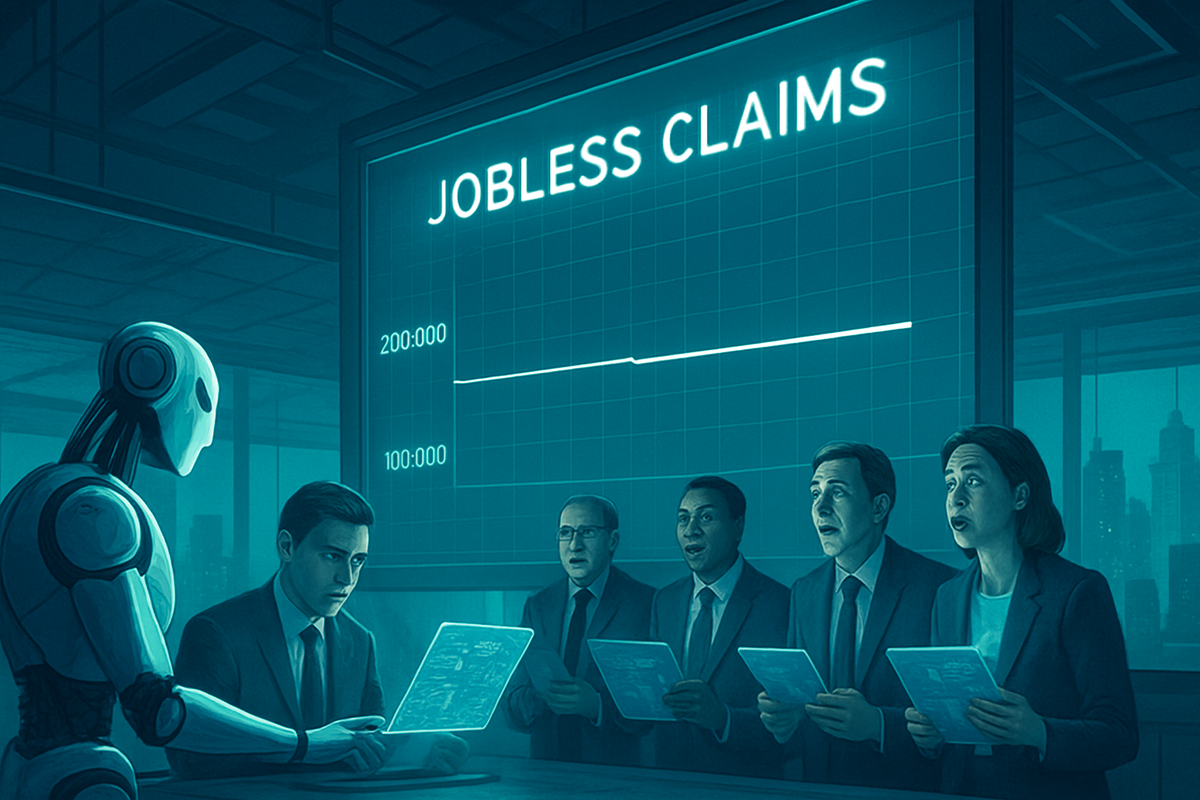

The United States labor market continues to exhibit a remarkable, if paradoxical, resilience as the first month of 2026 draws to a close. According to the latest data released this morning, weekly initial jobless claims rose slightly to 200,000 for the week ending January 17—a figure that notably undercut market expectations of 212,000. Despite a broader economic backdrop characterized by cooling consumer demand and a significant "budget rotation" toward artificial intelligence, the American workforce appears to be entrenched in a "low-hire, low-fire" regime that is keeping the unemployment rate stable at 4.4%.

This surprising data point suggests that while the era of rapid payroll expansion may be over, the widely feared "employment cliff" remains elusive. For the Federal Reserve, currently holding the target funds rate at a steady 3.5%–3.75%, the 200,000-claim threshold serves as a "resilience baseline" that complicates the path for further interest rate cuts in the first half of 2026. The immediate implication is a market that remains in a "wait-and-see" posture, balancing the stability of the labor market against persistent inflationary pressures.

Labor Hoarding and the 200,000 Threshold

The latest report from the Department of Labor marks a critical moment in the early 2026 economic narrative. Coming off a December that saw only 50,000 nonfarm payroll jobs added—the weakest annual growth since the pandemic recovery—analysts had braced for a surge in layoffs. Instead, the 200,000 figure reinforces a trend of "labor hoarding." Many firms, still scarred by the acute labor shortages of previous years, are choosing to retain staff even as margins are squeezed by rising costs and shifting fiscal policies like the One Big Beautiful Bill Act (OBBBA).

