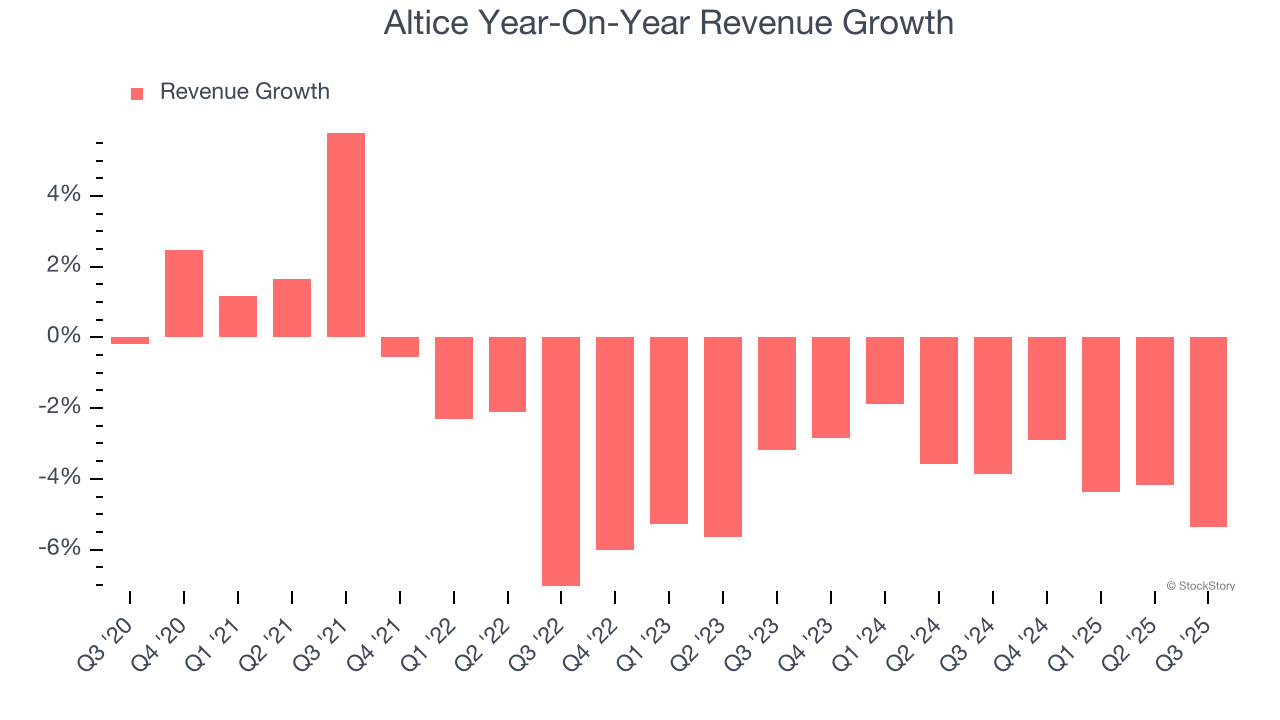

Telecommunications and cable services provider Altice USA (NYSE: ATUS) fell short of the markets revenue expectations in Q3 CY2025, with sales falling 5.4% year on year to $2.11 billion. Its GAAP loss of $3.47 per share was significantly below analysts’ consensus estimates.

Is now the time to buy Altice? Find out by accessing our full research report, it’s free for active Edge members.

