With a market cap of $51.9 billion, PayPal Holdings, Inc. (PYPL) is a global digital payments company that operates a large-scale, two-sided technology platform connecting merchants and consumers for online and in-person transactions. It offers a wide range of payment and financial solutions through brands such as PayPal, Venmo, Braintree, Xoom, and Zettle.

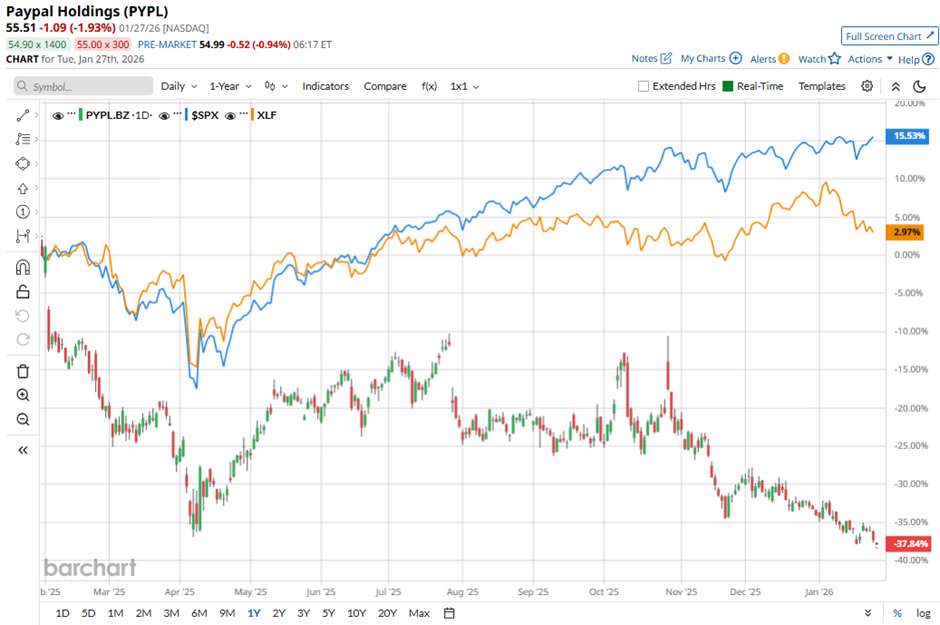

The technology platform and digital payments company's shares have lagged behind the broader market over the past 52 weeks. PYPL stock has decreased 38.5% over this time frame, while the broader S&P 500 Index ($SPX) has rallied 16.1%. Moreover, shares of the company are down 4.9% on a YTD basis, compared to SPX’s 1.9% gain.

In addition, shares of the San Jose, California-based company have also underperformed the State Street Financial Select Sector SPDR ETF’s (XLF) 3.1% return over the past 52 weeks.

Shares of PayPal rose 3.9% on Oct. 28 after the company reported strong Q3 2025 results, with adjusted EPS of $1.34 and revenue of $8.42 billion, both exceeding expectations. Investor sentiment was further boosted by PayPal’s new partnership with OpenAI, enabling ChatGPT users to buy products through its platform, and by the company’s decision to raise its full-year adjusted EPS forecast to $5.35 - $5.39.

For the fiscal year that ended in December 2025, analysts expect PYPL’s adjusted EPS to grow 15.3% year-over-year to $5.36. The company’s earnings surprise history is promising. It beat the consensus estimates in the last four quarters.

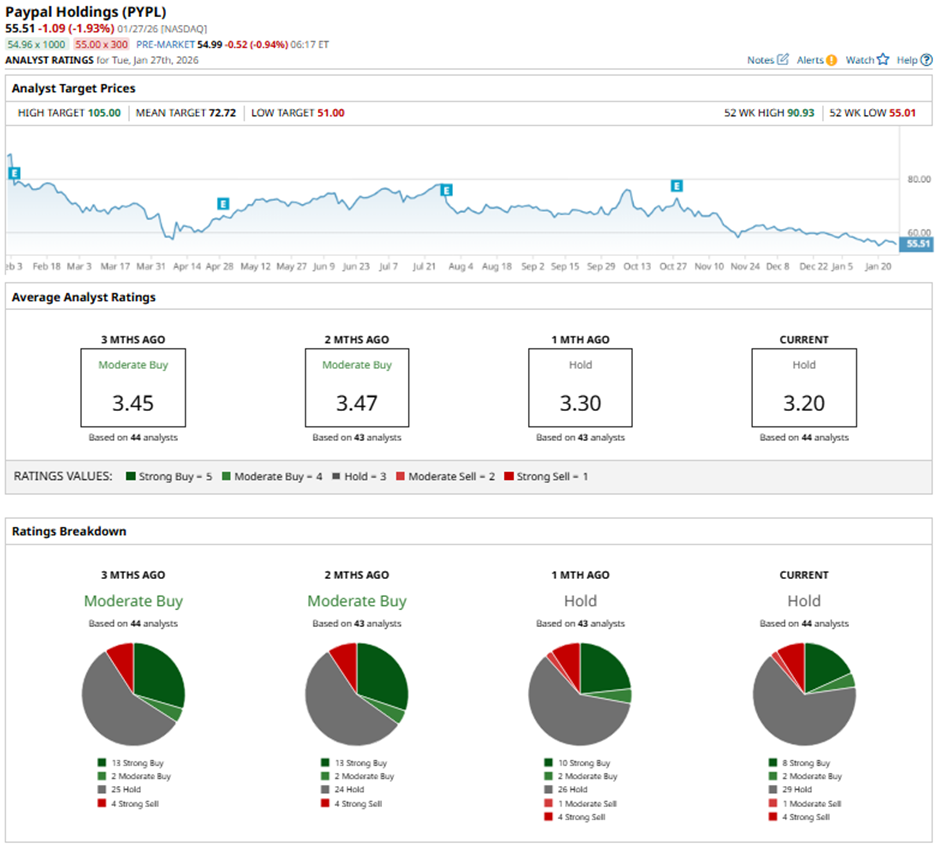

Among the 44 analysts covering the stock, the consensus rating is a “Hold.” That’s based on eight “Strong Buy” ratings, two “Moderate Buys,” 29 “Holds,” one “Moderate Sell,” and four “Strong Sells.”

This configuration is less bullish than it was three months ago, when PYPL had 13 “Strong Buys” in total.

On Jan. 8, Susquehanna lowered its price target on PayPal to $90 while maintaining a “Positive” rating.

The mean price target of $72.72 represents a 31% premium to PYPL’s current price levels. The Street-high price target of $105 suggests a 89.2% potential upside.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart