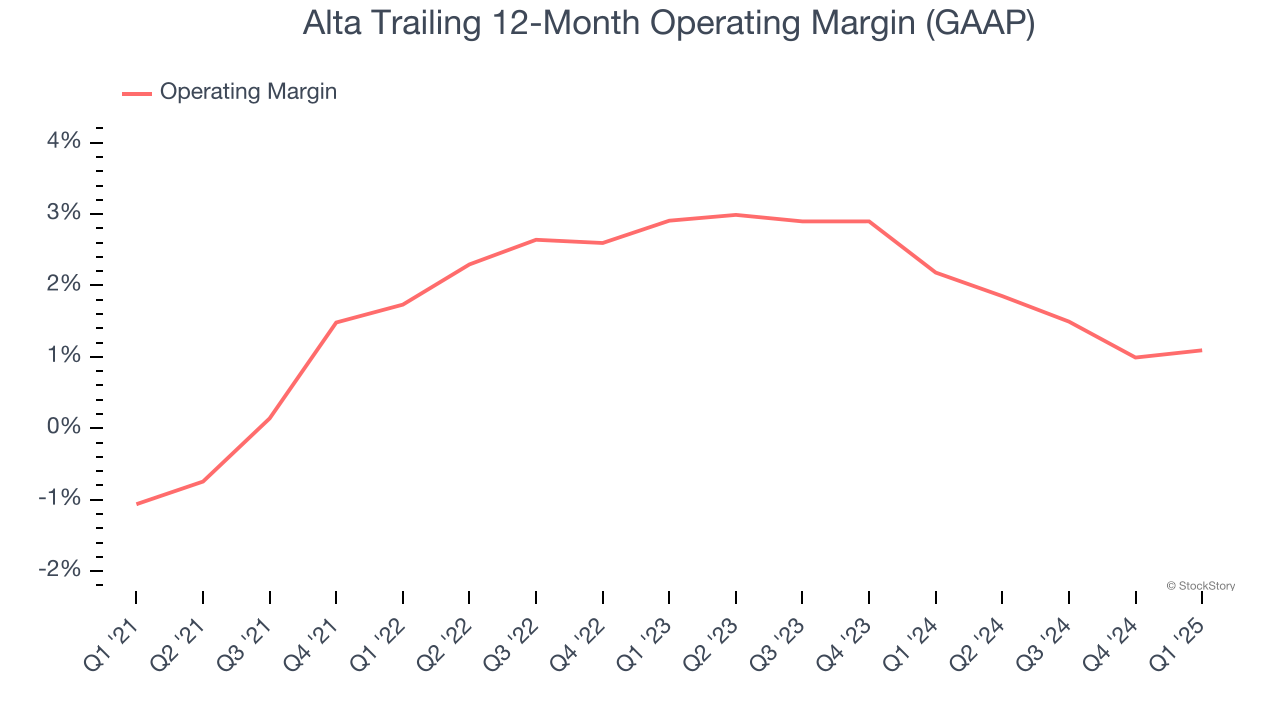

- Operating Margin: 0.2%, in line with the same quarter last year

- Free Cash Flow was -$31.2 million compared to -$29.2 million in the same quarter last year

- Market Capitalization: $158.3 million

Company Overview

Founded in 1984, Alta Equipment Group (NYSE: ALTG) is a provider of industrial and construction equipment and services across the Midwest and Northeast United States.

Sales Growth

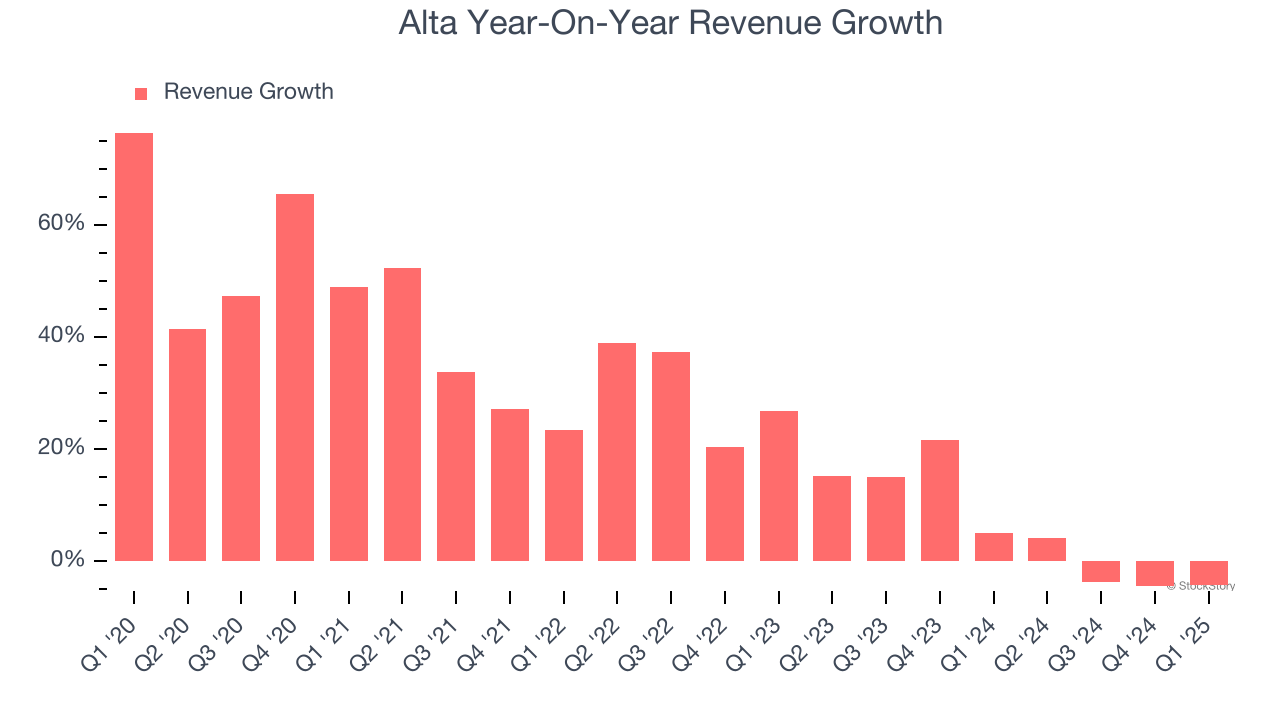

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Luckily, Alta’s sales grew at an incredible 23.9% compounded annual growth rate over the last five years. Its growth beat the average industrials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Alta’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 5.8% over the last two years was well below its five-year trend.

We can dig further into the company’s revenue dynamics by analyzing its most important segments, Equipment and Parts, which are 52.4% and 17% of revenue. Over the last two years, Alta’s Equipment revenue (new and used) averaged 3.4% year-on-year declines while its Parts revenue (maintenance and repair products) averaged 1.5% declines.

This quarter, Alta missed Wall Street’s estimates and reported a rather uninspiring 4.2% year-on-year revenue decline, generating $423 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 3.8% over the next 12 months, a slight deceleration versus the last two years. This projection doesn't excite us and indicates its products and services will face some demand challenges.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Alta was profitable over the last five years but held back by its large cost base. Its average operating margin of 1.6% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

On the plus side, Alta’s operating margin rose by 2.2 percentage points over the last five years, as its sales growth gave it operating leverage.

This quarter, Alta’s breakeven margin was in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

