Revvity currently trades at $96.77 per share and has shown little upside over the past six months, posting a middling return of 2.5%. The stock also fell short of the S&P 500’s 13.6% gain during that period.

Is now the time to buy Revvity, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free for active Edge members.

Why Do We Think Revvity Will Underperform?

We're swiping left on Revvity for now. Here are three reasons you should be careful with RVTY and a stock we'd rather own.

1. Weak Constant Currency Growth Points to Soft Demand

We can better understand Research Tools & Consumables companies by analyzing their constant currency revenue. This metric excludes currency movements, which are outside of Revvity’s control and are not indicative of underlying demand.

Over the last two years, Revvity’s constant currency revenue averaged 2% year-on-year growth. This performance slightly lagged the sector and suggests it might have to lower prices or invest in product improvements to accelerate growth, factors that can hinder near-term profitability.

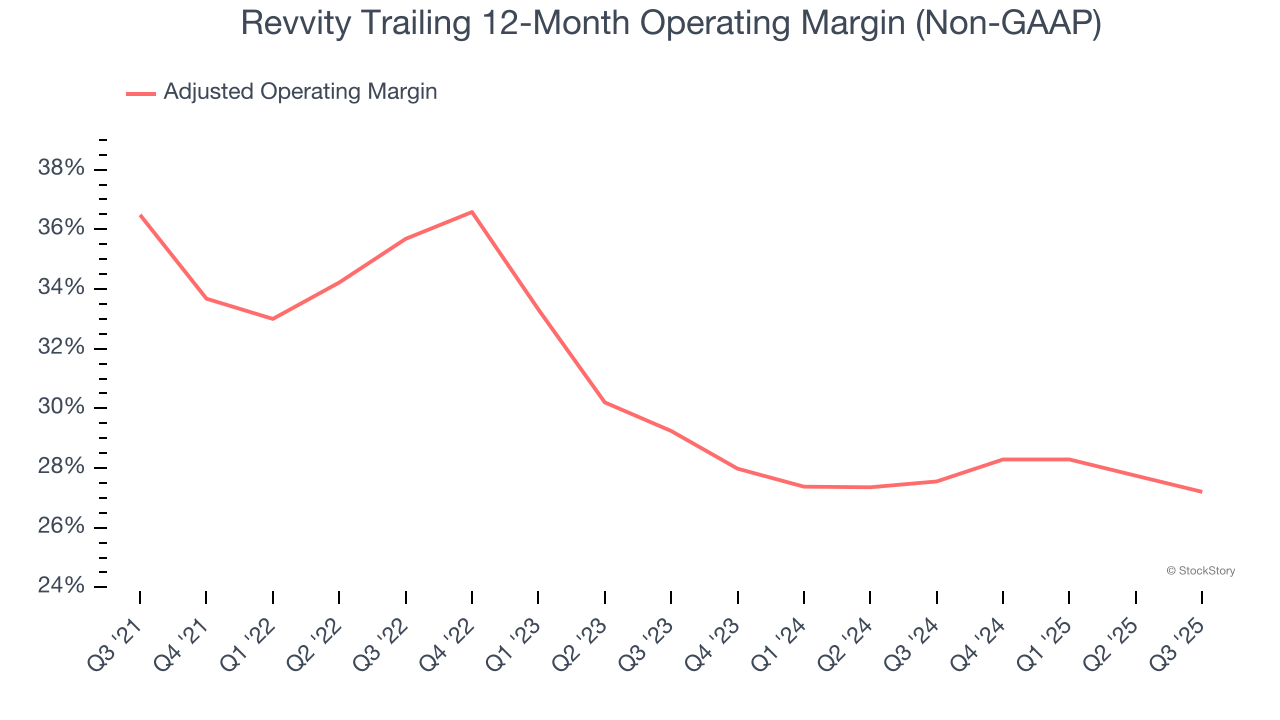

2. Shrinking Adjusted Operating Margin

Adjusted operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D. It also removes various one-time costs to paint a better picture of normalized profits.

