As the Q3 earnings season comes to a close, it’s time to take stock of this quarter’s best and worst performers in the specialized consumer services industry, including Pool (NASDAQ: POOL) and its peers.

Some consumer discretionary companies don’t fall neatly into a category because their products or services are unique. Although their offerings may be niche, these companies have often found more efficient or technology-enabled ways of doing or selling something that has existed for a while. Technology can be a double-edged sword, though, as it may lower the barriers to entry for new competitors and allow them to do serve customers better.

The 10 specialized consumer services stocks we track reported a mixed Q3. As a group, revenues missed analysts’ consensus estimates by 22.2% while next quarter’s revenue guidance was 0.6% below.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 7.8% since the latest earnings results.

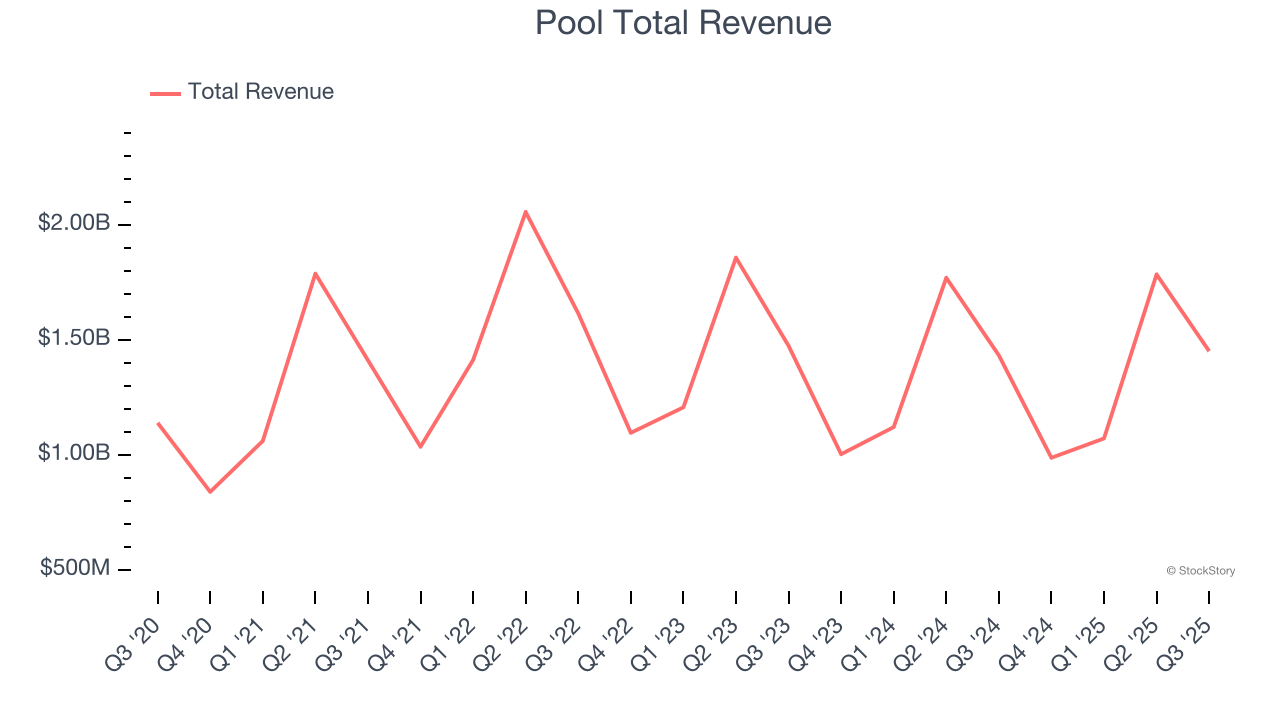

Pool (NASDAQ: POOL)

Founded in 1993 and headquartered in Louisiana, Pool (NASDAQ: POOL) is one of the largest wholesale distributors of swimming pool supplies, equipment, and related leisure products.

Pool reported revenues of $1.45 billion, up 1.3% year on year. This print was in line with analysts’ expectations, but overall, it was a mixed quarter for the company with full-year EPS guidance slightly topping analysts’ expectations but organic revenue in line with analysts’ estimates.

“Building on momentum from the second quarter, we achieved sales growth in the third quarter of 2025. Our dedicated teams delivered not only top-line growth but also expanded gross margin. We continued to strengthen our industry leading position by adding four new locations this quarter and elevated our customer experience through expanded private-label offerings and strategic product partnerships. This month, we proudly mark our 30th anniversary as a public company listed on the Nasdaq Stock Market, a milestone made possible by our team’s long-term strategic focus and ongoing commitment to offer our customers the best value proposition in the industry,” commented Peter D. Arvan, president and CEO.

Unsurprisingly, the stock is down 16.5% since reporting and currently trades at $249.

Read our full report on Pool here, it’s free for active Edge members.

