Earnings results often indicate what direction a company will take in the months ahead. With Q2 behind us, let’s have a look at UL Solutions (NYSE: ULS) and its peers.

The sector has historically benefitted from steady government spending on defense, infrastructure, and regulatory compliance, providing firms long-term contract stability. However, the Trump administration is showing more willingness than previous administrations to upend government spending and bloat. Whether or not defense budgets get cut, the rising demand for cybersecurity, AI-driven defense solutions, and sustainability consulting should benefit the sector for years, as agencies and enterprises seek expertise in navigating complex technology and regulations. Additionally, industrial automation and digital engineering are driving efficiency gains in infrastructure and technical consulting projects, which could help profit margins.

The 7 government & technical consulting stocks we track reported a mixed Q2. As a group, revenues were in line with analysts’ consensus estimates.

In light of this news, share prices of the companies have held steady. On average, they are relatively unchanged since the latest earnings results.

UL Solutions (NYSE: ULS)

Founded in 1894 as a response to the growing dangers of electricity in American homes and businesses, UL Solutions (NYSE: ULS) provides testing, inspection, and certification services that help companies ensure their products meet safety, security, and sustainability standards.

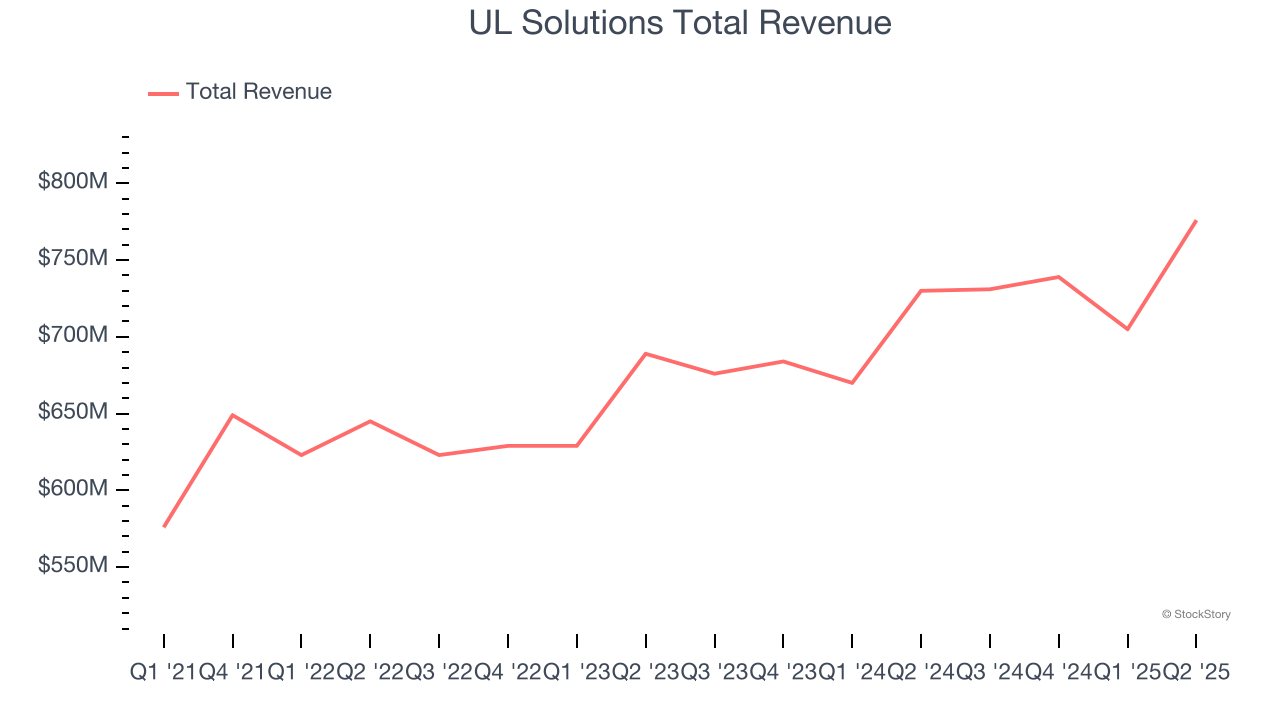

UL Solutions reported revenues of $776 million, up 6.3% year on year. This print exceeded analysts’ expectations by 0.6%. Despite the top-line beat, it was still a slower quarter for the company with EPS in line with analysts’ estimates.

UL Solutions achieved the fastest revenue growth of the whole group. Still, the market seems discontent with the results. The stock is down 16.9% since reporting and currently trades at $65.61.

Is now the time to buy UL Solutions? Access our full analysis of the earnings results here, it’s free.

Best Q2: Maximus (NYSE: MMS)

With nearly 50 years of experience translating public policy into operational programs that serve millions of citizens, Maximus (NYSE: MMS) provides operational services, clinical assessments, and technology solutions to government agencies in the U.S. and internationally.

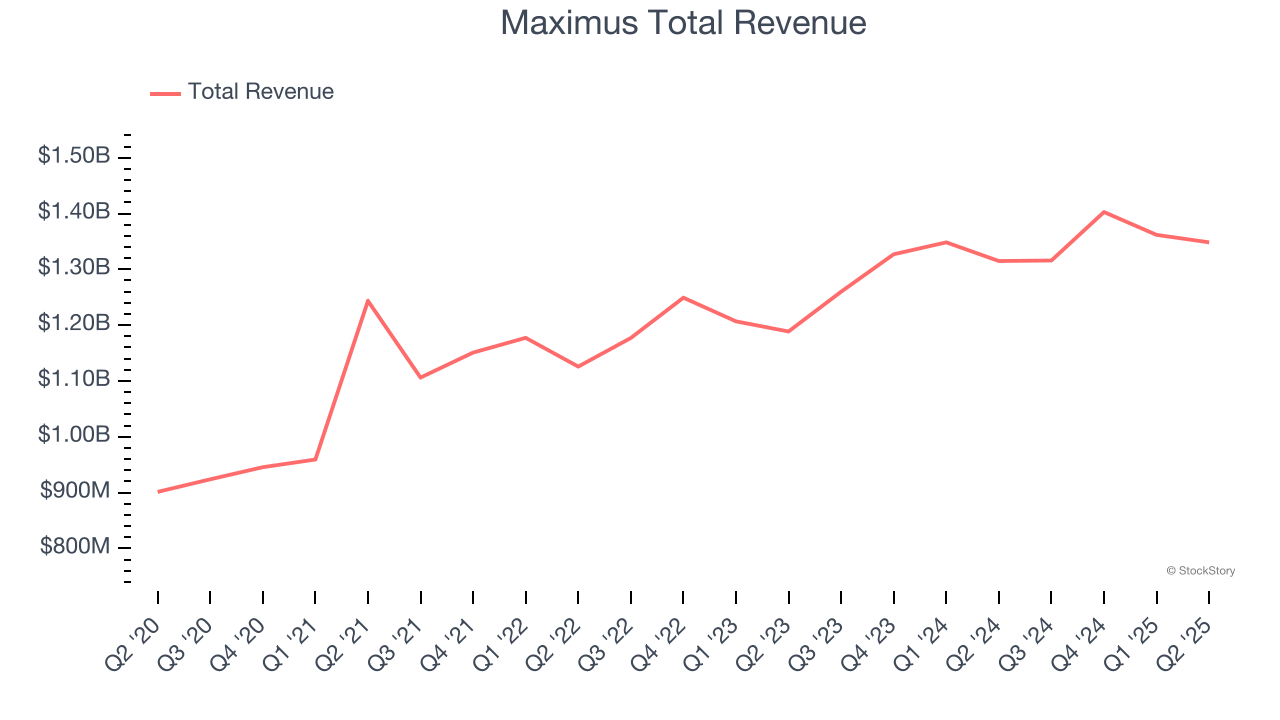

Maximus reported revenues of $1.35 billion, up 2.5% year on year, outperforming analysts’ expectations by 2.5%. The business had an exceptional quarter with a beat of analysts’ EPS and full-year EPS guidance estimates.

Maximus scored the biggest analyst estimates beat among its peers. The market seems happy with the results as the stock is up 16.9% since reporting. It currently trades at $87.42.

Is now the time to buy Maximus? Access our full analysis of the earnings results here, it’s free.

Weakest Q2: Amentum (NYSE: AMTM)

With operations spanning approximately 80 countries and a workforce of specialized engineers and technical experts, Amentum Holdings (NYSE: AMTM) provides advanced engineering and technology solutions to U.S. government agencies, allied governments, and commercial enterprises across defense, energy, and space sectors.

Amentum reported revenues of $3.56 billion, up 2% year on year, exceeding analysts’ expectations by 1.5%. Still, it was a slower quarter as it posted a significant miss of analysts’ EPS estimates.

As expected, the stock is down 5.4% since the results and currently trades at $23.96.

Read our full analysis of Amentum’s results here.

ICF International (NASDAQ: ICFI)

Operating at the intersection of policy, technology, and implementation for over five decades, ICF International (NASDAQ: ICFI) provides professional consulting services and technology solutions to government agencies and commercial clients across energy, health, environment, and security sectors.

ICF International reported revenues of $476.2 million, down 7% year on year. This result came in 1% below analysts' expectations. Overall, it was a mixed quarter for the company.

ICF International had the slowest revenue growth among its peers. The stock is up 14.2% since reporting and currently trades at $96.23.

Read our full, actionable report on ICF International here, it’s free.

SAIC (NASDAQ: SAIC)

With over five decades of experience supporting national security missions, Science Applications International Corporation (NASDAQ: SAIC) provides technical, engineering, and enterprise IT services primarily to U.S. government agencies and military branches.

SAIC reported revenues of $1.77 billion, down 2.7% year on year. This number missed analysts’ expectations by 5.1%. Zooming out, it was a mixed quarter as it also logged a beat of analysts’ EPS estimates but full-year revenue guidance missing analysts’ expectations significantly.

SAIC had the weakest performance against analyst estimates and weakest full-year guidance update among its peers. The stock is down 10.7% since reporting and currently trades at $101.69.

Read our full, actionable report on SAIC here, it’s free.

Market Update

Thanks to the Fed’s rate hikes in 2022 and 2023, inflation has been on a steady path downward, easing back toward that 2% sweet spot. Fortunately (miraculously to some), all this tightening didn’t send the economy tumbling into a recession, so here we are, cautiously celebrating a soft landing. The cherry on top? Recent rate cuts (half a point in September 2024, a quarter in November) have propped up markets, especially after Trump’s November win lit a fire under major indices and sent them to all-time highs. However, there’s still plenty to ponder — tariffs, corporate tax cuts, and what 2025 might hold for the economy.

Want to invest in winners with rock-solid fundamentals? Check out our Hidden Gem Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.