Analyzing the trend in its profitability, Revvity’s adjusted operating margin decreased by 9.3 percentage points over the last five years. Even though its historical margin was healthy, shareholders will want to see Revvity become more profitable in the future. Its adjusted operating margin for the trailing 12 months was 27.2%.

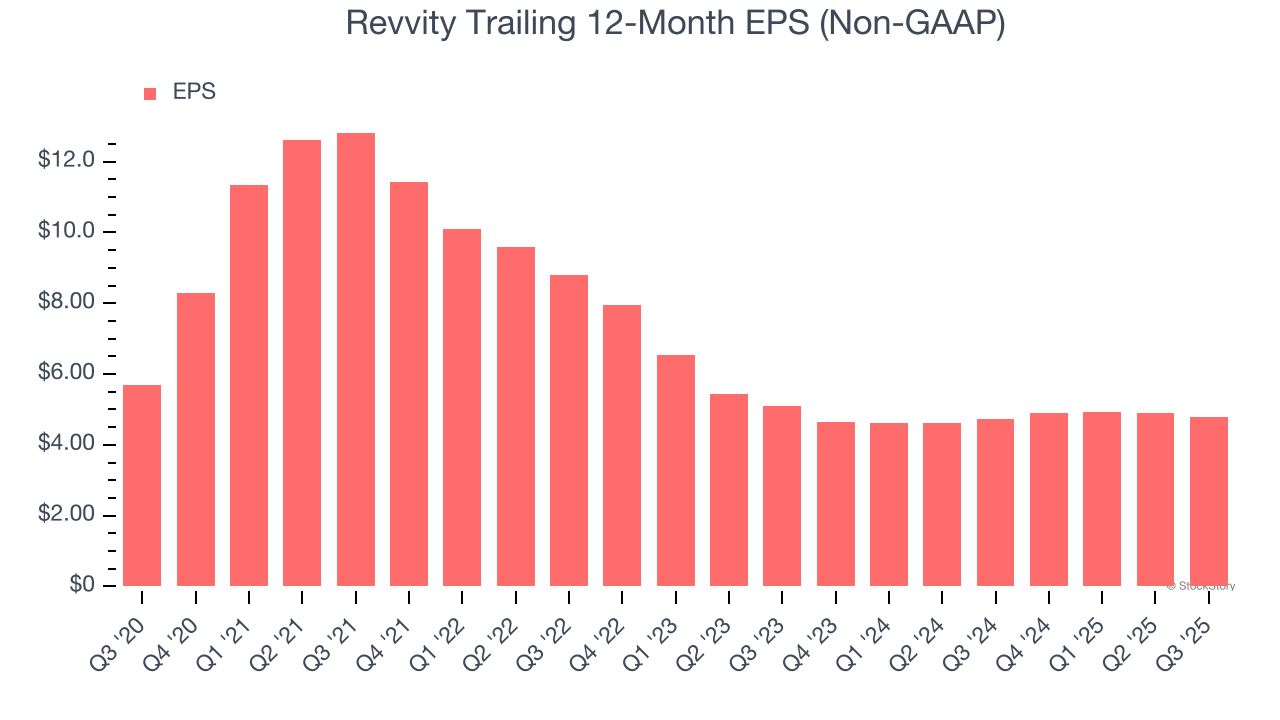

3. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for Revvity, its EPS and revenue declined by 3.4% and 2.7% annually over the last five years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Revvity’s low margin of safety could leave its stock price susceptible to large downswings.

Final Judgment

We see the value of companies making people healthier, but in the case of Revvity, we’re out. With its shares lagging the market recently, the stock trades at 18.3× forward P/E (or $96.77 per share). This multiple tells us a lot of good news is priced in - you can find more timely opportunities elsewhere. Let us point you toward one of Charlie Munger’s all-time favorite businesses.

High-Quality Stocks for All Market Conditions

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.