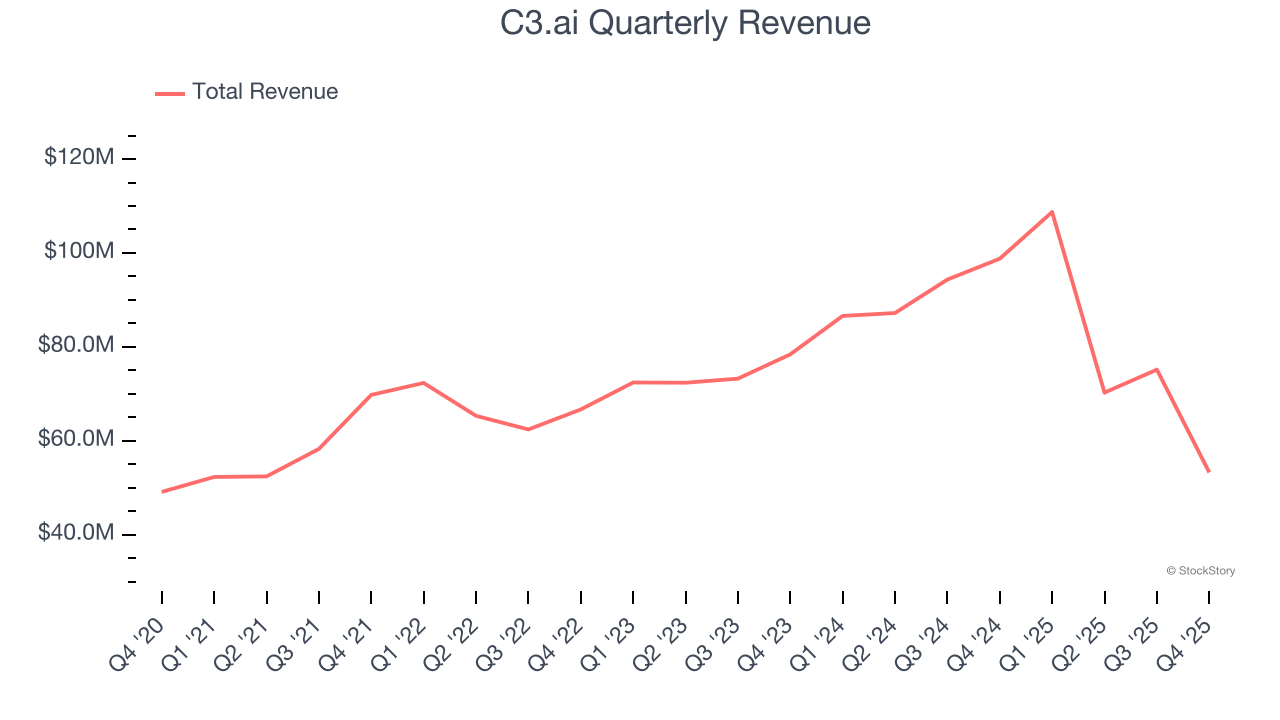

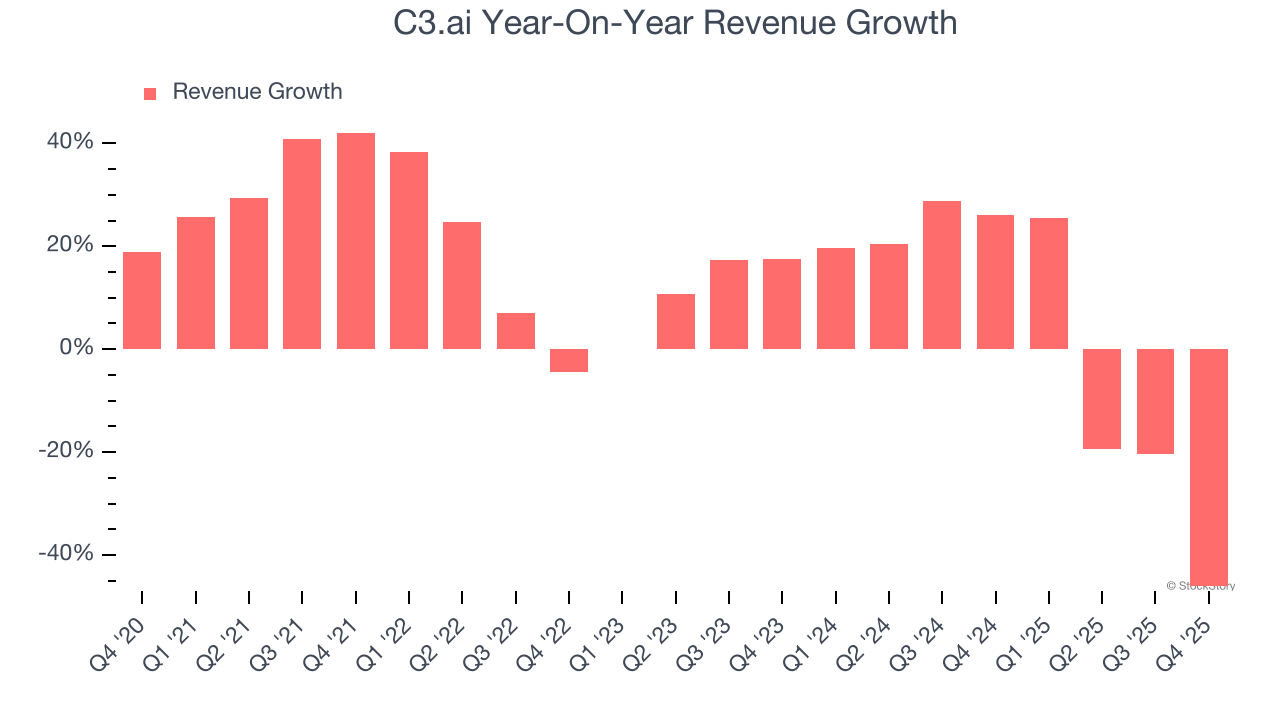

Enterprise AI software company C3.ai (NYSE: AI) missed Wall Street’s revenue expectations in Q4 CY2025, with sales falling 46.1% year on year to $53.26 million. Next quarter’s revenue guidance of $50 million underwhelmed, coming in 35.9% below analysts’ estimates. Its GAAP loss of $0.94 per share was 24% below analysts’ consensus estimates.

Is now the time to buy C3.ai? Find out by accessing our full research report, it’s free.

C3.ai (AI) Q4 CY2025 Highlights:

- Revenue: $53.26 million vs analyst estimates of $75.66 million (46.1% year-on-year decline, 29.6% miss)

- EPS (GAAP): -$0.94 vs analyst expectations of -$0.76 (24% miss)

- Revenue Guidance for Q1 CY2026 is $50 million at the midpoint, below analyst estimates of $78.01 million

- Operating Margin: -264%, down from -88.7% in the same quarter last year

- Free Cash Flow was -$56.2 million compared to -$46.88 million in the previous quarter