The timeline leading to this moment has been defined by a stark bifurcation in the economy. While job postings in traditional sectors have remained flat, AI-related roles have surged by over 130% since late 2025. This structural shift has created a protective shell around high-skill workers, while lower-skilled sectors are being bolstered by a "fiscal impulse" from new tax cuts. Initial market reactions were cautiously optimistic, with equity futures edging higher as the data suggests a soft landing remains achievable, even if the "landing" involves a stagnant hiring environment.

Winners and Losers in the "Low-Fire" Economy

The impact of this resilient labor market is not being felt equally across all sectors. Walmart (NYSE: WMT) appears to be a primary beneficiary of the current climate. As it officially joins the Nasdaq-100 index this month, the retail giant has moved aggressively to modernize its labor model. By implementing a new performance-based pay structure for over 500,000 hourly workers and leaning heavily into robotics-driven fulfillment, Walmart is navigating the "higher labor floor" better than its peers. Their ability to manage rising wages while maintaining a lean workforce is setting a new standard for the retail sector.

Conversely, UnitedHealth (NYSE: UNH) is struggling under the weight of this resilience. The healthcare giant saw its stock drop nearly 20% following disappointing 2026 guidance, as persistent labor costs—which now represent roughly 56% of total industry expenses—clash with stagnant reimbursement rates. For healthcare providers, the inability to find "cheap" labor in a tight market is leading to severe margin compression. Meanwhile, Microsoft (NASDAQ: MSFT) represents a middle ground; despite reporting a round of layoffs affecting up to 22,000 roles this January, the company is aggressively reinvesting those savings into AI infrastructure, effectively swapping human headcount for compute power.

NVIDIA (NASDAQ: NVDA) continues to operate in a league of its own, viewing the tight labor market as a theater for talent acquisition rather than a cost burden. Its recent $20 billion license and "acqui-hire" of Groq demonstrates that for the leaders of the "Inference Era," the price of specialized labor is a secondary concern to the necessity of speed and innovation.

The Broader Significance: Policy, AI, and Historical Precedents

This era of labor resilience fits into a broader industry trend of "Productivity Skepticism." In years past, a dip in hiring like the one seen in late 2025 would have heralded an immediate recession. However, the integration of AI is acting as a "productivity buffer," allowing companies to maintain output with fewer new hires. This mirrors the post-2008 recovery in some ways, but with the added complexity of the "Silicon Surcharge" and new tariff schedules that are pushing up the cost of goods even as labor remains tight.

The regulatory environment is also a factor. The OBBBA, which took full effect on January 1, 2026, has provided enough of a safety net for consumer spending to prevent a total collapse in service-sector demand. Yet, the Federal Reserve remains cautious. With Core PCE inflation hovering at 2.8%, the central bank is wary that a labor market that refuses to cool further could trigger a "wage-price spiral," especially as minimum wages rose in 22 states at the start of the year.

The Road Ahead: What to Watch in 2026

In the short term, the market will be laser-focused on whether the 200,000-claim level can be sustained. If claims consistently breach the 250,000 threshold, it would signal that the domestic manufacturing boom is failing to absorb workers displaced from the retail and healthcare sectors. For many companies, the strategic pivot of 2026 will be the transition from "AI experimentation" to "AI execution," where the focus shifts from simply hiring AI experts to actually realizing cost savings from automated systems.

Long-term, the labor market faces a "demographic ceiling." As the workforce ages and immigration policies remain a point of intense political debate, the scarcity of labor may become a permanent feature of the U.S. economy. Investors should watch for a "Fed Pause" that could extend until June 2026, as the central bank waits for more definitive signs that the "low-fire" environment isn't masking a deeper, more structural stagnation.

Conclusion: A Delicate Equilibrium

The latest jobless claims data confirms that the U.S. labor market remains a fortress of resilience in an otherwise turbulent economic sea. While the lack of aggressive hiring is a concern for long-term growth, the absence of mass layoffs is providing a necessary floor for consumer confidence and market stability. The "low-hire, low-fire" regime is the defining characteristic of 2026, forcing both the Federal Reserve and corporate America into a delicate balancing act.

Moving forward, investors should prioritize companies with "automation moats"—those capable of maintaining margins through technological efficiency rather than sheer headcount. The coming months will be a test of whether the U.S. economy can truly decouple growth from traditional employment metrics, or if the current stability is merely a prelude to a more significant structural adjustment.

This content is intended for informational purposes only and is not financial advice.