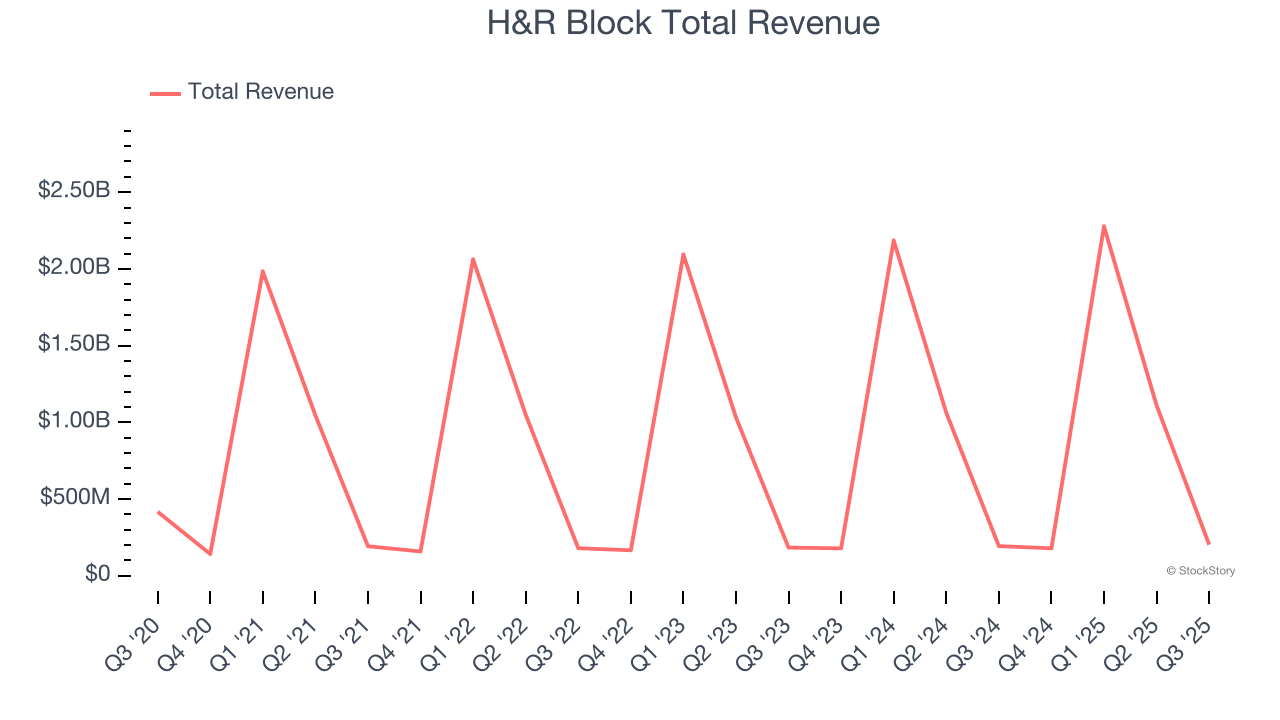

Best Q3: H&R Block (NYSE: HRB)

Founded in 1955 by brothers Henry W. Bloch and Richard A. Bloch, H&R Block (NYSE: HRB) is a tax preparation company offering professional tax assistance and financial solutions to individuals and small businesses.

H&R Block reported revenues of $203.6 million, up 5% year on year, outperforming analysts’ expectations by 1.5%. The business had a strong quarter with a solid beat of analysts’ EBITDA estimates and an impressive beat of analysts’ adjusted operating income estimates.

Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 6.9% since reporting. It currently trades at $47.90.

Is now the time to buy H&R Block? Access our full analysis of the earnings results here, it’s free for active Edge members.

Slowest Q3: 1-800-FLOWERS (NASDAQ: FLWS)

Founded in 1976, 1-800-FLOWERS (NASDAQ: FLWS) is an online retailer of flowers, gifts, and gourmet foods, serving customers globally.

1-800-FLOWERS reported revenues of $215.2 million, down 11.1% year on year, falling short of analysts’ expectations by 1.2%. It was a softer quarter as it posted a significant miss of analysts’ EPS and revenue estimates.

As expected, the stock is down 7% since the results and currently trades at $3.25.

Read our full analysis of 1-800-FLOWERS’s results here.

Frontdoor (NASDAQ: FTDR)

Established in 2018 as a spin-off from ServiceMaster Global Holdings, Frontdoor (NASDAQ: FTDR) is a provider of home warranty and service plans.

Frontdoor reported revenues of $618 million, up 14.4% year on year. This result beat analysts’ expectations by 1.1%. Taking a step back, it was a mixed quarter as it also recorded a decent beat of analysts’ EBITDA estimates but EBITDA guidance for next quarter missing analysts’ expectations.

Frontdoor scored the fastest revenue growth and highest full-year guidance raise among its peers. The stock is down 22.6% since reporting and currently trades at $50.85.

Read our full, actionable report on Frontdoor here, it’s free for active Edge members.

Carriage Services (NYSE: CSV)

Established in 1991, Carriage Services (NYSE: CSV) is a provider of funeral and cemetery services in the United States.

Carriage Services reported revenues of $102.7 million, up 2% year on year. This print surpassed analysts’ expectations by 1.3%. Zooming out, it was a mixed quarter as it also produced a narrow beat of analysts’ revenue estimates but full-year EBITDA guidance slightly missing analysts’ expectations.

The stock is down 5.1% since reporting and currently trades at $41.34.

Read our full, actionable report on Carriage Services here, it’s free for active Edge members.

Market Update

The Fed’s interest rate hikes throughout 2022 and 2023 have successfully cooled post-pandemic inflation, bringing it closer to the 2% target. Inflationary pressures have eased without tipping the economy into a recession, suggesting a soft landing. This stability, paired with recent rate cuts (0.5% in September 2024 and 0.25% in November 2024), fueled a strong year for the stock market in 2024. The markets surged further after Donald Trump’s presidential victory in November, with major indices reaching record highs in the days following the election. Still, questions remain about the direction of economic policy, as potential tariffs and corporate tax changes add uncertainty for 2025.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.