Altice (ATUS) Q3 CY2025 Highlights:

- Revenue: $2.11 billion vs analyst estimates of $2.14 billion (5.4% year-on-year decline, 1.4% miss)

- EPS (GAAP): -$3.47 vs analyst estimates of -$0.05 (significant miss)

- Adjusted EBITDA: $830.7 million vs analyst estimates of $837.2 million (39.4% margin, 0.8% miss)

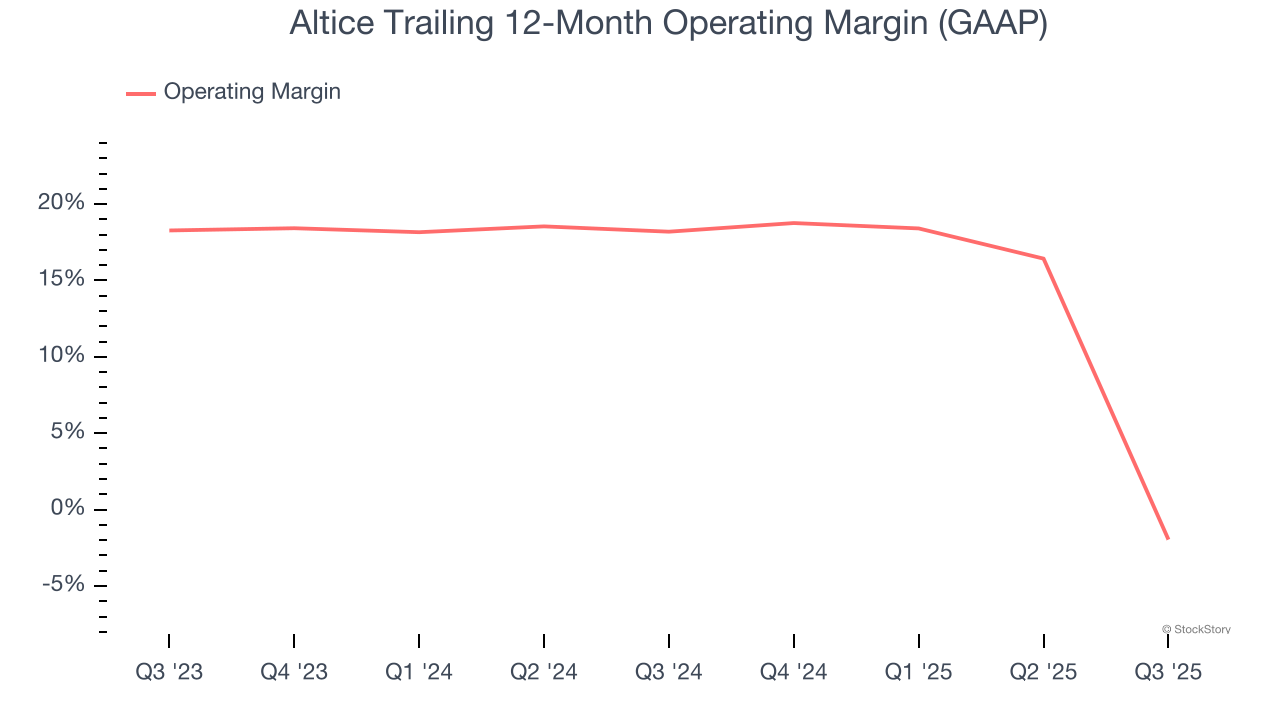

- Operating Margin: -55.3%, down from 20% in the same quarter last year

- Free Cash Flow was -$178.1 million, down from $76.87 million in the same quarter last year