Earnings Per Share

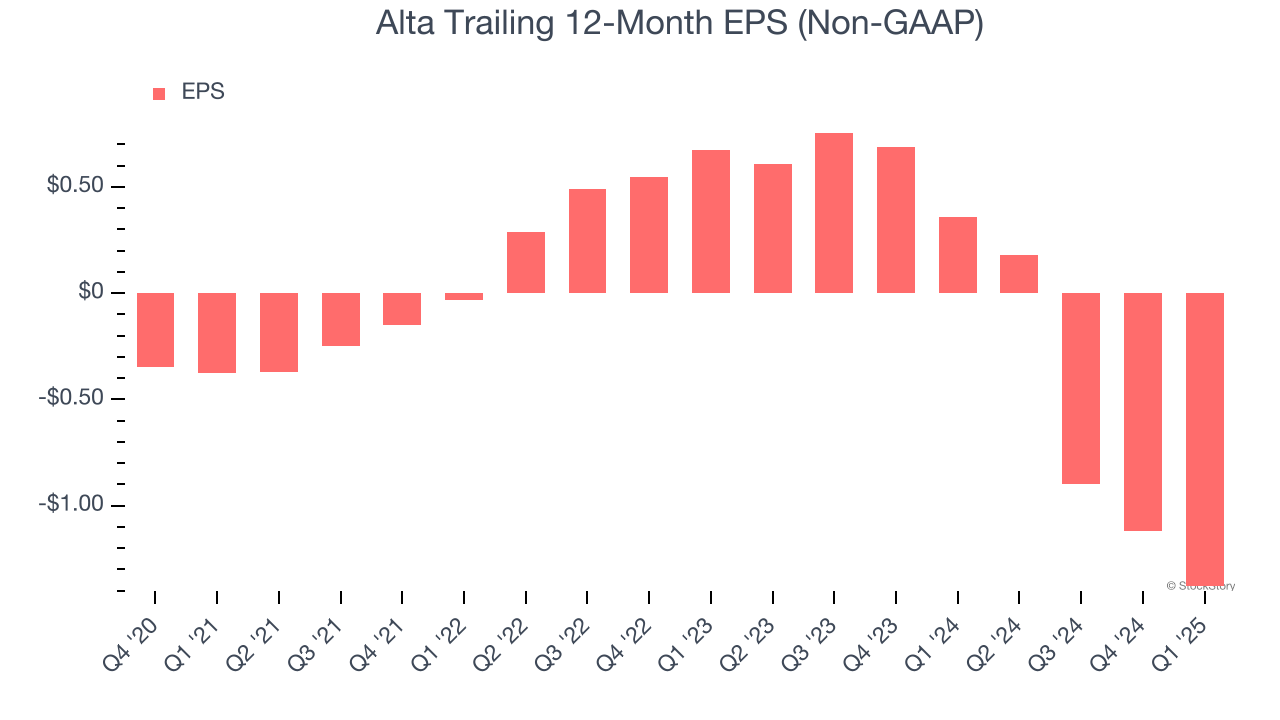

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Alta’s earnings losses deepened over the last four years as its EPS dropped 38.3% annually. We tend to steer our readers away from companies with falling EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Alta’s low margin of safety could leave its stock price susceptible to large downswings.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

Sadly for Alta, its EPS declined by 101% annually over the last two years while its revenue grew by 5.8%. This tells us the company became less profitable on a per-share basis as it expanded.

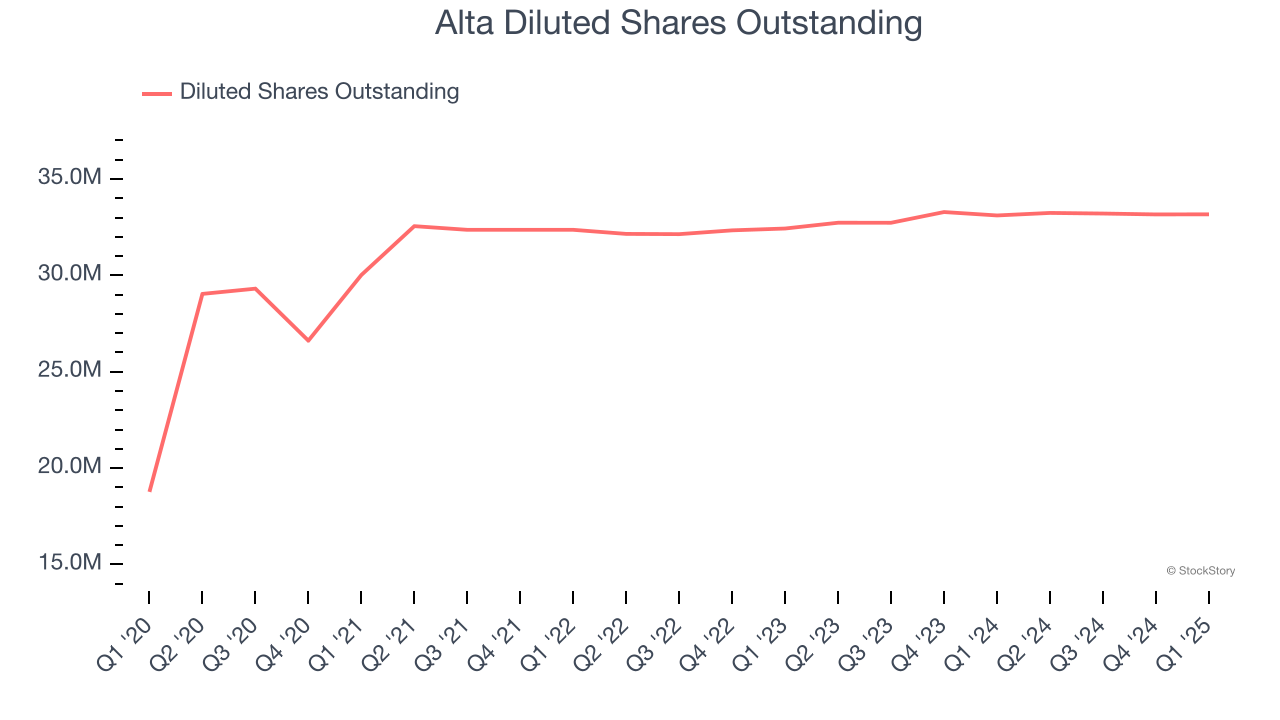

Diving into the nuances of Alta’s earnings can give us a better understanding of its performance. While we mentioned earlier that Alta’s operating margin was flat this quarter, a two-year view shows its margin has declined by 2.7 percentage pointswhile its share count has grown 2.3%. This means the company not only became less efficient with its operating expenses but also diluted its shareholders.

In Q1, Alta reported EPS at negative $0.48, down from negative $0.22 in the same quarter last year. This print was close to analysts’ estimates. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

Key Takeaways from Alta’s Q1 Results

We were impressed by how significantly Alta blew past analysts’ EBITDA expectations this quarter. We were also glad its full-year EBITDA guidance exceeded Wall Street’s estimates. On the other hand, its revenue missed significantly. Overall, this print had some key positives, but the market seemed to be hoping for better top-line performance. The stock traded down 5.1% to $4.30 immediately following the results.

Is Alta an attractive investment opportunity right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.