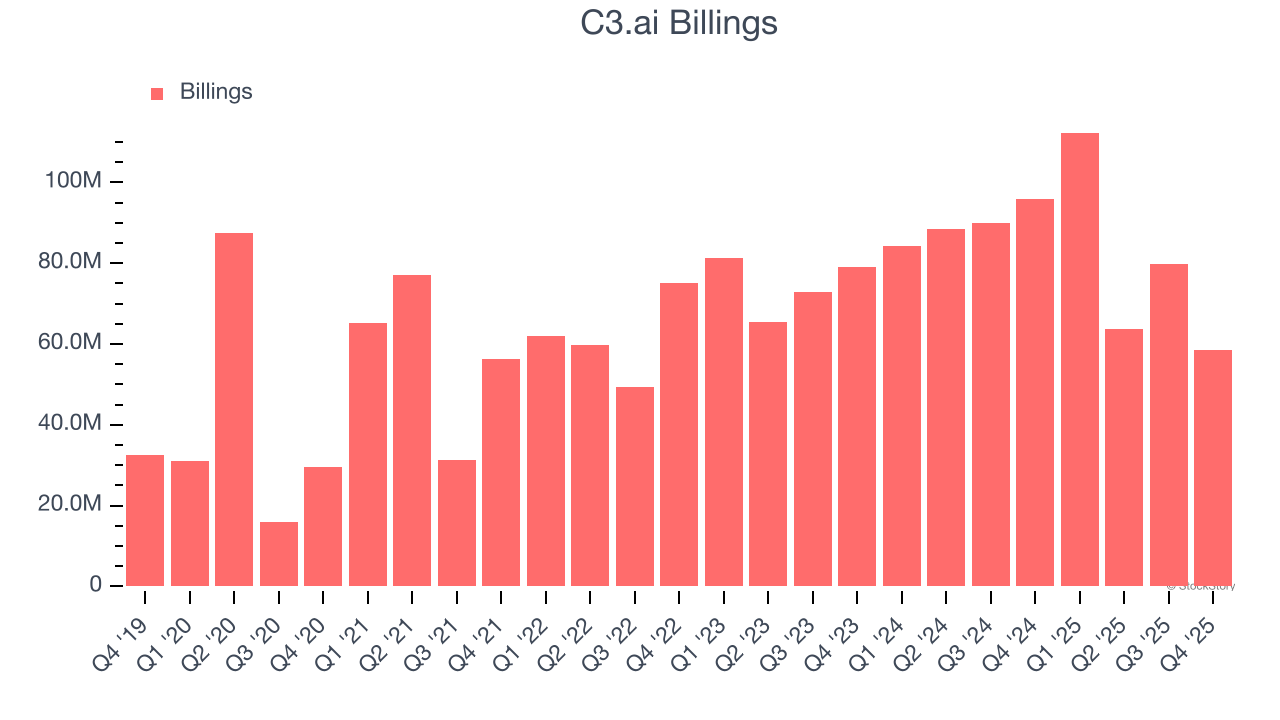

- Billings: $58.57 million at quarter end, down 39% year on year

- Market Capitalization: $1.42 billion

“I joined C3 AI six months ago and I did so with a clear conviction: this company is uniquely positioned to win in Enterprise AI. That conviction has been reinforced through extensive engagement with customers, prospects, partners, and investors. However, it was clear to me that we were not organized appropriately. We’ve reduced our cost structure and cash burn. We’ve restructured and flattened the sales organization. We’ve focused efforts on our best-in-class applications. We’ve shifted our go-to-market toward large-scale, enterprise-wide transformations. We’ve accelerated how we build and deliver product. And we are infusing our AI across every function at C3 AI. Those changes are substantially complete and C3 AI is now a more agile, more disciplined, and more accountable organization. Moving forward, our entire focus is on executing our return to growth and building C3 AI into a profitable, cash-positive business,” said Stephen Ehikian, CEO, C3 AI.

Company Overview

Named after the three Cs of its original focus—carbon, cloud computing, and customer relationship management—C3.ai (NYSE: AI) provides enterprise AI software that helps organizations develop, deploy, and operate large-scale artificial intelligence applications across various industries.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, C3.ai grew its sales at a 12.2% compounded annual growth rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the software sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. C3.ai’s recent performance shows its demand has slowed as its annualized revenue growth of 1.8% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

This quarter, C3.ai missed Wall Street’s estimates and reported a rather uninspiring 46.1% year-on-year revenue decline, generating $53.26 million of revenue. Company management is currently guiding for a 54% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 5.3% over the next 12 months. While this projection indicates its newer products and services will fuel better top-line performance, it is still below average for the sector.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

C3.ai’s billings came in at $58.57 million in Q4, and it averaged 11.2% year-on-year declines over the last four quarters. However, this alternate topline metric outperformed its total sales, meaning the company collects cash upfront and then recognizes the revenue over the length of its contracts - a boost for its liquidity and future revenue prospects.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

C3.ai is extremely efficient at acquiring new customers, and its CAC payback period checked in at 16 months this quarter. The company’s rapid recovery of its customer acquisition costs means it can attempt to spur growth by increasing its sales and marketing investments.

Key Takeaways from C3.ai’s Q4 Results

We struggled to find many positives in these results. Its full-year revenue guidance missed and its revenue guidance for next quarter fell short of Wall Street’s estimates. Overall, this quarter was quite bad. The stock traded down 20.8% to $8.18 immediately after reporting.

C3.ai’s earnings report left more to be desired. Let’s look forward to see if this quarter has created an opportunity to buy the stock. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).