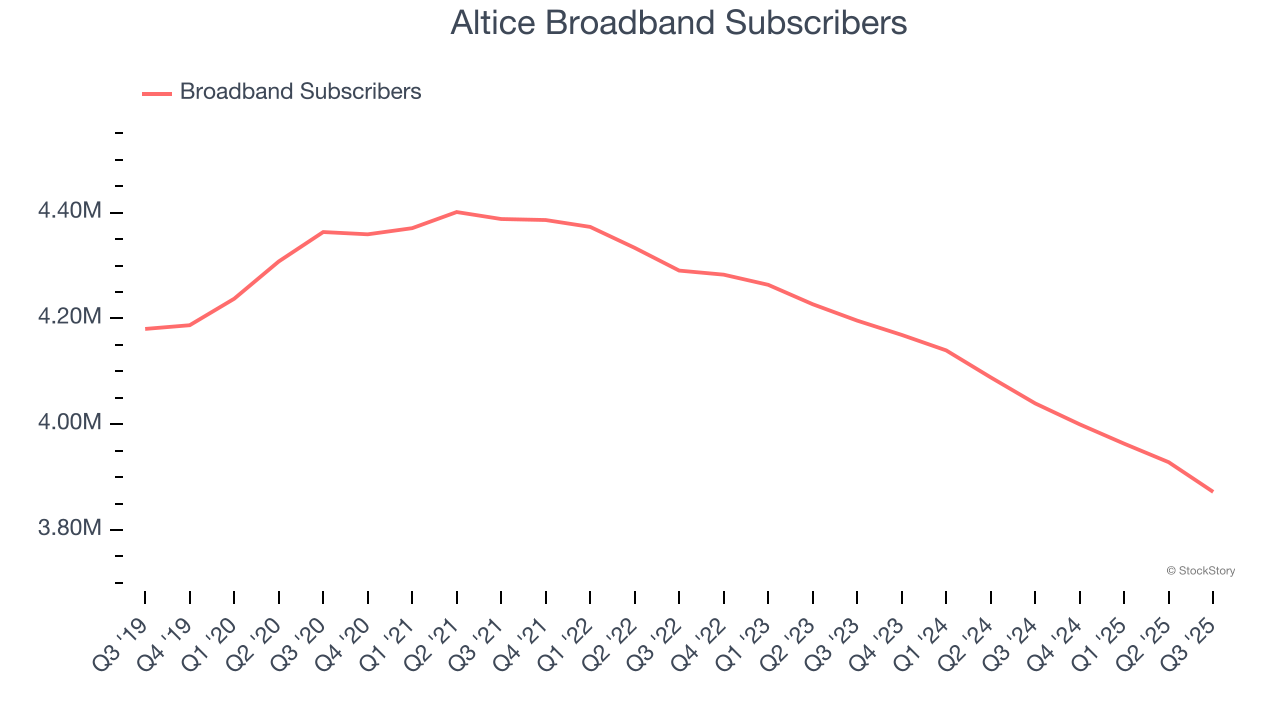

- Broadband Subscribers: 3.87 million, down 167,300 year on year

- Market Capitalization: $1.01 billion

Dennis Mathew, Altice USA Chairman and Chief Executive Officer, said: "In the third quarter, we delivered record gross margin performance and improved operational efficiencies, reaffirmed our full-year Adjusted EBITDA outlook, continued to elevate our customer and network experience, and achieved a milestone of over 700 thousand fiber customers. At the same time, we faced intense competition and a sustained low-growth environment, which resulted in softer broadband subscriber trends. Looking ahead, we are sharpening our go-to-market and base management strategies to strengthen our broadband performance and improve our revenue trajectory in this highly competitive landscape. We remain unwavering in our discipline and focus as we continue to build a more resilient business, positioned for sustainable, long-term growth and enhanced value for our shareholders. "

Company Overview

Based in Long Island City, Altice USA (NYSE: ATUS) is a telecommunications company offering cable, internet, telephone, and television services across the United States.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Altice’s demand was weak and its revenue declined by 2.5% per year. This was below our standards and is a sign of poor business quality.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Altice’s recent performance shows its demand remained suppressed as its revenue has declined by 3.6% annually over the last two years.

We can dig further into the company’s revenue dynamics by analyzing its number of broadband subscribers and pay tv subscribers, which clocked in at 3.87 million and 1.67 million in the latest quarter. Over the last two years, Altice’s broadband subscribers averaged 3.6% year-on-year declines while its pay tv subscribers averaged 13% year-on-year declines.

This quarter, Altice missed Wall Street’s estimates and reported a rather uninspiring 5.4% year-on-year revenue decline, generating $2.11 billion of revenue.

Looking ahead, sell-side analysts expect revenue to decline by 3.1% over the next 12 months, similar to its two-year rate. This projection doesn't excite us and indicates its newer products and services will not lead to better top-line performance yet.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Altice’s operating margin has shrunk over the last 12 months and averaged 8.3% over the last two years. The company’s profitability was mediocre for a consumer discretionary business and shows it couldn’t pass its higher operating expenses onto its customers.

In Q3, Altice generated an operating margin profit margin of negative 55.3%, down 75.2 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

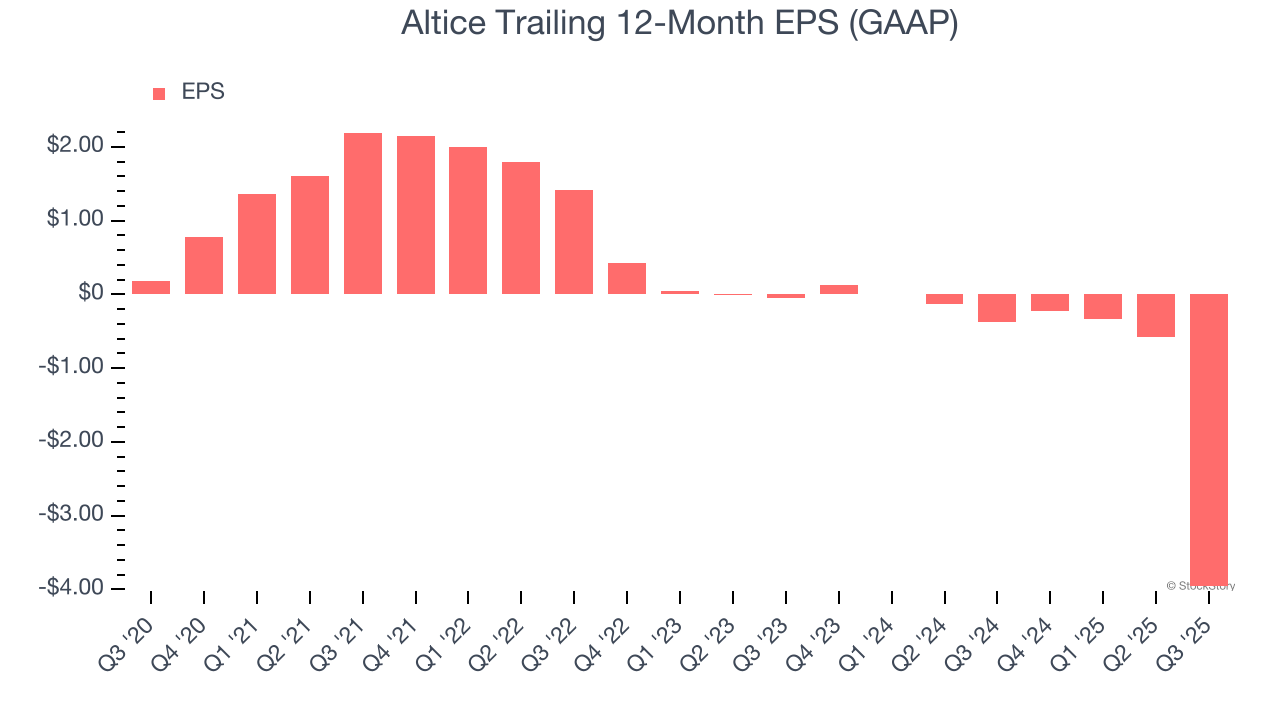

Sadly for Altice, its EPS declined by 88.3% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

In Q3, Altice reported EPS of negative $3.47, down from negative $0.09 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Altice to improve its earnings losses. Analysts forecast its full-year EPS of negative $3.96 will advance to negative $0.05.

Key Takeaways from Altice’s Q3 Results

We struggled to find many positives in these results. Its EPS missed and its revenue fell slightly short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 3% to $2.11 immediately following the results.

Altice’s earnings report left more to be desired. Let’s look forward to see if this quarter has created an opportunity to buy the stock. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.